The two Asian giants have a challenging year ahead

May 24, 2013

- The two Asian giants have a challenging year ahead

- The Fed will be challenged to keep the bond market under control

I’m filing this week’s report from China, at the conclusion of two weeks in Australia and Asia. The conversations have been excellent and provide a great ground-level perspective on what’s going on in the world’s fastest-growing region. And the food has been excellent, from paella in Balnarring to xiao long bao in Hong Kong.

Here are a few random thoughts that have arisen during my trek.

- There may not be a currency war going on, but the relative value of currencies occupies a lot of attention.

My personal search for yield has ended. Australia is a AAA-rated country that has enjoyed 21 consecutive years of gross domestic product (GDP) growth and offers 2.5% on a two-year government bond. Strong investor interest has replaced commodities demand to keep the value of the Australian dollar unusually strong. (I had to mortgage my house to buy a bottle of water upon arrival in Melbourne.)

The Reserve Bank of Australia cited the strong currency in its recent decision to cut rates, but it was too late to prevent Ford from announcing a gradual closure of its operations Down Under. Currencies that are too strong make domestic production uncompetitive, leading countries to contemplate competitive devaluation of their currency.

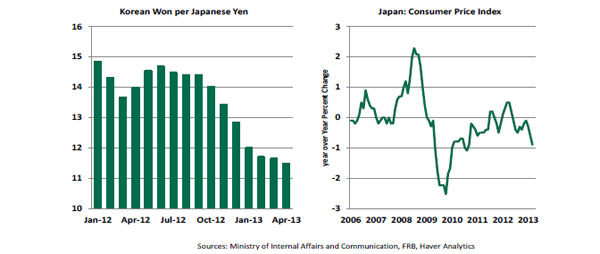

- Japan’s press to kick-start its economy is unnerving its neighbors.

The U.S. dollar now exceeds 100 yen, and the appreciation of other currencies has been even more pronounced. Korean producers are not happy that their direct competitor in the car and electronics markets has gained a 20% pricing advantage since last fall.

Japan’s stated goal of reaching a 2% inflation target is going to be a challenging one to reach. With lots of capacity in world factories, high levels of global unemployment and energy prices retreating, the Bank of Japan is trying to lean against some very strong winds. And should they succeed, the cost of supporting their enormous levels of government debt could create a real budget crisis.

Concerns over the success of Japan’s outline led to a sharp decline in the Nikkei 225 index this week, a reminder that a positive outcome there is by no means assured.

I still take the high road on the currency war issue. Countries that are cutting rates or conducting quantitative easing are attempting to spur GDP growth, which should be good for everyone. And I don’t think that any but the very largest central banks will succeed in depressing their currencies, should they choose to try. But this is an issue which may become more contentious before it calms down.

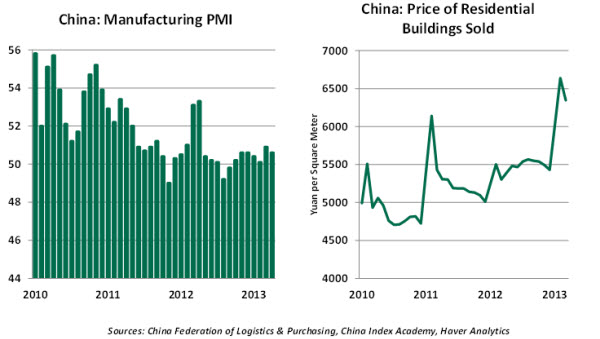

- China’s property markets present policy-makers here with a difficult choice.

By all accounts, prices are rising more rapidly, fueled by debt granted through banks and the growing “shadow” financial sector. In order to curb the enthusiasm, a series of measures has been tried: increased down payment requirements, property transactions taxes and bans on the purchase of second homes.

While fears of excess remain, China also needs a way to enhance its economic growth. Chinese manufacturing has been limited by slow growth of export markets and stiffer competition from other producers. And this week’s release of detail behind China’s 2012 GDP suggests that consumerism has yet to take up the slack.

