- Is central bank communication clarifying or confusing?

- The European Central Bank should focus its efforts on small business lending

- A look beneath the surface of housing proves revealing

I’ve been awfully busy lately, but I was able to get out early one afternoon in early May to watch my daughter play a junior-high soccer match. It was a wild affair; the lead changed hands three times before ending in a 4-4 draw. My daughter had mixed success: she whiffed on a clearance that led to a goal against but atoned with a clever pass that earned her an assist.

At home afterwards, she asked the question that all soccer dads dread: “Do you think I could play in the World Cup someday?” Quickly, I had to find words that appropriately combined cheer, candor and conditionality. I came up with, “If you keep working hard at it, we’ll see what happens.” A brilliant escape, if you ask me….

It strikes me that central bankers are presently struggling to find the right combination of cheer, candor and conditionality as they signal their impressions to the markets. Recently, the Federal Reserve and the Bank of Japan offered messages that have baffled some observers and frustrated others.

While some long for the days when veiled secrecy, enforced consensus and obfuscation dominated monetary messaging, I am not one of them. Followers have to recognize that managing an economy is an imprecise exercise, and reasonable people can often disagree about the right course. Nonetheless, policy-makers must take care to realize that the importance of their utterances is magnified when strategy reaches a transition point.

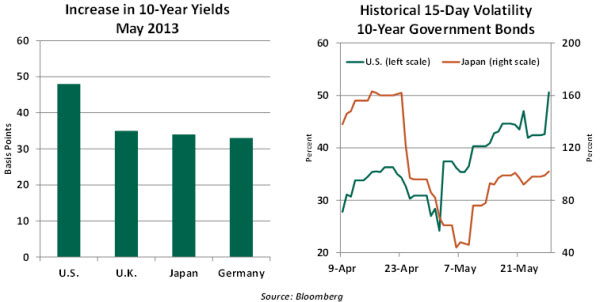

It has been an unsettled few weeks in the world’s bond markets. The catalyst for rising rates and renewed volatility has been some uncertainty over the future course of monetary policy in key countries.

It has been challenging to get a firm fix on what the future holds. Federal Reserve officials have offered mixed messages on the possible tapering of quantitative easing (QE) in the United States. Minutes from the Bank of Japan’s most recent meeting revealed some disharmony over the appropriate course of its stimulus program. And in the U.K., the Bank of England has been cautious with its signaling until incoming Governor Mark Carney takes his place in July.

All three central banks have engaged in QE, the program of bond buying that attempts to influence long-term interest rates. Since the world’s fixed income markets are vast, direct purchases by a central bank must be augmented with statements that help to steer expectations. While monetary authorities have direct control over short-term rates, managing the other end of the yield curve requires suasion to achieve the desired end.

Communication strategies for central banks have been the subject of a lot of study. The promise to keep rates low for a time has certainly helped to keep yields in check for most of the past several years. But matters can get dicey when the magnitude of policy programs is on the brink of change. With the Fed contemplating a tapering and Japan promising an acceleration, the markets will naturally wonder how much and when.

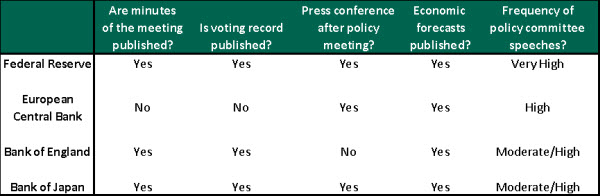

Getting the right point across is both easier and harder than it used to be. When I started in banking, central bank operations were shrouded in mystery and often not apparent for several weeks. Today, monetary authorities provide a plethora of information. Minutes, press conferences, forecasts and speeches can all be used to impart direction. The table below summarizes how the world’s central banks employ each of these practices.

So there is a lot more information out there than there used to be. But it isn’t always completely consistent. At policy inflection points, it isn’t unusual to find participants in the process disagreeing with one another, providing markets with a range of views and leaving investors to speculate over who is in the ascendance.

