- Everyone wants more financial stability, but at what cost?

- More FOMC participants are getting concerned about QE

- Germany’s faltering economy may lead it to support more ECB stimulus

With two teenagers still at home, stability is an elusive ideal. One moment, my children act like mature young adults; the next, their heads are rotating 360 degrees and the things that come out of their mouths are appalling.

On a broader scale, international policy makers have embarked on a quest for financial stability. Whole departments within central banks have been formed to monitor financial conditions and recommend policies to prevent a recurrence of the 2008 crisis. Yet measures designed to ensure stability come with costs and can create unintended consequences.

The goal of financial stability will be a recurring theme in the coming years, and promises to affect just about everyone. To follow the debate about these measures, it is helpful to understand a little of the background before delving into the key points.

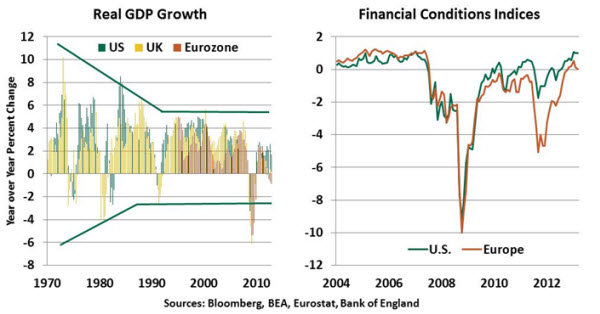

Prior to the crisis, major economies enjoyed a period that became known as “the great moderation.” For 20 years, real GDP growth moved within a narrow range; the U.S. had but two very brief and shallow recessions during that interval.

There was a growing belief that we had become the master of the business cycle. Financial conditions were extremely stable. Risk managers in the public and private sector were hailed for their sophistication, which produced such substantial gains for society.

Once exalted, many of these agents have since been excoriated in the wake of the Great Instability. Market discipline is no longer regarded as sufficient to head off trouble, and so the world is presently engaged in a broad exercise in financial re-regulation.

The Dodd-Frank Act (DFA) in the United States and the U.K. Blueprint for Regulatory reform (among others) aim to prevent a recurrence of 2008. The scope of these measures is far ranging. However well intentioned, though, these new guidelines present challenges for both financial companies and supervisors.

The sheer length and complexity of the new guidelines will take some time for each side to digest. For example, DFA is around 2300 pages, not including the passel of associated interpretations that regulators were directed to produce (and which they are well behind on, given the sheer weight of their new responsibilities).

There is an active debate over whether meticulous approaches like this are too complex for both financial companies and their overseers to apply productively. Andrew Haldane, the Executive Director of Financial Stability at the Bank of England, authored a paper last year that was playfully entitled The Dog and the Frisbee. In it, he argues that simple forms of regulation could have better success in guiding the oversight of financial firms.

A more succinct expression of principles, as opposed to a lengthy list of rules, might better adapt to changing circumstances. And there is scant evidence that complicated rules do a more effective job of deterring misbehavior; the Basel II capital standards are a case in point. For principles to be effective, though, supervisors must be intelligent and consistent as they apply the discretion that such a system would necessitate.

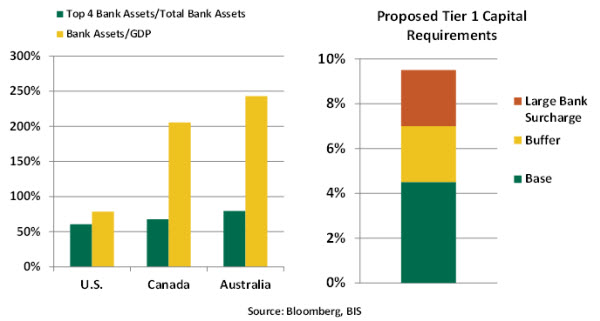

A specific target for re-regulation is the problem of financial institutions that are too big to fail. A small handful of global firms are so large, expansive, and interconnected that prospective failure would be immensely costly to society. Policy makers therefore have little choice but to forestall that outcome and put public money at risk. Because of this implicit backstop, these mega-banks enjoy a funding cost advantage over smaller firms.

Mergers of expedience, made amid the stress of the financial crisis, have actually increased the size of some of the largest banks in the world. This has only added to calls to break them up, potentially by fiat. Yet size is not necessarily a source of instability; Canada and Australia, for example, have highly concentrated banking systems but have not been prone to crises.

Further, the community of very large global firms will be facing much higher capital minima and much tougher regulatory requirements. This may, over time, encourage moderation in their scale and scope. The world’s financial giants are being asked to write “living wills,” that provide an outline for unwinding their operations, should that ever become necessary. And the additional oversight they will be subject to raises the possibility that potential problems can be detected early, before the firms impose costs on the public.

For all the good intentions, there is no guarantee that the rush to re-regulate will be successful. The next crisis may look nothing like the one just past, and the political will to take tough preventative steps during good times cannot be taken for granted.

Further, there is a cost of seeking financial stability that goes beyond the investment in compliance. As it is with stocks, economies that seek a lower variance of outcomes may see their expected performance diminish. Potential new regulation could slow financial intermediation and innovation and thereby reduce prospective rates of economic growth. In this case, the choice of where to aim on the continuum between risk and reward has huge stakes, and consequences for us all.

