I manage investment professionals for a living. When an analyst gives me the positives on one hand and the negatives on the other hand, but offers no conclusion, I want to cut one of those hands off. The best analysts understand all the issues but come to well-founded views.

I started writing this letter years ago. In the early days, it went to almost no one so it was a safe place to write whatever I wanted and really express a strong opinion, without being required to give the two-handed thing with no conclusion. That was exciting to me and it started us down the right path.

I have written bullishly in the past few years about the attractiveness of equities. I have talked about players for the economy coming out of the penalty box, such as energy, housing and manufacturing. Low valuations and the lack of bubbles or excess in consumer or corporate spending was a good starting point. I talked about how strong corporate profits (the micro) have outweighed the bad headlines (the macro), how I believe bad headlines are the friend of long term investors, and how they can provide investors with excellent opportunities to buy great companies at attractive valuations. Most of all, I’ve stressed the need to be unemotional in turbulent times to give yourself the chance to buy great companies at attractive prices.

And Then Depression Set In

If you have been reading my letters, you may have concluded that politically I am a conservative. When the presidential election results were in, it hit me and my bullish outlook like a ton of bricks. (For the 51% of the readers who just threw this letter away, please recycle. I’m an environmentalist too.) I always like to quote a good movie so I turn to the words of Bill Murray in Stripes. After losing his job and his girlfriend in the same day, he says, “and then depression set in.” The Obama victory crushed my psyche. Despite writing that investors above all should not be emotional, here I was in a funk.

To me, it is much more than just a question of your views on tax policy and entitlement spending. It is a question of who knows best – individuals or government? I grew up in liberal New England where motorcycle riders are required to wear helmets, you legally cannot put your studded snow tires on before November 15th and you cannot buy a soda of more than 16 ounces. I have been in Colorado for 25 years. Even though I don’t drink soda, I like that people can buy a big one if they want, I can put my snow tires on for our treacherous winter driving when I see fit, and for the two years I owned a motorcycle, I did not have to wear a helmet (but I did). Government is necessary to provide infrastructure, protection, and a safety net, but it does not have to make every decision in our lives.

Okay, I know what you are saying – Colorado just legalized marijuana. I agree with you, even Colorado has gone too far.

Parenting with Consequences

Watching the fiscal cliff negotiations and pondering how Congress is able to act like children got me thinking about parenting.

Babies do not come with instruction manuals. We have three children and my wife and I made plenty of mistakes in the early years. After a time, we came to adopt a parenting style called Parenting with Love & Logic,® also known as parenting with consequences. The idea is to encourage right behaviors by having logical and related consequences for a child’s actions. For example, when one of our kids would slam or lock the bedroom door against our wishes, we would simply remove the door for a few months. Their privacy was gone. The problem stopped, even after the door went back on. This change made a massive difference in our lives and I believe it helped us raise responsible kids that people enjoy being around.

I contrast our approach with the helicopter parents. The helicopters always hover around their kids to protect them and try to keep them from making a mistake, or from suffering any consequences from their bad decisions. Truth be told, helicopter parents believe their kids actually never make mistakes. These are the parents who do much of their kids’ homework and write essays for their college applications. Why worry, why be accountable when you have helicopter cover?

In terms of the U.S. Government, I consider Ben Bernanke to be a helicopter parent. Why should the federal government and its leadership worry about spending and running large deficits and debts when the Federal Reserve will buy an amount of Treasuries roughly in line with the deficit? While I am sure “Helicopter Ben’s” actions helped the economy somewhat over the past five years, the Fed has permitted bad behavior to continue in the form of trillion-plus dollar deficits, which I believe to be the source of our fiscal problems.

Consumers face consequences and appropriately, consumer debt fell in recent years. Meanwhile, sovereign debt in the U.S. and many developed nations increased significantly. Government debt exceeds household debt for the first time since 1996. Our failure to address the snowballing debt problem in the U.S. reminds me of the movie Austin Powers where a terrified, evil henchman is run over by a steam roller traveling at one mile per hour. This is an avoidable disaster.

