The recent “energy dividend” is not likely to last.

February 15, 2013

- The recent “energy dividend” is not likely to last

- Crafting a single monetary policy for Europe is challenging

Our first car was a 1960s era Cadillac, which my wife’s grandparents gave us. The remnants of fins still flanked the trunk, which could sleep three people comfortably. While smaller cars cowered under viaducts during heavy rain, our Betsy would plow ahead, a foot-high wake trailing behind. Much to my chagrin, the engine would rev itself at stop lights, daring drivers in the adjacent lanes to race.

At first, I wondered why anyone would give away such a great car. But the engine consumed both oil and gas at frightening rates, at a time when petroleum prices were tripling in the space of just three years. We eventually had to trade Betsy for a compact car; a sensible choice, but nowhere near as fun.

On a small scale, the cost of energy has a significant influence on consumers. On a larger scale, it drives geopolitics. For most of the last generation, prices have been rising and tension between producers and consumers has been high. In the last year, however, the world has been reaping a bit of an energy dividend. This has been one of the few clear bright spots during an otherwise challenging economic interval.

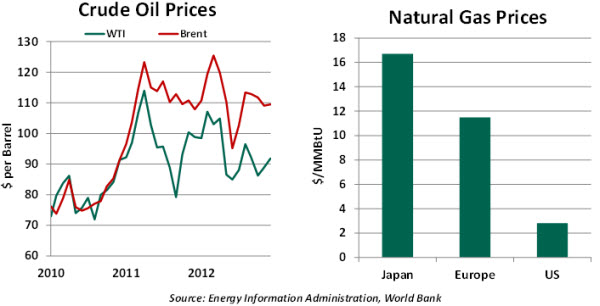

Except during the recession of 2009, 2012 was the first year in a decade that saw energy prices retreat. Supply and demand elements are both at play. Oil production in the United States has risen by almost 15% over the past year, thanks to improved harvesting techniques. Many OPEC nations have been producing aggressively to generate export earnings. On the consumption side, slow economic growth has diminished the appetite for energy in the developed world.

Because energy is not the easiest thing to transport, important cost differences between regions can arise. For this reason, the United States is presently enjoying more of a dividend than other parts of the world. In spots, this is contributing to some modest migration of manufacturing back to North America and consideration of expanded energy exports.

For countries that are net importers of energy, lower prices allow greater consumption of other items, enhancing GDP growth. Moderating fuel costs also help to contain inflation. Broad measures of consumer prices have been falling in the United States and in Europe, freeing central banks to be accommodative without compromising their inflation-fighting principles.

The Bank of England and the European Central bank target overall price levels, where the energy dividend is very direct. But even the “core” inflation (which excludes energy prices) targeted by the Federal Reserve has been muted by recent developments. Energy is a direct cost in the production of many finished goods, and drives the cost of transporting people and products.

The question is how long these relatively benign conditions can last.

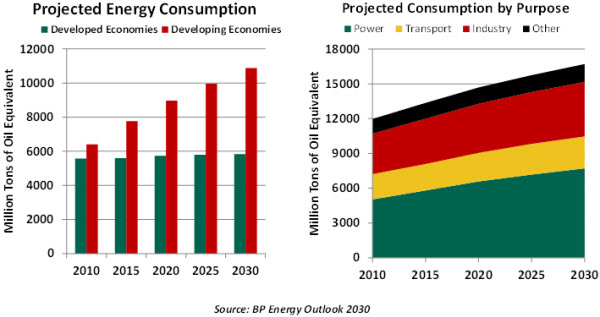

At some point, developed economies will return to normal rates of growth. As that occurs, demand for energy to fuel economic growth will re-accelerate. Developing nations are generating more drivers, more homeowners, and broader ownership of electronics; all of this requires power.

The environmental impact of energy generation is getting additional scrutiny. In the wake of the 2011 tsunami, Japan and Germany have taken steps to reduce their reliance on nuclear power (and, as a consequence, have increased their consumption of fossil fuels). Damage done to the earth’s substrata by aggressive harvesting methods has generated concerns. And the debate over carbon emissions has only been heightened by the recent string of severe storms and record global warmth.

