Historically, China has focused on infrastructure and heavy industries at the expense of the service sector as it delivered tremendous economic growth over the last two decades. It may be common wisdom now that in order for China to sustain its economic trajectory over the next decade, it must shift away from investment-led growth and toward more balanced growth, driven by internal demand and consumption. Some key components needed to drive this growth include: continued urbanization, reform of China’s social safety net and, more importantly, a focus on building a service economy that will create and stimulate sustained consumer demand in China for years to come.

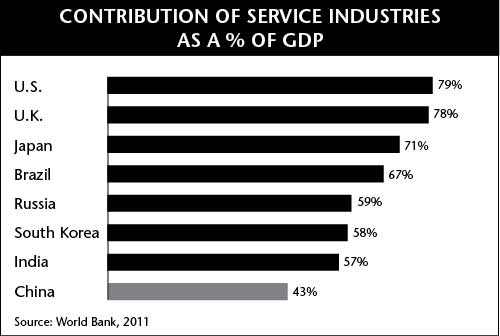

As a result of China’s prior emphasis on manufacturing, the service industry’s contribution to GDP was merely 43% in 2011, far below the U.S., which saw nearly 80%. The contribution was also well below that of countries such as Brazil and India. A country’s “service industry” is broadly defined to include all segments of the economy that provide intangible services such as those in trading, logistics, advertising, hospitality, financial and technological fields. As China’s GDP growth is slowing to about 8%, the government has changed its priorities and its official five-year plan (2011 to 2015) now targets contribution from services at 47% of GDP, which implies that most service sectors may soon experience above-average growth.

Benefits of Services-Driven Growth

Why focus on services? And what are the benefits of services to China’s economy? The service industry creates jobs—many jobs. And jobs need to be the key focus for the Communist Party if it wants to avoid unrest and maintain social stability, especially since it recently underwent a leadership transition. In most developed countries, the service industry usually accounts for more than 60% of total employment due to its generally labor-intensive nature. In China, this ratio is far lower at 35%. As the country’s economic model shifts away from the manual labor-intensive export sector, where many work in shops and assembly lines for clothing and electronics, the government needs to find a new way to generate job growth in order for its millions of migrant workers to maintain social stability. In addition, China produces about 6 million new college graduates each year, and finding quality employment for all these millions of young people is another challenge for its leadership. The service industry seems be a natural progression and a logical solution. Just consider all the manpower needed to provide services for industries that are growing to cater to China’s rising middle class of 300 million (estimated at half of its urban population alone) such as restaurants, language tutoring, health and beauty centers, auto repair shops, banking services and travel agencies. The productivity gains we have seen in manufacturing over the past decade have gradually been moving the labor force upward with higher wages and more demand for services and consequently creating greater opportunities to profit in the services sector. In addition to job creation, service industry growth may lead to higher general income growth and can directly boost consumption. Gains in consumption have notably taken place in other export-driven nations when they shifted to increase their service professions. For example, in South Korea, employment in services grew from 30% in 1961 to 65% in the mid-1990s. In Japan, service employment grew from 38% in the mid-1950s to almost 60% in the late 1980s. In both countries, domestic consumption rose significantly in these years. Typical services jobs also tend to pay more than low-level manufacturing work. In media reports, Beijing workers, such as a manager of a foot massage spa, said they have boosted their salaries by taking urban services jobs. The spa manager said she made roughly US$950 per month, about four times her salary as a factory assembly worker back in central China. In other higher-skilled service sectors, the average pay for those working in information technology and financial services is often much higher, with monthly wages starting from about US$1,500 or more. As more people are employed in higher-paying services work, a virtuous cycle of consumption demand may arise.

Another benefit to growth of the service industry is actually lower energy resource consumption. China’s notorious pollution problems in major cities have worsened from the burden of decades of industrial growth. In contrast, service sectors tend to consume only a fraction of energy resources. In 2007, when services contributed just over 40% to China’s GDP, the sector consumed approximately 10% of its power and 2% of its water—a vast improvement from resource-dependent heavy industrials and manufacturing sectors. A top priority of the Chinese government is to decrease pollution, diversify its fuel mix and reduce its energy dependence—all of which provide even more incentive to spur its service sector to grow.

Development in Select Service Sectors

Even as China’s rebalancing of growth occurs, there are still host of challenges to overcome in order for its service industry to flourish. A lack of scale, a low barrier to entry that breeds competition, higher tax burden and limited funding sources for small businesses are just a few examples of the hurdles. Due to mostly asset-based lending practices in China, most bank loans usually go to large state-owned enterprises versus smaller services companies that may be asset-poor even if they have the cash flow to service the debt. In addition, China’s service industry is known for its notorious competitiveness. As soon as a new business is launched that seems to be doing well, many copycats typically spring up quickly, driving down industry margins. It is also harder to achieve scale in China’s services industries as many of the business owners are smaller operators and may not have the managerial skill sets nor the vision to standardize the process and expand business models to a much bigger scale.

Despite such hurdles, progress is still occurring and both multinational and domestic firms are expanding within China’s many service sectors, and the trend will likely accelerate. On my frequent research trips to China, I have noticed an increasing number of restaurants as well as more diverse cuisine concepts. Many mom-and-pop shops are being replaced by cleaner and more modern outlets with more consistent service quality and chains across many cities. Educational services are also growing, with many signs advertising for English tutoring and test prep centers in urban areas, driven by a cultural emphasis on educational excellence. The trend toward more study abroad and the ultra-competitive domestic college entrance exam process are both spurring development in this sector. Although the education space is very fragmented, several players are slowly gaining scale and strong brand recognition.

In the Internet space, e-commerce services have grown exponentially with a compound annual growth rate of more than 90% in the last five years. Online sales have already reached 6.2% of total retail sales in 2012, leapfrogging the U.S. at 5.2%. Some large Chinese e-commerce players already dominate and several U.S. competitors are also active in this growing sector and teaming up with local partners. On top of driving consumption for online sales and creating many services jobs, another benefit of e-commerce is facilitating more efficiency in the development of logistics services. More than 40% of China’s express delivery volume now comes from e-commerce. The boom in e-commerce has resulted in many players increasingly leasing and building their own warehouses and trucking fleets across the country and installing sophisticated technologies to manage the more efficient use of these resources. Within the auto sector, the business of service components has risen in importance. Although most investors focus on new car sales in China, after-sale services are increasingly being emphasized by many auto dealers as the future driver of dealer profits. In the booming travel sector, wealthier urbanites are spending more on leisure pursuits. We are seeing multiple domestic budget hotel chains emerging and capitalizing on this growth. Online travel portals are also rising in importance by helping consumers navigate and manage their domestic and international travel needs.

China is at an economic crossroads. Which path it takes may greatly affect its long-term growth trajectory. A slower but more sustainable and balanced growth led by services and consumption seems to be the best path for its future prosperity. This shift to boost services will not necessarily be smooth. We are likely to see ups and downs but sharp-eyed investors may find winners that could allow them to capitalize on China’s new services revolution.

Sherry Zhang, CFA

Senior Research Analyst

Matthews Asia

The views and information discussed in this article are as of the date of publication, are subject to change and may not reflect the writers' current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of any securities or any sectors mentioned herein.

The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. Matthews International Capital Management, LLC does not accept any liability for losses either direct or consequential caused by the use of this information.

© Matthews Asia