Despite exceptionally easy monetary policy, inflation risk remains low.

March 15, 2013

- Despite exceptionally easy monetary policy, inflation risk remains low

- Record stock market levels are boosting consumer spending

- U.S. capital spending is poised to be a bright spot this year

I met my wife at the University of Chicago, where we were both undergraduates majoring in economics. Because of that background, we’ve been called the ultimate fun couple. While others are out enjoying movies, we are at home studying supply and demand curves.

To receive our diplomas, we had to sign a pledge promising to defend the price level always, and everywhere. Milton Friedman was at his zenith back then, and Paul Volcker was just starting the Federal Reserve’s efforts to tame inflation with strict control of the money supply. Initially painful, those efforts ultimately proved successful. Current Fed Chairman Ben Bernanke has called it most significant achievement in the Fed’s nearly 100 years of existence.

So I was a little troubled recently when I was accused of not taking inflation seriously. Granted, I do not devote many slides to the topic in my standard deck, mostly because there seem to be so many other pressing topics. But to some, the unprecedented ease introduced by central banks will inevitably lead to a situation where too much money is chasing too few goods.

So it seems appropriate to address this apparent shortcoming of perspective with a discussion of where inflation is, and where it might be going. With central bank meetings in Europe just past, and the next meeting of the Federal Open Market Committee (FOMC) on the calendar next week, the timing is opportune.

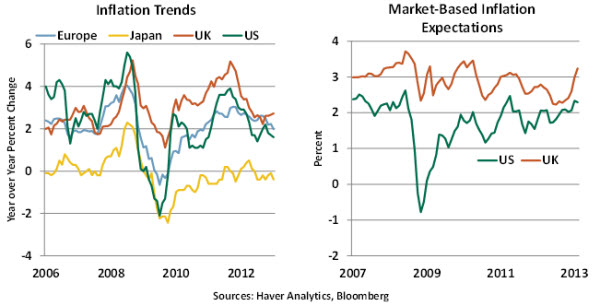

Inflation has generally been trending down in the world’s major economies. Recession in some places, and slow growth in others, has reduced aggregate demand and created significant amounts of excess capacity.

In the United States, inflation is comfortably below the Federal Reserve’s targeted level. In Europe, inflation is running slightly above central bank guidelines, but soft economic conditions are expected to bring prices back down to within an acceptable range before long.

My first macroeconomic class stressed, however, that expectations of inflation were potentially more pernicious than inflation itself. U.S. inflation expectations remain pretty well-anchored, as measured by trading in inflation-protected securities. Inflation expectations in Britain have jumped in the past two months in anticipation of another round of quantitative easing there.

Viewed from the bottom up, it seems difficult to find a formula that would create much faster inflation anytime soon. Labor costs are a dominant portion of production costs, especially for service industries. With un- and underemployment elevated in many countries, wage growth has been very slow and will likely remain in check for a considerable period into the future. Further, most commodity prices are lower today than they were a year ago, and firms do not have the pricing power that they did before recession set in.

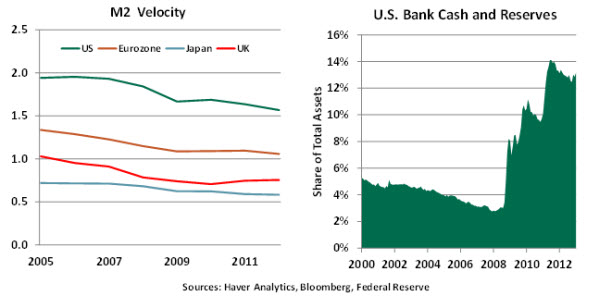

But it is the top-down view that seems to trouble many observers. From this perspective, combing through the components of price indexes to find upward pressure is fruitless; focusing on the money supply is the key. A look at recent trends is cause for some concern; M2 in the United States has risen by 7.5% over the past twelve months, while the money supply in the United Kingdom has risen by more than 6%.