March FOMC Minutes: Full Employment Mandate vs. Financial Stability

The minutes of the March Federal Open Market Committee meeting reveal a range of opinions about the costs and benefits of the Fed’s large-scale asset purchases (LSAPs). The important takeaway from the minutes is that a growing number of FOMC participants are ready to scale back asset purchases in 2013 as costs are rising relative to benefits.

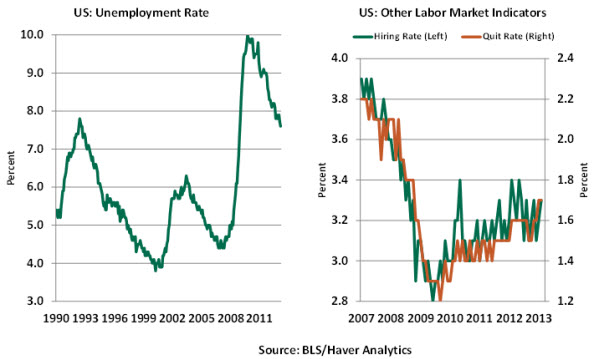

The Fed currently is engaged in an open-ended program to purchase $85 billion in securities each month. The timing of reduced asset purchases or complete disengagement is tied to “a substantial improvement in the outlook of the labor market.” Last week’s employment news was not the most encouraging we’ve received lately, but the broad sweep of labor market indicators reflects important improvement over the past six months.

A pickup in the quit rate would imply that workers have gained confidence they would rehired, while an increase in the hiring rate would suggest business optimism. Overall, an improvement in these rates would denote that demand for labor has strengthened; we are watching these numbers closely because an increase in one month is not a trend.

The long-term cost of LSAPs has worked its way to the center of the Fed’s radar screen. At the March FOMC meeting, staff research addressed the view that the extended low interest rate environment encourages “excessive risk taking that could have adverse consequences for financial stability at some point in the future.” Their findings failed to point to any current imbalances that pose a “systemic risk.” But several sectors “bear watching” and there was clear concern that these risks could grow over time.

The minutes indicate that at one end of the spectrum is a hawkish group that would like to slow LSAPs immediately. At other end, two members believe that purchases should continue at the current pace (or even be increased) for the rest of the year. It is the middle group between the two extremes that is most interesting; they seem to favor a reduction in purchases later this year, and a potential stop by year-end.

For now, the mixed signals from the labor market may defer more aggressive talk of LSAP tapering. Developments in Europe featured in the minutes and remain as one of the factors that present a downside risk to current projections of U.S. economic activity. Nonetheless, the risk that quantitative easing might present to financial stability down the road is an issue that is not going to go away quietly.

Germany: Weak Economic Data Will Tip the ECB’s Hand

The defensive posture of the European Central Bank (ECB) last week amid the deepening eurozone economic weakness is baffling, particularly given that fiscal austerity is in full play across the eurozone and monetary policy is the only game in town. Real gross domestic product (GDP) of the eurozone has contracted for five straight quarters and the unemployment rate is 12%.

The ECB’s actions in the past three years have focused on stabilizing financial conditions through Security Markets Programme, Longer-term Refinancing Operations, and the announcement of Outright Monetary Transactions. Positive developments in aggregate economic data of the eurozone are not visible yet.

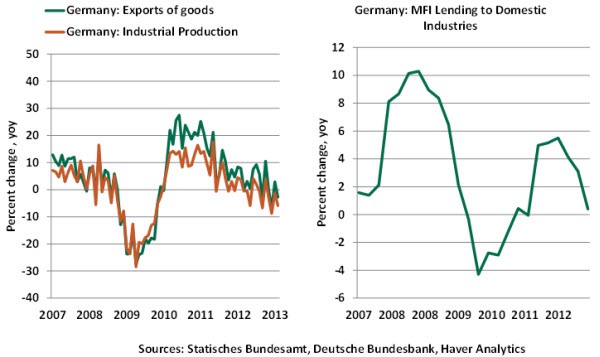

Of the four large economies, the perception is that Germany’s economic performance is on a better footing than its eurozone partners. But a close analysis of incoming economic data from Germany yields a more sober conclusion.

Germany’s real GDP dipped 0.6% in the final quarter of 2012; industrial production has shown five consecutive year-to-year declines. German exports dropped a solid 2.0% in the fourth quarter and the trend shows a sharp deceleration. This reflects the adverse economic conditions of other eurozone members, who are the largest importers of German goods and services.

The Purchasing Managers’ Index of the German factory sector slipped below 50 in March, denoting a contraction in factory activity; the Ifo Business Climate Index edged down in March. Banks account for 80% of financial intermediation in Europe, with capital markets providing the remaining 20%. Credit extension to businesses in Germany is essentially flat versus a year ago, following a decelerating trend. All of these economic numbers are hardly representative of strong growth in Germany in the near term.

Germany has been reluctant about easing monetary policy further, which is largely due to German preoccupation with inflationary threats. On the inflation front, German and eurozone inflation are running at 1.8% and 1.7%, respectively, for the last 12 months. This is down from 2.4% and 2.6%, respectively, a year ago. These favorable inflation numbers and weak economic data could reduce German resistance to additional monetary policy accommodation at ECB meetings in the months ahead.

© Northern Trust