Into this academic but high-staked market fog has stepped another Fed official, this time not a Chairman but a relatively new yet similarly quizzical Governor. Jeremy Stein’s February 2013 speech has not gained the attention that Chairman Greenspan’s did, but it is remarkably similar in its intent and initial question: Governor Stein asks, “What factors lead to overheating episodes in credit markets?… Why is it that sometimes, things get out of balance?” Without mimicking Chairman Greenspan’s phrase, Governor Stein renews the quest, asking nearly a decade and a half later, “How do we know when irrational exuberance has unduly escalated asset values?”

I suppose it’s fair to criticize both queries on two grounds: 1) Although asked by Chairman Greenspan, it was never really answered in the 1996 speech. 2) If the Fed’s so smart, why are some of us still poor? Why did our 401(k)s become 201(k)s in 2009 before recovering to near peak levels currently? If they’re so smart, why the roller coaster ride, the 30% decline in home prices since 2006, and our current 7.9% unemployment rate?

Well to answer for the absent Chairman and the necessarily silent Governor Stein, the Fed incorrectly assumed that as long as inflation was benign, and future productivity prospects were near historical proportions, then asset price exuberance was an indirect and much less significant influence on economic growth. The Chairman admitted as much in a public “mea culpa” several years ago. We’re notthatsmart, he seemed to intone. Sometimes we make mistakes. I’m with you there, Mr. Chairman. Sometimes we all do.

So let’s approach this new paper with eyes wide open and pant bottoms close to those mythical musical chairs. Governor Stein’s speech reflects importantly on the answer to the question asked by a recent Wall Street Journal headline: “Is (the) Bull Sprint Becoming a Marathon?” Is there indeed “A Boom Time” in markets as the Financial Times queried on the heels of Dell, Virgin Media, and then HJ Heinz?

Governor Stein, as does PIMCO, suggests caution. On a scale of 1-10 measuring asset price “irrationality”, we are probably at a 6 and moving in an upward direction. Admittedly, Stein never ventures into the netherworld of stock market prices or leveraged buyouts. He appears to know better. What he does stake claim to however is a thesis for high yield spreads with the implication that other credit markets bear similar consequences. His initial starting point is that the pricing of credit isprimarily an institutional as opposed to a household decision making process. Individuals may become unduly irrational when it comes to buying high yield ETFs or mutual funds, but it is the banks, insurance companies and pension funds, to name the most dominant, that influence the price of credit – high yield bonds – and by osmosis, investment grade corporates, municipals, and other non-Treasury risk credit assets. From this initial premise, he then points to recent research by Harvard’s Robin Greenwood and Samuel Hanson that suggests that while credit spreads are helpful future guides, that anon-price measure – the new issuevolume (and perhapsquality ) of high yield bonds – is a more trustworthy input. To quote: “When the high-yield share (of issuance) is elevated, future returns on corporate credit tend to be low.” And because of financial innovation and easier regulatory changes, institutional buyers such as banks, insurance companies and pension funds tend to match the mountains of issuance with an exuberance that eventually can be labeled irrational. Stein’s bottomline is that recent evidence suggests that we are seeing a “fairly significant pattern of reaching-for-yield behavior emerging in corporate credit.” In fact, investors bought over $100 billion of high yield and levered loan paper last year, a record level even exceeding the ominous levels in 2006 and 2007. Shown below in Chart 1 is a history of CLO issuance, admittedly a subset of high yield, but one which illustrates the supply pattern Governor Stein is leery of.

Now at this point, I suppose readers expect yours truly to jump all over the Governor’s speech/premise and to advance my own more learned thesis. Not really. With previously expressed reservations about the prescience of the Fed (or any of us!) I applaud his attempt to answer the initial 1996 question. I think Governor Stein’s speech was a little uni-dimensional, and a little too supply and model driven as opposed to behaviorally influenced, but I liked it, and PIMCO agrees with its conclusion. Corporate credit and high yield bondsare somewhat exuberantly and irrationally priced. Spreads are tight, corporate profit margins are at record peaks with room to fall, and the economy is still fragile. Still that doesn’t mean you should vacate your portfolio of them. It just implies that recent double-digit returns are unlikely to be replicated and that when today’s 5-6% high yield interest rates are adjusted for future defaults and recovery values, that 3-4% realized returns are the likely outcome. Just this past week the Financial Times reported that global corporate default rates are inching higher just as companies with fragile balance sheets sell large amounts of debt. Don’t say Governor Stein didn’t warn you.

