Fear is a powerful motivator. Whether it’s a saber-toothed tiger or investment risks, it’s hard to stay calm when confronted with a perceived threat. Fear of a 2008 – 2009 downturn repeat, even in spite of strong performance in the US equity market in the first half of the year, has kept many investors sidelined. Grant Bowers, portfolio manager ofFranklin Growth Opportunities Fund, believes fear itself could be the biggest issue holding back many investors right now, noting that in his view, short-term volatility aside, the recent US market rally is based on supportive fundamentals which he thinks should have staying power.

“Clearly there are always short-term issues that will occupy the market, whether it’s China’s growth rate, Europe’s problems, or whether interest rates are going to spike up. You want to be thinking about equities on a long-term basis. I wouldn’t be surprised to see some volatility in the market in the next 3-6 months, but my sense is any volatility could be met with people waiting in the wings to buy—to participate in the market.

“We think the retail investor hasn’t participated meaningfully in this rally. We see bigger-picture trends that look positive, and strong US companies taking market share and being well positioned competitively, generating profitability. In my view, there are plenty of pockets of opportunity for stocks to potentially move higher.”

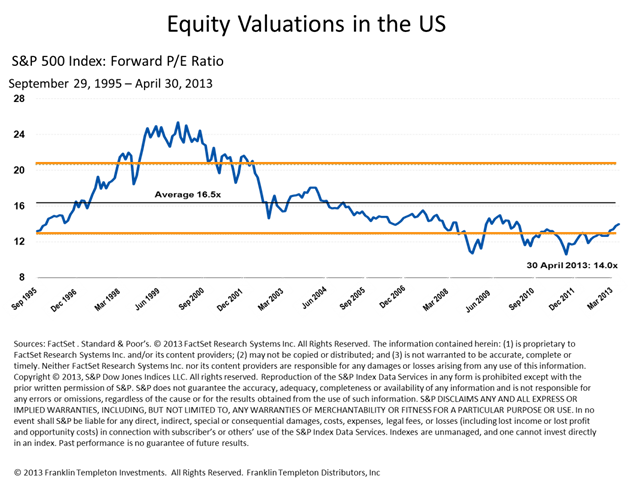

Some investors who may agree they’ve not participated meaningfully in the rally are wondering if valuations are now too high to jump in. Bowers sees a sort of middle ground.

“Markets have rallied quite a lot off the bottom [a few years ago], but valuations haven’t gone up as much as one might expect. Valuations currently sit at right around historical valuation averages on a P/E basis. Not cheap, but not expensive. I think valuations are something you want to be focused on, but I wouldn’t call the US market overvalued; I think it’s fairly valued.

“We think there are still a lot of opportunities where markets/sectors aren’t pricing in growth appropriately. Many US companies exited the financial crisis stronger, leaner and more competitive than they entered it. They expanded globally, have taken market share and are generating cash at unprecedented levels. Cash many companies are retaining on the balance sheets – even with the increases in buybacks and dividends – continues to be impressive.”

Some investors are also wondering if recent gains are a part of a so-called “great rotation” out of fixed income – and if it will last. Bowers doesn’t buy this spin, either.

“We’ve seen investors come back into equities again given recent market returns, and that’s spurred talk of a ‘great rotation:’ a tidal wave of assets into equities and out of fixed income. The idea of a great rotation – I just don’t see it. I think we are seeing a more normalized distribution of new money allocation. Equities are looking attractive relative to other asset classes like fixed income or commodities. I don’t necessarily believe we’ll see a “great rotation” until fixed income investors feel pain, until bond yields move back up substantially. There’s a lot of buying power out there still. There’s a lot of money in cash and people under-allocated to equities.”

An Energy and Housing Renaissance

The idea of a “manufacturing renaissance” taking place in the US has gotten a lot of play recently as manufacturing activity has picked up and increasingly moved back onshore. Bowers terms what’s been happening as an “energy renaissance,” as lower-cost energy is a big factor in this trend.

“The structural changes in available energy, natural gas and oil in the US and the new discoveries of shale gas and resulting liquids have reduced the cost of energy in the US. That’s an embedded structural advantage that lends cost competitiveness for US manufacturers, particularly in commodity-based products. That structural cost advantage can trickle down not just to related companies, but also to the US consumer in the form of job creation and lower-cost goods and services.

“If the US becomes energy independent, it could change the playing field on a geopolitical basis. It can create an entirely new dynamic that could ultimately pay significant dividends for the US economy. These are things that will need to play out over decades. I think it could be a game changer.”

Bowers notes that the resilience of the US consumer is often doubted, but US consumer spending has remained robust, even though it paused briefly during the most recent recession. Like US corporations, US consumers have delivered on their balance sheets, taking advantage of low interest rates. Of key importance to consumers has been confidence in the housing market, which can have a big ripple effect on the economy.

“Housing has been on the mend, and prices are stabilizing. There is pent-up demand for housing purchases in the US. Affordability is high and interest rates are low. My sense is that there is a sort of ‘all clear’ signal home buyers are getting, that they shouldn’t conclude they’ll lose all their money buying a home. We’re seeing buyers come back and even seeing supply constraints in some markets. Housing has a big multiplier effect on the economy; it adds to the labor market, to GDP. A healthy housing market can provide a nice tailwind for the US economy and the US market.”

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes affecting individual companies, particular industries or sectors, or general market conditions. The Franklin Growth Opportunities Fund may be more volatile than a more conservative equity fund and may be best suited for long-term investors. The fund’s investments in smaller- and mid-sized-company stocks involve special risks such as relatively smaller revenues, limited product lines and smaller market share. Smaller- and mid-sized company stocks historically have exhibited greater price volatility than larger-company stocks, particularly over the short term. The fund may focus on particular sectors of the market from time to time, which can carry greater risks of adverse developments in such sectors. These and other risks are described more fully in the fund’sprospectus.

The information provided is not a complete analysis of every material fact regarding any country, region, market, industry, or fund. Comments, opinions, and analyses are those of Franklin Templeton Investments and the quoted person(s) and are for informational purposes only. Because market and economic conditions are subject to change, these comments, opinions and analyses are rendered as of the date of this posting and may change without notice. Opinions are intended to provide insight as to how the quoted manager analyzes securities and the commentary is not intended as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy.

All investments involve risk, including possible loss of principal.

Data from third party sources may have been used in the preparation of this commentary and neither the author nor Franklin Templeton Investments has independently verified, validated or audited such data. We do not guarantee its accuracy. Reliance upon information in this posting is at the sole discretion of the viewer.

Links can take you to third party sites/media, directly or through new browser windows. We urge you to review the privacy, security, terms of use, and other policies of each site you visit. You use any third-party site, software, and materials at your own risk. Franklin Templeton does not control, adopt, endorse or accept responsibility for content, tools, products, or services (including any software, links, advertising, opinions or comments) available on or through third party sites or software.Franklin Templeton Investments and the author accept no liability whatsoever for any loss arising from use of this posting or any information, opinion or estimate herein.

Franklin Templeton Distributors, Inc.

© Franklin Templeton

© Franklin Templeton Investments