I wonder what the rate of interest on U.S. Treasuries would be if the Federal Reserve were selling the same amount of Treasuries that it has been buying. In rough terms, net new government debt flowing into the marketplace would be more than $2 trillion per year, not zero. As we’ve seen in Europe, the pain point for most countries is 7% government bond yields. When you have rapidly expanding debt and interest rates rise from low levels to approximately 7%, you get a near tripling of debt service payments. Debt service dominates your budget. The solution becomes draconian cutbacks but, as we saw in Greece and Spain, not without social unrest or even street riots.

It need not go that far. I believe the fix to the deficit problems in the United States is partly through taxes, and partly through lower spending and some economic growth. We have to face the fact the United States made spending promises that it cannot keep and that there are adjustments that can be made. One consideration is improving the inflation calculations related to entitlements. Another example, average life expectancy in the United States, conservatively estimated, is eight years higher than it was in 1970, but the age for retirement and receiving Social Security and Medicare benefits generally has not changed. Surely, increasing life expectancy should give us some margin to gradually increase the retirement age.

We don’t need a perfect solution in Washington, just some progress toward the solution to restore confidence and growth. By dithering, our politicians are running away from their duties and ignoring the consequences. Listen: Sometimes awful kids with lousy parents surprise you and grow up to be great adults. You wonder how it happened. I hope that will be the case when our policy makers grow up too.

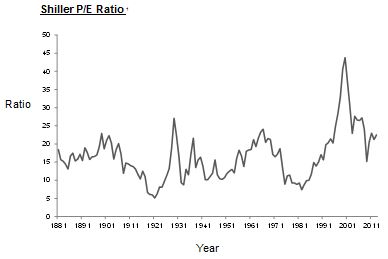

CAPE FEAR

Another movie, this one scary. Robert DeNiro’s villainous role in Cape Fear gave me nightmares. That was 21 years ago. Today’s CAPE Fear is a different thing entirely, but perhaps no less scary for its believers.

Some of the smartest strategists I know monitor something called the cyclically adjusted price-to-earnings ratio or CAPE. Unlike traditional price-to-earnings (P/E) ratios, it uses average, inflation-adjusted earnings over the past 10 years and not a single year’s number. With earnings generally growing over a decade, the CAPE is often higher than the P/E on current earnings. While the market has looked cheap on current P/E, particularly relative to today’s low interest rates, it has not looked cheap on CAPE, provoking a lot of fear among strategists and investors who focus on this measure.

Part of the wisdom of CAPE is to help an investor navigate the economic and profit cycles of companies, and cut through the emotion of good times and bad times to make good investment decisions. I respect it from that standpoint. Benjamin Graham and David Dodd recommended the use of CAPE in their seminal book Security Analysis, published in 1934. Robert Shiller wrote about it in his book Irrational Exuberance, so it is also known as the Shiller P/E. With the weight of strategists I respect, the voice of Benjamin Graham, and data showing a strong relationship between CAPE and subsequent 10-year returns, I got worried. Were these “low valuations” that supported my bullishness really a mirage?

No. In this circumstance, I am comfortable disagreeing with the great ones’ premise. I agree that if you can buy stocks at a CAPE of eight to15 times, you should be incredibly bullish. But the ratio is rarely that low. It fell below 15 times in late 2008, but prior to that had not seen that territory since the 1980s.

CAPE believers have argued the market has been as much as 40% over-valued. I believe this is too bearish.

CAPE believers have argued the market has been as much as 40% over-valued. I believe this is too bearish.

CAPE suggests that we are at a cyclical peak in profits, or at least a frothy valuation of corporate earnings power. For a few years, CAPE fear has been saying to stay out of stocks. I plan to write a longer analysis of CAPE fear when I have more space, but let me for now say simply and clearly that I disagree. It hardly feels that we are at a cyclical peak in the economy. After the Great Recession, economic growth has been low and erratic. According to the Wall Street Journal, “U.S. growth is currently weak, and overall output is 13.5% lower than what it would be had we continued on the pre-2008 trend.”2 Corporate profits have been strong, despite a global economy that has been largely disappointing since the Lehman Crisis.