Further, central banks no longer signal their actions as directly. Instead, they provide a framework for their decision-making, such as the Fed keeping policy accommodative until the outlook for labor markets improves. In some cases, these decision rules are quantified, but different voices may express different estimates of what constitutes success.

When there is dissonance, this can be very unsettling to markets. Investors in U.S. securities, as they try to limit the bond price losses that would result from rising rates, are acutely sensitive to the potential that Fed policy may soon change. Those following Japan are trying to set strategy in anticipation of a substantial quantitative easing effort where specifics are not yet clear. European investors are wondering what more Mario Draghi might do and also what the Bank of England might do under new management.

Yet these kinds of uncertainties are not new to central banking. They’ve always been present, but until recently they were debated more privately. For my money, decision rules, and forecasts are much more revealing than opaque statements that require weeks of parsing. And respectful disagreement is the sign of a healthy decision-making process, not a weak one.

Our view is that the recent backup in global yields is probably overdone. A glut of global capacity is one of several factors that should keep inflation in check. And the weight of central bank action still leans decisively toward easing. Still, this month’s trading reveals the fragile nature of current markets, which will require careful handling to avoid a disorderly reversion.

Important turning points can invite volatility. I’ll certainly be facing that at home, as my daughter moves on to high school next year. Crafting a successful communication strategy in that arena will continue to be quite a challenge.

European Central Bank Meeting: Choosing the Right Tool

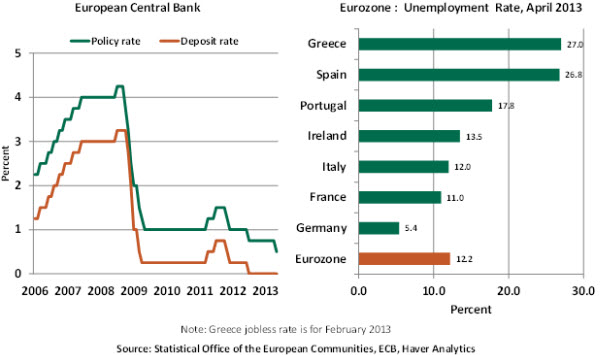

The Governing Council of European Central Bank (ECB) gathers on June 6 for monetary policy deliberations. Given the increase in the eurozone unemployment rate to 12.2% in April, a persistent contraction of credit and contained inflation, the ECB should take suitable steps to mitigate a further deterioration of the already-weak economic situation.

The ECB lowered its policy rate 25 basis points to 0.50% at the May meeting. ECB President Mario Draghi’s remarks at the press conference afterward implied that the door is open for further easing of monetary policy.

Draghi mentioned other policy alternatives that could mend the eurozone economy. A new way of funding small- and medium-sized enterprises (SMEs), particularly in the periphery, was one of the options. He also indicated that the ECB was open-minded about a negative deposit rate.

Starting with the conventional option, many expect another reduction in the policy rate to 0.25%. Draghi noted that some members would have preferred a larger easing in May, which raises expectations of action this time around. However, the impact of this choice will improve if it is combined with better access to credit.

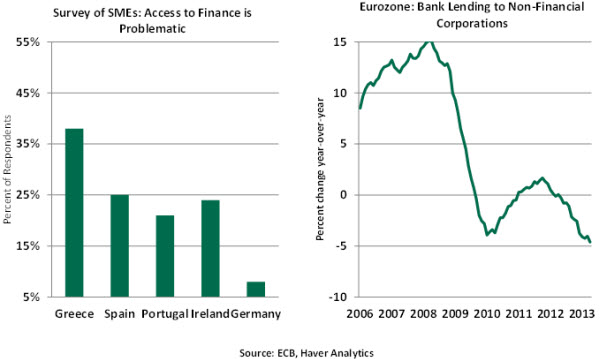

Tight financing conditions for SMEs in the periphery are a major concern. According to the European Commission, SMEs provide two out of three private-sector jobs in the European Union and contribute to more than half of the value-added by businesses. Without access to capital, this sector will be hindered in contributing to recovery.

