- We expect the last minute deal in the lame duck session to result in about 1.3% of GDP contraction, slightly less than our earlier prediction of about 1.5%.

- The compromise eliminated (or at least delayed) the possibility of the most damaging equity market outcomes.

- The deal failed to set up a framework for structural deficit reform in 2013. Almost immediately, Congress must address the debt ceiling, the sequester and the continuing resolution to keep the government funded.

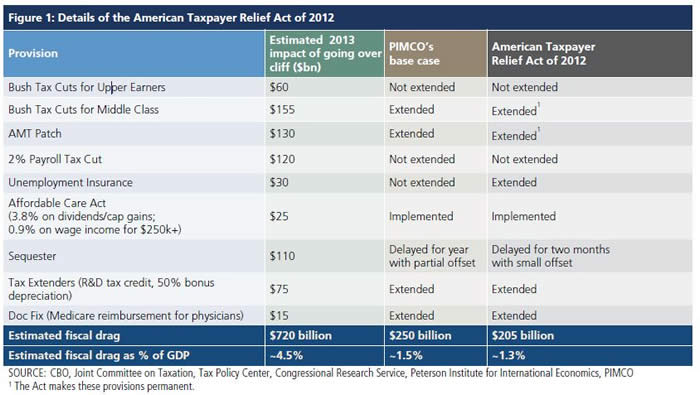

In our previous publications, we outlined a base case for a fiscal cliff resolution: a short-term, “mini” deal fashioned in the eleventh hour in the lame duck session of Congress that would largely avert the 4.5% fiscal contraction associated with going “off the cliff.” Our base case had assumed that a fiscal cliff deal would include a compromise on the upper-income rates; an extension of the middle class tax cuts and the AMT patch; an increase (and parity) in taxes on dividends and capital gains at 20% for upper earners; an expiration of certain stimulus measures, such as the payroll tax cut; and some sort of compromise to avoid the across-the-board spending cuts known as the sequester. We had predicted that such a resolution would result in fiscal drag of about 1.5% of GDP for calendar 2013, with most of the contraction stemming from the expiration of stimulus measures such as the payroll tax cut, an increase in rates on upper earners and some deficit reduction associated with a sequester delay.

Let's start with the overall economic impact. The (very) last minute deal in the lame duck session closely resembled our base case, though with marginally less fiscal contraction than we had expected: some 1.3% of GDP relative to our prediction of about 1.5% of GDP.

Turning to composition, the ultimate deal signed into law did differ in some components. For one, it included a one-year extension of unemployment benefits, a provision that proved to be a linchpin critical to getting liberal Democrats to vote for the deal. And two – and more surprisingly – the fiscal cliff compromise only delayed the sequester by two months, replacing it with a very small amount of deficit reduction (with little impact in 2013); we had expected that a more meaningful deficit down payment would be included in exchange for a full-year delay of the sequester.

While the ultimate fiscal cliff deal represented slightly less fiscal contraction than what we had assumed – a plus for U.S. economic growth in the short-term – the deal failed to increase certainty about many of the country’s fiscal issues.

True, the deal made permanent the tax cuts for the middle class, the AMT, and rates on investment income and estates – a victory for a majority of Americans who now have more clarity about their tax liabilities going forward. But making these provisions permanent vs. merely extending them for a year also carries an expensive price tag: Using a current law baseline, the Congressional Budget Office estimates that the fiscal cliff deal will add $3.9 trillion to the debt over the next 10 years.

More importantly, from an uncertainty perspective, the deal failed to set up a framework for structural deficit reform for 2013, and in doing so lawmakers neglected to address a trifecta of fiscal issues that the new 113th Congress will now have to address almost immediately: 1) the debt ceiling, which will have to be increased by March at the latest, 2) the sequester, which was only delayed for two months, and 3) the continuing resolution to keep the government funded, which is essential to address before the March 27th expiration in order to avoid a shutdown.

The net effect of all this? While investors thought that they might get a reprieve from Washington dysfunction after lawmakers spent an inordinate time dithering and posturing over the fiscal cliff that only produced a mediocre deal (at best), they instead will need to brace themselves for even more political brinksmanship in the weeks ahead as the new Congress turns to these important and looming fiscal issues. As these issues come into focus and the rhetoric begins, expect there to be more associated market uncertainty and volatility.