Shiller P/E Ratio 1

There are always skeptics. Many market strategists have been claiming for years that profit margins, in an uptrend for nearly 10 years, were too high and poised to fall, undermining the outlook for stocks. The source of the margin expansion, however, is mostly lower interest expense from deleveraging and lower taxes from more non-U.S. revenues. These factors can persist. Most people are too optimistic so I try to listen closely to the pessimistic cases. When the argument is for margins to go down because they went up, however, my eyes glaze over. That’s not logic, only fear. I hate that.

Despite negative real interest rates, corporations are sitting on record levels of cash. Capital spending by corporations has been constrained for years due to a lack of confidence. Consumers have deleveraged and have not overspent on autos, credit cards and homes. Overall, durable goods spending, despite having rebounded, is two standard deviations below the long-term trend and at recession levels. Despite the uncertainty and the dysfunction in Washington, the outlook is positive. Consumer confidence hit a five-year high in December. We just need that confidence to spread to corporate board rooms, improving the outlook for capital spending. Housing is clearly turning up, with a lot of room to run. Rising home prices are leading to a wealth effect and restored confidence, which should support spending in the next few years. The energy renaissance in America is a game changer for that industry and many others. The U.S. has become more competitive and firms would like to move manufacturing back to the U.S. The U.S., despite the headlines, is in better shape than it has been in decades.

Europe still has problems but the financial system is not crumbling as many had worried. Japan has a new sheriff who is committed to getting the economy out of its long funk. China, a key driver of global economic growth, has stabilized and is turning up. Manufacturing jobs are growing at double digit rates in six states including North Dakota, Oklahoma and Washington.

![]()

1 Source: Shiller, R. Irrational Exuberance. Princeton University Press, 2000. Print

2 Edward Prescott and Lee Ohanian, “Prescott and Ohanian: Taxes are Much Higher Than You Think,” WSJ Article – Taxes Are Much Higher Than You Think,” Wall Street Journal 12/12/12.

2012 was the most miserable bull market I can recall. It was miserable from the standpoint of a lot of volatility and bad news, and a lot of investors sitting on the sidelines as equities appreciated without them. I have a hard time believing that the upturn is over when the historic equity outflows of the past few years have not even begun to reverse. The stage is set for better economic growth around the world. This will be good for employment and corporate profits. With a sound earnings base and low valuations, stocks should do well. We don’t need a perfect solution in Washington, just some progress toward the solution to get the economy and markets back on a sustainable path.

Get over the fear as – I hope you can tell – I got over my depression.

Sincerely,

Jim Goff, CFA

Director of Research

Please consider the charges, risks, expenses and investment objectives carefully before investing. For a prospectus or, if available, a summary prospectus containing this and other information, please call Janus at 877.33JANUS (52687) or download the file from janus.com/info. Read it carefully before you invest or send money.

Investing involves market risk. Investment return and fund share value will fluctuate and it is possible to lose money by investing.

Past performance is no guarantee of future results.

There is no assurance that the investment process will consistently lead to successful investing.

The opinions are those of Jim Goff as of December 2012 and are subject to change at any time due to changes in market or economic conditions. The comments should not be construed as a recommendation of individual holdings or market sectors, but as an illustration of broader themes. Past performance is no guarantee of future results.

S&P 500® Index is a commonly recognized, market capitalization weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance.

In preparing this document, Janus has relied upon and assumed, without independent verification, the accuracy and completeness of all information included in this letter which is from a variety of sources such as U.S. Government Agencies, International Strategy & Investment (“ISI”), Empirical Research and research departments of global investment firms. Janus cannot be held responsible for any direct or incidental loss incurred by applying any of the information in this publication.

Statements in this piece that reflect projections or expectations of future financial or economic performance of a mutual fund or strategy and of the markets in general and statements of the Fund’s plans and objectives for future operations are forward-looking statements. Actual results or events may differ materially from those projected, estimated, assumed or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to the other factors noted with such forward-looking statements, include general economic conditions such as inflation, recession and interest rates.

Investment products offered are: NOT FDIC-INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Janus Distributors LLC (01/13)

FOR MORE INFORMATION CONTACT JANUS

151 Detroit Street, Denver, CO 80206 I 800.227.0486 I www.janus.com

C-0113-32325 04-30-13

188-15-23486 01-13

© Janus Capital Group