Many investors generally turn to China for its growth potential, and this, often singular, emphasis on investing for earnings growth means they tend to overlook the importance of dividends. When the long-term historical performance of global equity markets is considered, investors can see that the contribution of dividends to total return is significant. In this regard, China has been no exception. Between 1999 and 2012, 46% of the total return of the MSCI China Index was derived from dividends received and reinvested. The significance of dividends has always been appreciated at Matthews Asia, and what may surprise many investors is that Chinese companies have offered both higher yields and higher dividend growth than U.S. firms. A dividend-investing approach, with a focus on both dividend yields and dividend growth, can be an effective investment strategy in China.

Dividends augment investor returns with recurring income streams, which can significantly impact long-term total returns. In the past few years, this phenomenon has been even more pronounced. From 2010 to 2012, the MSCI China Index produced a total return of approximately 6%. If contributions from dividends are excluded, the index would have returned -3%, meaning all positive returns were derived from dividends. While China offers investors much opportunity to tap growth companies, investors may risk overpaying for that growth. And in some instances, an increase in dividend payments may cause an investor to worry that it would lead to a company’s reduced capacity for growth. Nevertheless, if investors specifically seek out cash dividends, they may reduce some of the risk of equity investing by receiving some current income.

A pure dividend yield strategy requires a disciplined investment process with regard to valuations. Research has shown that a strategy of investing in high dividend yielding companies in China would have outperformed the broad MSCI China Index from 2000 to 2011. There is an ever stronger case, to be made, however, in investing for dividend growth of Chinese firms. The total dividend pool as well as the number of dividend payers has expanded with the continuous development of China's capital markets. In 2011, Hong Kong-listed Chinese companies and Chinese firms listed on other major overseas exchanges saw total dividend payments surpass US$72 billion, compared to just about US$8 billion in 1998. Furthermore, the pool of dividend-paying companies increased more than three-fold, from 238 companies in 1998 to approximately 842 companies by the end of 2011.

While China’s market for new stock listings has been sluggish as of late, it is notable that roughly three quarters of the total dividends paid in 2011 came from companies that were listed after 1998.

An Expanding Dividend Pool

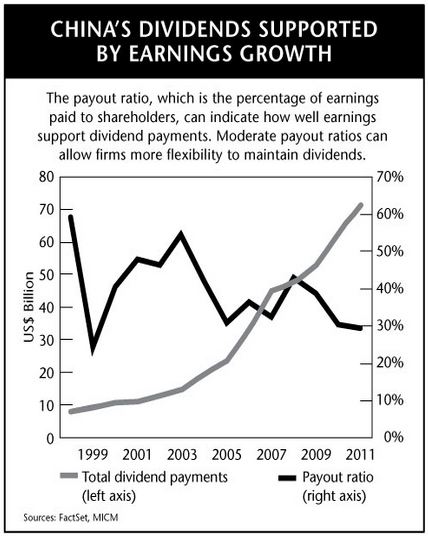

The expansion of China's pool of dividend payers over the past decade has been accompanied by healthy underlying corporate earnings. This is evidenced by a general overall decline in the dividend payout ratio for Chinese companies as a whole.

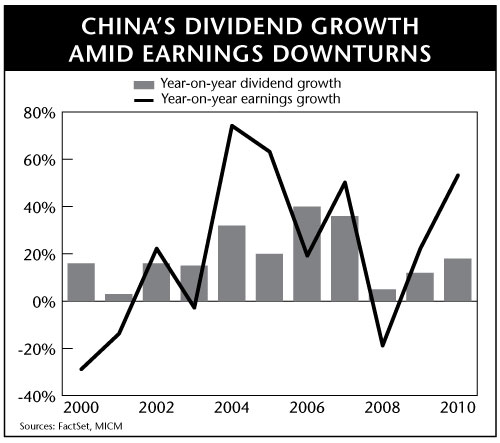

At the same time, Chinese dividend-paying companies still generally maintained conservative balance sheets with low financial leverage. That bodes well for both the sustainability and the future growth of dividends in China, since a moderate payout ratio can allow companies more flexibility to either maintain dividends or increase future dividend payment amounts. Historically, dividends in China have exhibited lower volatility relative to earnings. The chart below shows that since 2000, there were two major downturns that impacted earnings growth for Chinese firms—the first being the dot com crash that started in 2000 and the second being the more recent Global Financial Crisis of 2008. In both instances we saw double-digit earnings corrections while dividends still registered positive growth.

