Over the past 20 years, Asia has come a long way to evolve into an asset class in itself. China and India have famously led the way as symbols of emerging nations. But when I think about seeking growth in Asia, I am particularly drawn to the region’s smaller equity markets as attractive hunting grounds for investment opportunities. Asia continues to change at a rapid pace, and this change is not restricted to China’s ever-changing landscape, but to many other areas that may see fewer media headlines.

I have spent considerable time in these markets, with more frequent trips in recent years, and with each visit, I always detect increased economic activity on the streets. Sometimes changes come in the form of that which is missing rather than new elements added. For example, during my last visit to Sri Lanka in December, I was surprised to see that the heavily armed guards found at most major hotels and office buildings were all gone. They had long had a common presence at these venues even up until my prior visit six months earlier because of extra safety measures still in place since the end of the 26-year civil war in 2009.

In the Cambodian capital of Phnom Penh, it seems that with every time I return, the boulevards are tidier, the riverwalk cleaner and more beautification efforts are underway.

Thailand is another country that has undergone an impressive transformation, even amid much political turmoil. This slow-moving economy has surprised many investors as its nominal GDP has nearly tripled to US$346 billion in the past decade. Further to the south, Indonesia, with its favorable demographics, is another nation that global investors have recently come to consider a stock market darling. How have these changes come about? There are two main factors in my view: rising disposable income and increased investment from both foreign direct investment (FDI) and remittances from those working overseas.

Increased FDI flows into emerging Asian economies have been driven largely by production in China moving to lower-cost areas in the region due to rising wages. Multinational companies as well as Chinese and Korean manufacturers have stepped up investments in Southeast Asia to take advantage of its abundant pool of low-cost, yet skilled, labor force. Rising FDI and better government efforts to shore up infrastructure in big cities are helping to pull many out of poverty and enrich lives. This is a common phenomenon happening throughout Southeast Asia. These improvements, in turn, are spilling over to less-developed neighboring countries that are considered Asia’s “frontier” economies. Vietnam is a good example of this as some multinational high-tech manufacturers have turned to the country recently, investing billions to set up testing facilities and factories there.

In terms of remittances, the Philippines surpassed Mexico last year in terms of the amount of money its more than 8 million overseas workers send home. Official remittances sent to the Philippines were projected to reach over US$24 billion for 2012, according to the World Bank. Mexicans living abroad were projected to send back just under US$24 billion and the top two countries for remittances were India and China at about US$70 billion and US$66 billion, respectively for 2012.

The Asian Frontier

Many of the region’s so-called frontier markets, including Bangladesh, Mongolia, Pakistan and Sri Lanka, are marked by lower GDP of generally under US$250 billion and equity market capitalization of under US$50 billion—though not all of them have functional, liquid stock markets yet.

Many countries—including Cambodia, Laos, Vietnam and Myanmar—are members of the Association of Southeast Asian Nations economic bloc. Bangladesh and Pakistan are part of the Indian sub-continent and then there are some outliers like resource-rich Mongolia.

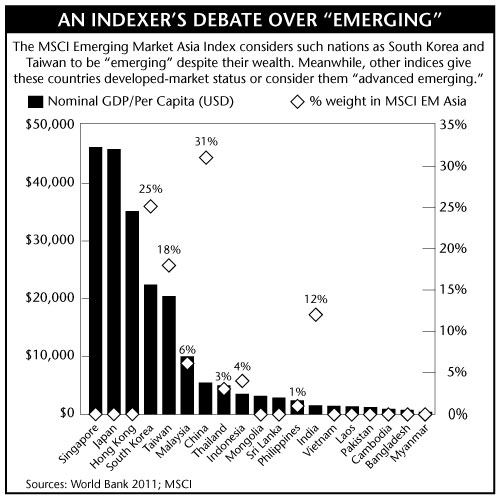

I am frequently asked how to define “emerging Asia,” and the answer is that there are several different interpretations from the equity investment point of view. According to MSCI Emerging Markets Asia Index, emerging Asia includes South Korea and Taiwan. However, these economies seem to me to have already emerged. I would argue that they are in a different league from countries such as Indonesia or Thailand. Meanwhile the FTSE Emerging Market indices promoted South Korea to developed-nation status in 2008 and more recently placed Taiwan on a watchlist for possible promotion from “advanced emerging” to “developed.” This may not sound like a debate for the average investor, but given that billions of dollars are indexed to such benchmarks, the distinction may matter more than one might think.

The labels of “frontier,” “emerging” and “advanced emerging” are more or less shades of the same idea. I don’t believe there should be so much emphasis on this delineation when it comes to investing in the companies of Asia’s lesser developed areas. After all, countries classified as part of emerging Asia today were all recent graduates of Asia’s “frontier” camp.

Even with GDP per capita commonly used to categorize countries, this metric alone can sometimes be misleading in gauging the development of a particular segment of a country. A nation’s promising economic growth alone does not always mean good performance of a particular market. Consider, for example, the retail sector in India or China. Retail competition in these countries is so strong that returns on investment may not be as high as macroeconomic data may suggest. My point is that each investment idea must be carefully examined before investors commit. The same investment disciplines should be applied to determine a firm’s real return on investment and growth potential.