Yet the potential of increases in the money supply to pressure the price level may be limited by reduced levels of “velocity.” Roughly speaking, velocity is the frequency with which money turns over in an economy. The more turnover, the more likely it is that a given increase in liquidity from the central bank will stress the price level.

The velocity of money in major markets has fallen sharply in the past several years. This is due in no small measure to the fact that banks are holding on to more cash than they normally do. Almost half of the money injected by the Federal Reserve into the U.S. economy sits idle on bank balance sheets. These balances have been slowly working their way down as bank lending expands, but the Fed can slow the pace of credit expansion if it ever needs to by raising the rate it pays to the banks on excess reserves.

Further, the link between money and inflation was never perfect, and it has frayed over the years. Some of this has to do with the challenge of defining money and distinguishing liquid funds from investments. (The more liquid forms of money are thought to be fuel for inflation.) As inflation is a global phenomenon, with goods and services sourced from all over the world, looking at the money/inflation relationship country by country may not tell the full story.

None of this is an ironclad guarantee that inflation won’t escalate at some point in the future. Central banks have pledged to remove their accommodation when economic conditions have shown sufficient improvement. Timing and executing this strategy will not be easy, leaving the risk that too much money will remain out in the system for too long. But the ethic of price-level control, forged amid challenging circumstances a generation ago, remains exceptionally strong within the world’s central banks.

There’s an old joke in economics about a graduate who returns to college for a 30th class reunion. Stepping into the classroom of a favorite macro professor, the graduate notices that the final exam for the class is based on the same questions that had been posed to him years before. “Ahhh…” the professor says, “But the answers have changed.”

The tests facing central banks are the same as they were a generation ago. But in answering the questions facing them, monetary authorities must concede that the appropriate responses may not be the same.

The Wealth Effect Returns

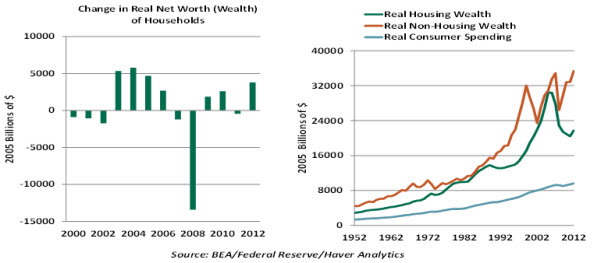

Last week the Federal Reserve published its Flow of Funds report, which includes an estimate of household net worth. This quantity shot up $5.5 trillion to $66 trillion during 2012. Household wealth is within reach of matching the all-time high set in 2007.

This is an encouraging development in itself, but it promises to help economic growth through the “wealth effect.” The wealth effect is the change in consumer spending due a perceived change in wealth of households, and it may serve to explain why recent consumption readings have been unexpectedly strong.

Understanding the impact of the wealth effect requires breaking it into two components. Household wealth is composed of home equity (market value of owner-occupied homes and residential rental property, net of mortgage debt) and non-housing wealth (net financial assets). Housing wealth posted a gradual increase for much of the post-war period until a sharp gain commenced in 1997. It was soon followed by a historically large decline, and a slow recovery is underway now.

Non-housing wealth has registered noticeably large movements since the early 1990s after nearly four decades of steady climb. The financial crisis brought a significant correction, but virtually all of that lost ground has been regained.

Research indicates that the sensitivity of consumer spending to changes in housing wealth and non-housing wealth are different. Every dollar of housing wealth is estimated to lift consumer spending between 3 cents and 6 cents, while every dollar of non-housing wealth would increase consumer spending 2 cents.

Adjusting for inflation using the personal consumption expenditure price index, real housing wealth and real non-housing wealth advanced $1.3 trillion and $2.5 trillion, respectively, during 2012. Based on the estimates cited earlier, real consumer spending should move up roughly $76 billion – $128 billion in the quarters ahead due to the increase in wealth. This represents a boost of roughly 0.5% ¬– 1.0% to gross domestic product (GDP) growth.