So officials have dropped some of the tough housing talk and may be willing to let the bubble inflate just a little bit longer. This risks creating a deeper pool of troubled credit.

In sum, the two heavyweights of the region are both facing uncertain transitions. And the economies which are linked closely to them are watching with bated breath.

- The discussions over the past two weeks only deepened my sense that the United States has a lot to learn when it comes to retirement plans.

The two factors which can lead long-term investment plans astray are insufficient contributions and improper asset allocation. There is a considerable body of research that suggests that the average citizen puts aside far too little and lacks the expertise to make the most of investment returns. Public regimes that depend on consistent contributions from legislatures are vulnerable to cyclical swings. And politicians are focused on their next election, a time horizon that is mismatched with the horizon covered by the plan.

Countries in this area of the world have taken some interesting approaches. Australians are required to set aside 9% of their pay (soon to rise to 12%) for a “superannuation” fund, providing substantial seed money. The Chinese also require mandatory contributions from employees. Other governments have created funds with significant amounts of capital quite apart from the general ledger in order to defease obligations for retirement income.

The U.S. Social Security system is confined to investing in Treasuries, has not been adequately funded by the government and is, therefore, facing tremendous long-term shortfalls. Many local government plans are dramatically underfunded. And the defined contribution plans available in the private sector are often not used effectively by those who will be relying on them. Some new thinking might be welcome.

During my journey, I was confronted with a variety of weather conditions, ranging from Melbourne’s autumn chill, to Singapore’s choking humidity, to a black rain warning in Hong Kong. It seems as if the economic climate in this part of the world is shifting around a lot, too.

Bernanke Hints at QE Tapering

Federal Reserve Chairman Ben Bernanke’s testimony at the Joint Economic Committee this week had four important elements: cautious optimism about the economy, benefits of the Fed’s easy monetary policy stance, focus on the labor market and dovish inclination about the course of monetary policy.

Financial markets have been eagerly awaiting guidance about asset purchases, given recent comments from several Fed officials about tapering of asset purchases. Bernanke’s prepared testimony about asset purchases was neutral. However, in the Q &A session, he noted that a reduction of asset purchases is possible in the “next few meetings” if economic data suggest that the labor market improvement is sustainable.

Bernanke’s strong concern about the labor market is evident in this passage:

“Despite this improvement, the job market remains weak overall: The unemployment rate is still well above its longer-run normal level, rates of long-term unemployment are historically high, and the labor force participation rate has continued to move down…. High rates of unemployment and underemployment are extraordinarily costly…”

The minutes of last Federal Open Market Committee meeting, published May 22, are consistent with Chairman Bernanke’s view.

“Most observed that the outlook for the labor market had shown progress since the program was started in September. But many of these participants indicated that continued progress, more confidence in the outlook, or diminished downside risks would be required before slowing the pace of purchases would become appropriate.”

Bernanke also touched on the risks of financial instability if low interest rates are maintained for too long and reassured that the Fed is monitoring this closely. At the same time, in his opinion, “…a premature tightening of monetary policy could lead interest rates to rise temporarily but would also carry a substantial risk of slowing or ending the economic recovery and causing inflation to fall further.”

Despite these dovish-sounding messages, the U.S. Treasury bond market seemed to draw the opposite conclusion. The 10-year Treasury note yield exceeded 2% late in the week, a response to the bullish incoming data and expectations of a reduction in asset purchases by the Fed.

To be sure, the monthly gain in payroll employment is averaging a little above 200,000 in the last six months compared with an average of 130,000 in September 2012 when the third round of quantitative easing was announced. This is a distinct improvement. But layers of joblessness remain very high, prompting key Fed voters to hope for better.

We continue to think that a tapering of asset purchases is possible within the next six months. It will certainly require some additional momentum in the job market and may ultimately be based more on fear that too much QE could kindle financial instability down the road.

What this week illustrates, though, is the market’s sensitivity to even the hint that policy will be changing. The Fed will have to manage this perception carefully to prevent an overreaction.

© Northern Trust