The April 2013 survey on access to finance of SMEs in the euro area showed a wide divergence among members. As shown in the left-hand chart below, businesses in the periphery are significantly more inhibited. And overall lending in the eurozone has been hindered by the challenged condition of some of the area’s leading banks.

The ECB has broadened its collateral framework as the crisis has unfolded. It may be unwilling to take on more risk by accepting SME loans as collateral, but it may be more open to providing favorable terms for loans to the European Investment Bank, which in turn could be extended to regional banks that extend loans to SMEs. Draghi alluded to this sort of plan in May. A concrete articulation of this program is possible as an outcome of next week’s meeting.

Banks in the eurozone stopped earning interest on deposits at the ECB in July 2012. There are different points of view about the net impact of a negative deposit rate. Advocates argue that a negative rate would compel bankers to lend money. But, if banks are not lending at a zero rate, it is not clear how a negative rate would change counterparty risk assessments.

Critics also hold the opinion that banks already starved of capital would face additional stress if the ECB institutes a negative deposit rate. Strong banks would reduce deposits at the ECB and drain liquidity. Some computer systems may have difficulty with the negative rate. Our view is that Draghi will most likely report that the Governing Council is still weighing the costs and benefits of a negative deposit rate.

At the extreme, even if the ECB can live with the unintended consequences of a negative deposit rate, it is not a growth initiative that can transform an economic bloc that has registered six straight quarters of economic stagnation. A lower policy rate and a program to ease access of finance to SMEs stand a better chance of success. We’ll certainly be listening for more clarity on the timing and design of such an effort.

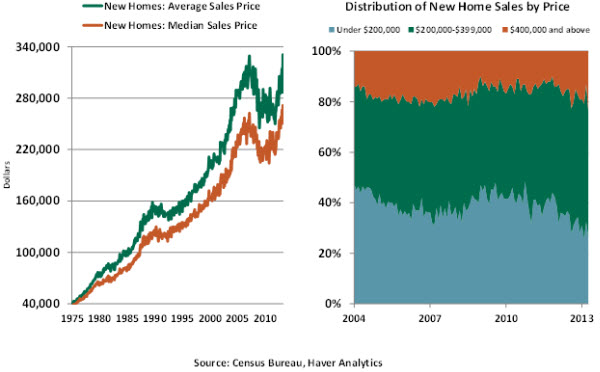

Prices of New Single-Family Homes – More Than Meets the Eye

The median and average price levels of new single-family homes reported by the Census Bureau (CB) posted new historical highs in April. This achievement is noteworthy but must be viewed with some caution because of the way in which the CB compiles its figures.

House price dynamics have turned more favorable. The supply of new homes has dropped, and construction costs have risen. Demand has been boosted by the wealth effect from rising equity prices, improving labor market conditions and low mortgage rates.

The supply-and-demand dynamics for new homes is only a partial explanation of the pickup in prices seen in the CB’s report. The CB’s measure is heavily influenced by the mix of homes sold, which can vary considerably over time. A historical comparison helps explain why the mix of homes sold influences the median and average prices of new single-family homes.

Sales of new homes peaked in July 2005. During this period, the share of new homes priced under $200,000 reached a high mark of 47% of sales, the largest reading excluding the spike related to the first-time home buyer program in 2009-2010.

By contrast, the share of these homes fell to 27% in April 2013. Homes priced upwards of $400,000 accounted for 24% of new home sales in April, the largest share since record-keeping began for this series in 2004. Homes priced at $200,000-$399,000 made up 50% of sales in April, which exceeds the share seen in the housing market boom.

So the caveat here is that the CB’s reading may be exaggerating house price increases in the current environment because of the shifting mix of sales. The market may therefore not be as frothy as it might appear on the surface.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

© Northern Trust