Dividends Can Provide a Corporate Governance Signal

A likely factor behind the endurance of these dividend payments may be the concentrated ownership structure of Chinese companies. Unlike in developed markets, such as the U.S., Chinese companies tend not to have fragmented company ownership. Despite being publicly listed, they are generally still controlled by a single shareholder—be it an original founder or the government in the case of state-owned enterprises (SOEs). Controlling shareholders have various incentives to tap the cash flow of their listed entities, and it is not unheard of for listed companies to loan money to their controlling shareholders or to purchase goods or services from private companies owned by controlling shareholders. By comparison, the dividend payment is one of the few legitimate ways for those controlling shareholders to make a claim on the underlying cash flow. For private founders who have gone public, dividends may be their primary income source. Meanwhile, dividends from listed SOEs, which are often considered “crown-jewel” assets, could be a meaningful source of funding for government spending. Companies that maintain consistent dividend policies send a signal about their approach to corporate governance—an increasingly important differentiator in China—as all shareholders are paid dividends regardless of whether they are majority or minority shareholders.

Dividends may also serve as indicators of a company’s business model strength and force executives to become more disciplined in their investment decisions. And because dividends are cash payouts to shareholders that need to be backed by real cash earnings or existing cash balances, they may be less prone to accounting manipulation. This is especially important for emerging market investors, including those investing in China, where corporate disclosure can often be lacking. As some of the recent high-profile accounting issues involving overseas-listed Chinese companies have shown, one commonality among many companies found to have committed fraud has been the absence of dividend payments. Many companies that were scrutinized did not pay meaningful dividends despite reportedly high revenue growth and lofty margins. On the contrary, many of them had a history of constantly tapping capital markets and raising new money from investors. In this sense, we believe that dividend growth is a better metric than reported accounting earnings growth. A strategy focusing on both dividend yield and dividend growth may lower some of the risks related to corporate governance issues, and can be a prudent strategy for investors considering investments in China.

Perhaps the safest regulatory environments are created when a country has, over a long period of time, grown a culture of corporate governance and regulatory policy that guides corporate actions. China has had a relatively short time in which to develop such market institutions, let alone such a culture. However, a significant trend related to China’s growing dividend universe is its improving regulatory environment. As a recent example, the Shanghai Stock Exchange issued guidance in January to announce that it would give priority to listed companies offering a dividend payout ratio above 50% in such factors as financing, mergers and market access. From the viewpoint of Chinese regulators, this emphasis on dividends promotes longer-term investments in the country’s domestic A-share market, which thus far has been acutely missing, and also may provide better protection for the interest of minority shareholders.

A Diverse Mix

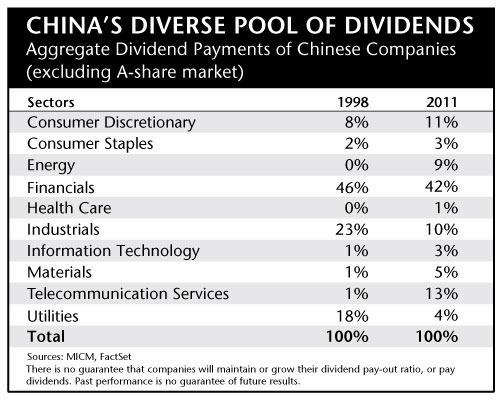

What is also encouraging about the increase in the number of Chinese dividend-paying companies is that the composition of the underlying dividend payers has become increasingly diverse. In 1998, the top three dividend-paying sectors—financials, industrials and utilities—accounted for about 86% of the total. By 2011, those sectors accounted for 66%. Financial firms were still the top dividend payers, but comprised a smaller 42% weighting. Meanwhile, sectors such as consumer discretionary, energy and telecommunication services all saw their dividends rise considerably.

The shift in contributions from these sectors makes sense as China continues to de-emphasize export-heavy manufacturing and rely more on domestic consumption. Companies in consumer-related sectors should increasingly benefit, and are expected to feature more prominently among the country’s future dividend payers.

With this deeper and broader universe of Chinese dividend-paying companies, investors seeking to capitalize on China's growth are now able to construct a diversified portfolio of companies that pay healthy dividends and have the potential to deliver on dividend growth.

As China pushes forward its capital market reform, dividend investors should be more optimistic about China's future dividend landscape.

Yu Zhang, CFA

Portfolio Manager

Matthews International Capital Management, LLC

The views and information discussed in this article are as of the date of publication, are subject to change and may not reflect the writers' current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of any securities or any sectors mentioned herein.

The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. Matthews International Capital Management, LLC does not accept any liability for losses either direct or consequential caused by the use of this information.

© Matthews Asia