Markets work. Not because they are perfect, but because they self-correct. Inherent to their functioning is the ability for buyers and sellers, borrowers and lenders, to freely express their predilection to engage in commercial transactions as proxied by the price mechanism. This is all utterly basic. So, why are the capital markets in general, and the credit markets in particular, not to be trusted to operate without the price and quantity guidance of the Federal Reserve? Is the American economy in a better place than when it was in the throes of the financial crisis? Of course. And, to a very great degree, we can all collectively thank Chairman Bernanke for his decisive execution of the Fed’s lender of last resort mission in 2008-2009. But that was then. Might the Fed now be jeopardizing its legacy by fostering a colossal misallocation of resource? If so, then what recovery may come would have all the permanence of a sandcastle.

The Fed has dutifully sat by the patient’s side for over four years. But when Mr. Bernanke originally administered his concoction of zero rates and quantitative ease, the Fed was confident that these truly extraordinary monetary actions were emergency measures from which “exit” was a year, at most two, away. The Fed had diagnosed the “patient” as suffering from a shortage of aggregate demand and concluded that the doctor needed to “manufacture” consumption so as to get the patient back on the playground. The Fed commanded short rates be zeroed out and quantitative easing initiated. To what end? According to the Fed’s essentially Keynesian logic, the negative rate environment facilitated by these policies foster an intertemporal shift away from savings and towards consumption. In so doing, consumer demand is lifted and realtime economic growth is enhanced. Additionally, the never-this-low in recorded history level of mortgage rates is intended to spur a “wealth” effect by pumping up the housing market. According to theory, if you get enough people spending and enough people feeling wealthy, the demand side of the economy will throw a party, inducing businesses to hire, leading us to a sustained prosperity.

There can be little doubt these policies “work”, in the sense that their first-order effects are exactly what the Fed advertises them to be. Of course, seeing what is in plain sight really isn’t that much of a talent which is likely why the capital markets tend not to reward investors for this “skill.” For this reason, the more relevant issue for 2013 is evaluating the longer term “costs” associated with these monetary programs. After all, monetary policy, like government itself, is not magic. Hence, policies may “hit” their intended near-term targets, but they do not operate in vacuo. For instance, lower rates obviously enhance demand for loans; conversely, lower rates also compress net interest margins, thereby shrinking the risk appetites of lenders. All actions have consequences.

FED BUYING DRIVES DOWN MORTGAGE YIELDS TO RECORD LOWS . . .

Source: BofA Merrill Lynch Global Research, CoreLogic

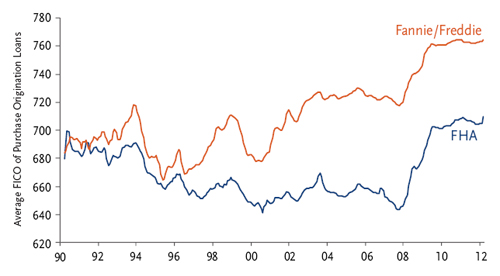

…YET PURCHASE MORTGAGE LENDING STANDARDS ARE AS TIGHT AS EVER

Source: Bloomberg, TCW

In light of recent job growth, rising home prices, and the mitigation of risk on/off market dynamics, some might think we ought to stop worrying and love the financial repression. Yet the policies of the day pose interesting questions to those who ponder the second-order effects of the Fed’s “beneficent” stimulus. For instance, wouldn’t an intertemporal shift away from savings have the obvious effect of decreasing savings? Perhaps you question whether this matters. After all, under a fractional banking system, even a modest pool of savings can be levered into a stupendous amount of credit creation. If loans can be created with the stroke of a banker’s pen, why do savings rates matter? Because, of course, financial intermediation is not magic, either. Loans do have to paid back and tomorrow does eventually come. More technically, the lower the level of “true” savings, the higher the leverage ratios an economy must engineer so as to achieve the Fed’s “targets” for credit expansion. More insidiously, the existence of a financial “veil” does not banish the underlying economic reality. Some forms of credit creation (eg. a mortgage refinancing) have a redistributive quality to them that is qualitatively different than say a developer borrowing to pour concrete into the foundations of a hundred new homes to be constructed. While credit creation might be more or less infinitely elastic, the supply of resources (e.g. concrete) available to launch capital projects is not. If you consume all your seed corn, all the credit creation in the world can’t do anything more than redistribute what we already have. Persist, and you’ll just end up inflating asset prices.

Further, if money is essentially a measure, a unit of exchange, then how can Fed money printing (credit creation) truly and sustainably create wealth? Isn’t true wealth a function of the ability of a business or employee to provide or invent a good or service that has value to another? In that event, pumping up home prices may have some perverse second-order effects. For instance, say you are a renter. The Fed’s policies are helping to drive up not just the price of homes but also of rents. A “typical” young couple has to shell out more for rent today and has a bigger lifetime “nut” to pay in the form of future mortgage payments for that home they aspire to purchase. Do these policies make the couple wealthier – or simply transfer existing wealth? Is there not a fundamental distinction between rising home prices driven by the higher wages of a growing economy versus higher prices resulting from mortgage “price fixing” courtesy of the Fed’s QE?

And then there is the matter of the US Federal government. In the parlance of another era, it is in the business of tax and tax, and spend and spend. Or, if you prefer, to borrow and borrow. All this is done in the name of economic “stimulus.” Implicitly, resources used by the private sector to either spend today or to commit to capital projects is “not stimulative.” And since government isn’t magic, Federal borrowings are our borrowings (if you are fortunate enough to be a US taxpayer!). While many have earned, or might need, the largesse of our national government, there are some inconvenient truths to government spending that ultimately need to be confronted. First, if the Keynesian inspired recovery doesn’t happen according to plan, the Feds are either going to have to tax a lot more or spend a lot less. Second, Federal debts need to be repaid, or at least serviced. Don’t worry, some say: Treasury rates are negative and so the government is making money off the borrow. Trouble is, rates won’t always be negative and even if they were, the no free lunch principle holds: transferring wealth from the owners of Treasury debt is not the same as wealth creation.

So now we live one of the great economic experiments of all time. If the Fed is “right” that you can spend your way to prosperity, all this doubt surrounding second-order effects and the unsustainability of the policy regime will turn out to be much ado about nothing. Keynesianism will have achieved an impressive victory as sustainable growth returns. In the alternative, we may well come to see that much of what is called “stimulus” today is merely a convenient term for redistributing wealth and resources according to the priorities of the Fed and the national government. If so, then we will find that the reconfigured economy of tomorrow will be inefficiently constructed. Perceived stability today just might be setting us all up for a sucker punch of stagflation tomorrow. And tomorrow does eventually come.

LEGAL DISCLOSURES

This publication is for general information purposes only. Past performance is no guarantee of future results. While the information and statistical data contained herein are based on sources believed to be reliable, we do not represent that it is accurate and should not be relied on as such or be the basis for an investment decision.

Any opinions expressed are current only as of the time made and are subject to change without notice. TCW assumes no duty to update any such statements. The views expressed herein are solely those of the author and do not represent the views of TCW as a firm or of any other portfolio manager or employee of TCW. Any holdings of a particular company or security discussed herein are under periodic review by the author and are subject to change at any time, without notice. In addition, TCW manages a number of separate strategies and portfolio managers in those strategies may have differing views or analysis with respect to a particular company, security or the economy than the views expressed herein.

MetWest is a wholly-owned subsidiary of The TCW Group, Inc.

© TCW Asset Management