Federal Reserve officials have highlighted in recent remarks that improved equity markets are due, in part, to very accommodative monetary policy. The wealth effect can therefore be considered as another dividend of quantitative easing, and should be considered as part of the cost-benefit analysis of the program that the FOMC will undertake at its meeting next week.

These calculations should not be used to establish precise changes in consumer spending. They are, at best, empirical guidelines for thinking about the relationship between changes in wealth and consumer spending. Yet the recent increase in wealth augurs positively for consumer spending in the quarters ahead, and it is an important tailwind in an environment of fiscal austerity.

Capital Spending Gathers Strength

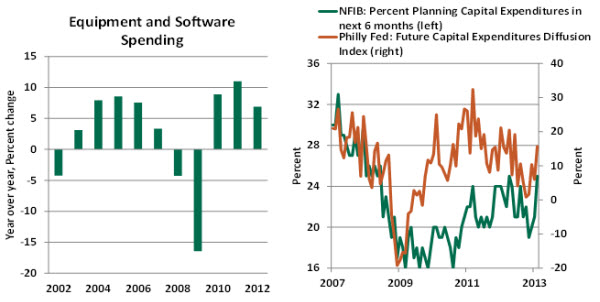

The Great Recession established several ignominious economic records, among them the 22% reduction in capital spending, the largest during recessions of the post-war period. Business spending on equipment and software started to recover in 2010, but posted slower growth in 2012. In the past two decades, capital spending made up roughly 7% of GDP; in the last two years it has averaged 8.2%, ranking as one of the top contributors to growth. Recent readings present a convincing case for strong growth in capital spending this year.

As shown in the chart below, the Federal Reserve Bank of Philadelphia’s Business Survey results for February indicate firms are optimistic about capital spending in the next six months after a lull in the second half of 2012. The February report of the National Federation of Independent Business also shows an increasing share of small businesses making plans to raise capital expenditures in the near term.

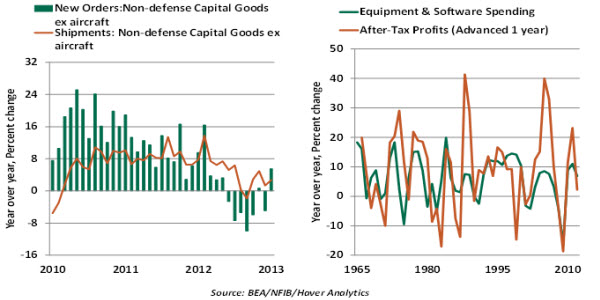

Orders of non-defense capital goods excluding aircraft posted a year-to-year gain in January after a string of declines in the latter half of 2012. Shipments of non-defense capital goods excluding aircraft, a proxy for capital spending in the GDP report, gathered momentum in January. Both of these recent developments paint an encouraging picture for capital spending in the near term.

Economic theory posits that corporate profits are an important driver of investment expenditures, and historical evidence supports this hypothesis (see chart). In fact, the change in corporate profits after taxes leads capital spending. The trend in capital spending in 2010 – 2012 is consistent with this historical relationship. Profit growth in the first three quarters of 2012 points to a strong performance compared with 2011, barring a large decline in the fourth quarter. Based on the lagged relationship between profit growth and capital spending, it follows that capital spending in 2013 should exceed the performance seen in 2012.

A growing economy calls for additions to the capital stock of the economy. Growth of real net capital stock in the economy averaged less than 1.0% in 2010 and 2011, which is weak and significantly below the historical average (+2.6%). Bullish economic numbers of the January – February period and a long economic recovery suggest that a replacement and expansion of capital stock are both most likely to follow soon. Overall, the combination of profit growth and forward momentum of the economy bolster expectations of an increase in capital spending during the rest of the year.

© Northern Trust