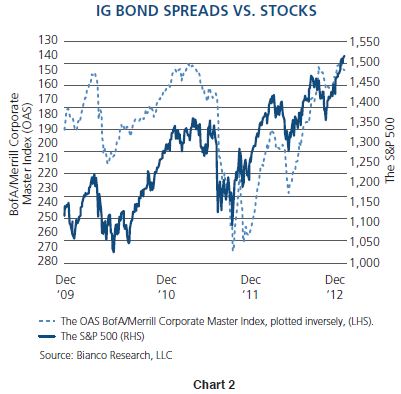

But I would step now into the forbidden territory of equity pricing by presenting additional historical correlations compiled by Jim Bianco of Bianco Research – admittedly not a thickly populated academically staffed organization like the Fed, but a well-regarded one nonetheless. He points out in a recent daily release that high yield and corporate bonds are really just low beta equivalents of stocks. It appears that they are. The following charts show a rather commonsensical negative correlation of high yield spreads (and therefore future high yield returns) to stock prices.

The conclusion would be that where high yield prices go, stock markets follow, or vice versa. Narrow yield spreads in high yield credit markets appear to be accompanied by “narrow” equity risk premiums in the market for stocks, which is another way of saying that the course of future equity returns may not resemble its recent exuberant past. 3-4% high yield returns over the next few years? Why shouldn’t that logically lead to a generalized 5-6% return forecast for stocks? Admittedly, returns for both high yield and equity markets have been unduly influenced in the past few years by Quantitative Easing, the writing of trillions of dollars of Federal Reserve checks and the exuberant migration of institutions and households alike to the grassier plains of risk assets dependent on favorable economic outcomes. It is what central banks encourage and to date it has been successful. If and when that support dissipates or if the economy remains anemic, investors should be cautious and temper their enthusiasm.

PIMCO’s and Governor Stein’s “rational temperance,” in contrast to excessive historical bouts of “irrational exuberance,” simply counsels to lower return expectations, not to abandon ship. PIMCO is a global investment manager – not one with a perpetual frown or even an ever-present half empty glass – but one which hopes to provide alpha and above market returns while still standing tall in the aftermath of future irrational bouts of exuberance. We join with Governor Stein and perhaps Alan Greenspan in encouraging not an exit but a reduced expectation. Credit spreads nor interest rates cannot be artificially compressed forever, nor can stock prices rise perpetually on their coattails. Be rational, be optimistic if so inclined, but temper it with a commonsensical conclusion that we have seen something similar to this before, and that previous outcomes seldom matched the exuberance.

IO Speed read:

1) Chairman Greenspan’s “irrational exuberance” speech in 1996 posed an excellent question, and history provided the answer.

2) Fed Governor Jeremy Stein asks the same question in 2013 with a uni-dimensional but useful model.

3) Stein’s paper, accompanied by correlations from Bianco Research, suggests caution in today’s high yield market.

4) High yield bonds, stock prices and other risk spreads move in relative tandem.

5) PIMCO cautions “rational temperance”: be bullish if you want, but lower return expectations on all asset classes.

Past performance is not a guarantee or a reliable indicator of future results. Investing in the bond market is subject to certain risks, including market, interest rate, issuer, credit and inflation risk. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Equities may decline in value due to both real and perceived general market, economic and industry conditions.

The BofA Merrill Lynch High Yield Master II Index is an unmanaged index consisting of U.S. dollar denominated bonds that are rated BB1/BB+ or lower, but not currently in default. BofA Merrill Lynch Corporate Master Index is an unmanaged index comprised of approximately 4,256 corporate debt obligations rated BBB or better. These quality parameters are based on composites of ratings assigned by Standard and Poor's Ratings Group and Moody's Investors Service, Inc. Only bonds with minimum maturity of one year are included. The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index. The S&P 500 Index is an unmanaged market index generally considered representative of the stock market as a whole. The index focuses on the Large-Cap segment of the U.S. equities market. It is not possible to invest directly in an unmanaged index.

This material contains the current opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material is distributed for informational purposes only. Forecasts, estimates, and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2013, PIMCO.

© PIMCO