Should the international community take steps to ameliorate environmental consequences, they would undoubtedly add to the cost of energy.

And the world’s leading energy-producing region is in a considerable state of flux. Regime change in Egypt, Libya, and Yemen began with excitement but has devolved into instability. Syria remains engaged in civil war. Iran’s nuclear program and its threats against the Suez shipping channel are troubling. Without careful diplomacy, the Arab Spring could descend into a disappointing fall.

If things break the wrong way in the Middle East, the benefits of cheaper energy could reverse. Economic growth could be stunted, and inflation could rise. The resulting stagflation could find central banks tightening credit earlier than they would prefer. Over the longer term, global supply and demand forces will likely result in higher energy prices. This will place a premium on intelligent energy usage.

Not long ago, I was driving a rented hybrid on the way to see clients. At a stoplight, a 1960s Cadillac pulled up beside me. I could swear that the headlight winked at me, but I couldn’t bring myself to return the gesture. Best to leave that part of my past behind.

European Central Bank: One Policy, Many Countries

The European Central Bank (ECB) left the monetary policy rate unchanged at 0.75% last week and its policy statement pointed out that “the risks surrounding the economic outlook for the euro area continue to be on the downside.” President Mario Draghi’s remarks last summer indicating that the ECB will do “whatever it takes” to prevent a disintegration of the currency and the announcement of “Outright Monetary Transactions” appear to have worked financial market magic, for now, with notable improvements in eurozone stock prices, sovereign bond yields, and credit default swap spreads. These positive developments in financial markets are yet to make their way into the real economy.

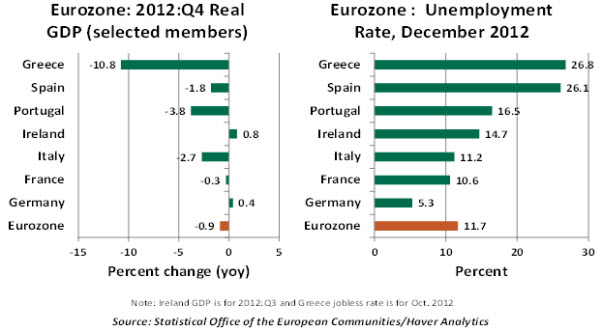

Real eurozone GDP declined for three straight quarters at the end of 2012, shrinking 0.9% in the past year. There is a vast disparity in the pace of economic activity among members of the eurozone. At one extreme, real GDP of Greece fell nearly 11.0% from a year ago, while that of Spain, the fourth largest economy, declined 1.8% in the same period. Real GDP of Germany, the engine of the eurozone, slipped in the fourth quarter, but it maintains a small gain on a year-to-year basis.

The unemployment rate of the eurozone is 11.7%, a new high for the economic bloc. Within the region, Greece is experiencing the harshest labor markets conditions with an unemployment rate of 26.8%, while Germany is an enviable position with a 5.3% unemployment rate, the lowest since the recession high of 9.0% in June 2009.

Inflation in the eurozone ranges from 0.3% to 2.8%, the average for the economic region was a 2.0% year-to-year increase in January. The latest reading matches the ECB’s inflation target, which is has achieved after two years of inflation headline numbers holding above its goal. Germany is very firm on achieving and maintaining the inflation target. Therefore, at the ECB’s Governing Council meeting, Germany would certainly be a voice of dissent if monetary policy easing is considered to stimulate economic growth.

The financial market calm is masking the fact the ECB is still dealing with a serious economic crisis. The important aspect to track is how well the recovery dynamics in the real sector is working. Taken together, the eurozone’s economic fundamentals are still woefully weak and the depth of the economic crisis is not uniform. The ECB faces the challenge of balancing the demands of weak and strong members and votes of all members, from Greece to Germany, carry equal weight. Crafting a suitable monetary policy for one and all is the ECB’s challenge for 2013.

© Northern Trust