Do we expect the divisive and partisan tone that has plagued recent fiscal negotiations to continue in this new session of Congress? Unfortunately, yes. While there will be more than 90 new lawmakers in the 113th Congress, we still expect compromise to remain elusive: In fact, November’s election arguably produced an even more partisan House with fewer moderates, and given what will likely be tough primary races in the Senate in 2014, some senators might be even less inclined to compromise than before. There is also a noticeable chill among the various different party leaders after what were especially vitriolic negotiations – even by Washington’s standards – over the fiscal cliff deal.

At this point, even Congressional lawmakers don’t know how negotiations surrounding the debt ceiling, sequester and continuing resolution will ensue, but if we had to prognosticate, we would expect more muddling through from a policy perspective – not a dire outcome, such as a default on our country’s debt or a government shutdown, but no grand bargains either. And, as with every other fiscal negotiation of the past two years, we would expect there to be a lot of bluster and rhetoric leading up to what will likely result in a subpar deal at the last possible moment.

Investment implications

Translating the meaning of this “mini” fiscal cliff deal to portfolio positioning, lawmakers in Washington unfortunately have not given investors a clear signal. A grand bargain would have been the “all-clear” sign for equity markets and risk assets, which would have benefited both from the reduction in near-term uncertainty as well as the optimism that would have accompanied medium-term fiscal reform and bipartisan compromise. Alternatively, falling off the fiscal cliff would have been the “all-clear” sign for Treasuries, which would have been buoyed by the flight to quality by global investors in the face of an imminent and deep recession and political dysfunction. Instead, investors were given mixed signals.

Some components of the deal are moderately favorable for equities and credit-intensive fixed income investments. Others favor Treasuries.

The lower-than-expected fiscal drag in 2013 reduces the likelihood of near-term recession. The fact that a deal was reached at all eliminated (or at least delayed for now) the possibility of the most damaging equity market outcomes. And while certainly not an example of stellar legislating, the mini-compromise did reduce some of the uncertainties regarding future taxation. All of these factors support risk-taking, at least for a market that has become conditioned to expect little from politicians.

On the other hand, while the fiscal cliff ticking time bomb clock on television is no longer serving as a constant reminder of U.S. political dysfunction, it may be only a matter of days until it is replaced with a debt-ceiling sand-dripping hourglass graphic to warn investors about the disaster that will ensue if time passes without political action. As such, we expect elevated levels of market volatility compared to the relatively benign volatilities implied by options markets. Recent Fed action tying future central bank policy to economic variables rather than calendar dates also serves to increase market volatility, particularly around economic data releases. Given that we expect no debt ceiling resolution until the eleventh hour, we therefore expect volatility markets to react similarly to how they reacted in the last week of December (VIX Index up nearly 4%) and in the week surrounding the last debt ceiling compromise (VIX Index up more than 10%).

Finally, and on a more optimistic tone, we view the tax-exempt municipal bond market as a beneficiary of the mini-fiscal cliff package for two important reasons. First, the increase in the highest marginal tax bracket increases the marginal benefit to an investor of holding a tax-exempt municipal bond. While municipal bonds do not directly benefit from higher taxes, they are comparatively better off, as they are not hurt by higher taxes like most other investment alternatives. Second, while it is certainly not politically triumphant that tax reform was omitted from the fiscal cliff resolution, tax-exempt municipal bond investors can certainly rejoice for the time being.

Many of the tax reform proposals on the table during the fiscal cliff debate included an end, or at least a curbing, of the municipal bond tax exemption as a way of increasing revenue without increasing tax rates. Future tax reform remains a significant risk factor for the asset class, but with the issue being put on a crowded back burner (at least for now), tax-exempt municipal bonds will continue to enjoy their favored tax status and therefore investor demand.

So where does that leave us? Politicians will continue to keep investors on their toes regarding fiscal policy. Indeed, we expect policy uncertainty to be especially acute over the next two months as Congress addresses the debt ceiling, sequester and continuing resolution. Any hopes for a grand bargain – something we had always contended was much more difficult than the headlines suggested – have been mostly dashed for good, or, at least, quite a long time. What we should expect is more policy incrementalism coupled with polarized debate resulting in last-minute deals that don’t materially change the country’s fiscal trajectory. All in all, this will mean more uncertainty for markets with elevated levels of volatility for the foreseeable future.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to certain risks, including market, interest rate, issuer, credit and inflation risk; investments may be worth more or less than the original cost when redeemed. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Certain U.S. government securities are backed by the full faith of the government. Obligations of U.S. government agencies and authorities are supported by varying degrees but are generally not backed by the full faith of the U.S. government; portfolios that invest in such securities are not guaranteed and will fluctuate in value. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax.

© PIMCO

© PIMCO