Considering GDP growth alone as a metric can be tricky as we see all the time in the case of China. China’s developed coastal areas can be more than three times as wealthy as its rural segments. In fact, China as a whole is difficult to assess based on the yardstick of GDP per capita. On the one end you have such modern provinces as Shanghai, which has an equivalent GDP to Finland. At the other extreme, you have Hainan, which has a GDP equivalent to that of Kenya.

Because stock markets in Asia’s smaller economies tend to be overlooked by global investors, they are primarily driven by local retail investors. We tend not to see local institutional investors in these markets as they are still young. In fact, the stock exchanges in Laos and Cambodia only opened in 2011.

Why Consider Emerging Asia Now?

While no one can ever know the best timetable to start investing in a region, the time seems ripe to explore new growth companies in Asia’s truly emerging countries. Former U.S. writer, political scientist and diplomat Henry Kissinger once described Bangladesh as a “basket case.” I lived there for two years in the mid-1980s and believe that Kissinger was correct in this assessment back then. But I believe he would surely be impressed if he could see how things have changed. Bangladesh’s annual per capita GDP growth has been averaging about 5% over the last 10 years and has seen strong growth in the last few years (compared to flat growth in 1970s). The size of its economy itself stands over US$100 billion today. The rapid growth of Bangladesh’s garment industry has been a key economic driver for the country. Many factories were relocated from China to tap attractive opportunities in Bangladesh and its vast pool of laborers. What set Bangladesh and other Asian frontier countries apart from such markets in other parts of the world is the ability of its workers to have upward mobility. An appreciation for education and a strong work ethic are evident throughout much of Asia. This has led to economies developing around more than just low-cost exports. Export products range from basic goods such as textiles, footwear and garments to more sophisticated, higher cost manufacturing including technology and electronic products. An executive in Dhaka recently noted that he felt companies in Bangladesh had a competitive advantage in producing generic drugs because its pharmaceutical firms could attract many well-qualified engineering graduates from leading local universities for lower wages than Indian pharmaceutical firms could.

To be sure, the Dhaka Stock Exchange Index has seen its fair share of volatility over the last few years. Having marked a 83% rise in the Index in local currency terms, Bangladesh was one of the world’s top-performing stock market in 2010. It had also returned 63% in local currency terms in 2009. However, with unsustainably high valuations, the Index has fallen by more than 50% since its peak in December 2010.

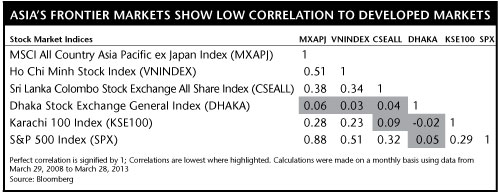

It is often pointed out that emerging markets bear little correlation to other more developed markets despite the fact that this correlation is higher today than it was years ago. Globalization is happening even in the frontier markets, yet their basic economies are still quite locally oriented so this lower correlation does not appear as if it will change in the near future.

Volatility has also been a factor elsewhere in the region. Sri Lanka’s stock exchange showed a strong rally in 2009 following the end of its 25-year old civil war, and was up 125% in local currency terms in 2009 and 96% in 2010. It has since returned to more reasonable levels over the past two years. Vietnam has been one of the world’s most volatile markets over the past four years due to extremely high credit growth and slow government reforms. However, so far this year, it has been among the region’s better performing stock markets. My sense is that these markets have undergone a learning curve from which local investors may continue to benefit.

A Selective, Bottom-Up Approach

During my time traveling and investing in Asia’s frontier countries, what I have found is that Matthews’ bottom-up stock picking approach serves this market well. In what are still largely inefficient equity markets, identifying the most attractive opportunities requires taking the time to understand the local economies and researching companies on-the-ground.

Vietnam is a good example. Here we have a US$40 billion market that limits foreign shareholder ownership to 49%. Historically, retail-driven small markets have been volatile and Vietnam has been no exception. As with other similar markets, Vietnam has been highly volatile because of its low liquidity and the absence of long-term investors. The majority of foreign investors in Vietnam are attracted to many of the same large-capitalization stocks. Our approach, on the other hand, is to seek good smaller and mid-size firms in which we can invest with a long time horizon. Since Vietnam restricts foreign investments, capacity for index stocks, such as banks and utilities, tends to be oversubscribed.

Despite the challenges of investing in some emerging Asian economies, their rapid growth together with favorable demographics, increasing consumer wealth and lower labor costs have all supported a deepening of capital markets in recent years. A bigger universe of publicly traded firms offers investors what we believe are new opportunities to gain exposure to fast-growing companies in what are still relatively inefficient markets.

Taizo Ishida

Portfolio Manager

Matthews Asia

The views and information discussed in this article are as of the date of publication, are subject to change and may not reflect the writers' current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of any securities or any sectors mentioned herein.

The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. Matthews International Capital Management, LLC does not accept any liability for losses either direct or consequential caused by the use of this information.

© Matthews Asia