Summary

In recent years, the U.S. dollar has tended to lose value when the global economy improves, as investors are more willing to take risks. We believe that pattern has changed and that the U.S. dollar will outperform the Japanese yen, the euro and the British pound over the medium term, even if the global economy continues to improve. In our view, current conditions justify a material deviation in currency exposure compared with certain global fixed income benchmarks, such as the Barclays Global Aggregate Bond Index.

The dollar decouples

When global uncertainty increases, the U.S. dollar has tended to appreciate because investors historically have viewed it as a safe-haven currency. Conversely, when the global picture improves and investors are more willing to take risks, the U.S. dollar has usually lost value.

However, we believe that trend has changed recently, particularly against major currencies such as the Japanese yen, the euro and the British pound. Japan’s recent efforts to reflate its economy have had the effect of driving down the value of the yen versus the dollar. The euro is likely to remain weak as long as Europe remains in recession and vulnerable to perceived increases in systemic risk due to its sovereign debt crisis. The U.S. economy has performed better than other economies in recent years, and the Federal Reserve (Fed) is likely to exit quantitative easing (QE) programs before Japan, the euro zone or the United Kingdom.

As a result, we believe that the U.S. dollar will outperform the euro, yen and pound over the medium term. We believe that the same is likely for the currencies of other countries with more stable fiscal metrics and higher interest rates, including some of the smaller developed economies, such as Norway, Australia and New Zealand, as well as emerging-market economies such as Brazil and Mexico.

Japan’s fiscal adventure

Japan has initiated aggressive fiscal and monetary policies aimed at ending deflation and spurring economic activity. The Bank of Japan has increased its inflation target to 2% from 1% and significantly increased the size of its asset purchases, known as quantitative easing. This has led to a sharp depreciation in the yen, particularly since the beginning of the year.

If everything goes according to plan, Japanese economic growth will increase. Relative growth differentials typically drive inflation expectations and by extension interest rate differentials, and higher interest rates tend to support a stronger currency. However, we believe that the Japanese central bank will commit to a low interest rate policy until it is certain that economic growth can be sustained, and that could take years. We believe that if Japan’s interest rates were to rise in the interim it would be the result of higher implied credit risk, not growth in real gross domestic product (GDP) and inflation, and therefore it likely would present additional headwinds for yen valuation.

If Japan’s bold plan fails, the recent weakness in the yen could be reversed. As the Bank of Japan buys Japanese government bonds in order to push Japanese investors out of safe-haven government debt (hoping investors will shift into equities, private investment or simply spend more), a large portion of Japanese investor funds likely will flow into non-Japanese equity and debt markets. As long as the Bank of Japan keeps rates low and liquidity high, we believe there will be an additional level of support for global risk assets as capital ventures further out on the risk spectrum. However, if the plan doesn’t work or appears likely to be abandoned, that capital can be expected to rush back to Japan, forcing the yen higher against other currencies.

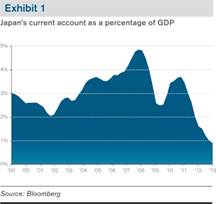

The United States’ dependence on foreign funding is well known, but we believe it may become a factor for Japan, as well. For now, most of Japan’s public sector debt is owned within Japan, traditionally a high-saving country. For years Japan’s current account (the difference between its exports and its imports) has been in surplus, making the country a net creditor to the world. However, in recent years, particularly through 2011 and 2012, Japan’s current account has declined as a percentage of GDP (Exhibit 1). The trend appears to be headed in the direction of a current account deficit, which would make Japan a net debtor to the world. If that occurs, it is unclear which foreigners would choose to finance a country with such challenging fiscal metrics.

Europe’s economy limps along

At present, the United States has the highest projected growth rate among the four regions discussed in this paper. The International Monetary Fund, for example, recently forecast 2013 growth of 1.9% for the United States, -0.3% for the euro zone, 0.7% for the United Kingdom and 1.6% for Japan.

The U.S. economy has shown signs of improvement in recent months. U.S. job growth has been steady, if slow, while the unemployment rate has declined over the past year, to 7.6% in May 2013 from 8.2% in the same month a year earlier. U.S. manufacturing activity has remained mostly in expansionary territory, as reflected in the Institute for Supply Management’s purchasing managers’ index (PMI), which surveys private sector purchasing managers in the manufacturing sector. Despite fluctuations, this U.S. PMI reading has generally remained above the key 50 level that separates expansion from contraction.

Europe has not fared as well. The euro zone remains in recession, and unemployment has risen to 12.2% in April 2013 from 11.2% in April 2012. European manufacturing PMI readings are consistently below 50. The European Central Bank (ECB) recently cut its refinancing rate to a record low 0.5%.

The lingering recession, as well as ongoing bouts of headline risk such as the recent uncertainty in Cyprus and Italy, may force the ECB to buy sovereign bonds in the secondary market. This would bring interest rates down on the bonds in question, while indirectly pressuring the euro lower through expansion of the central bank’s balance sheet. The Bank of England is expected to increase its bond-buying or quantitative easing program, which would have a similar depressive effect on the pound.

Meanwhile, year-over-year U.S. GDP growth has been positive for the past three years. Market participants recently have begun to speculate as to when the improving economy might prompt the Fed to taper off its bond-buying program. If U.S. job growth continues to accelerate, such speculation is likely to lend further support to the U.S. dollar.

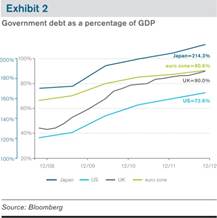

Although the United States cannot be eliminated as a source of potential systemic risk, those risks appear greater in Europe and possibly Japan. As challenging as the fiscal situation is in the United States, it is relatively worse elsewhere. The United States currently has the lowest government-debt-to-GDP ratio of the four regions in question (Exhibit 2). While the U.S. fiscal profile is poor, it looks better than that of other countries, and it is beginning to stabilize. The United States also benefits from holding the status of the world’s reserve currency.

Fundamentals favor dollar

In this environment, we would favor the U.S. dollar even as global growth stabilizes or begins to improve. Countries with lower debt loads and higher growth prospects should have better-performing currencies, and we believe that better relative fiscal and economic fundamentals should be supportive for the U.S. dollar. Of course, the global economy remains vulnerable to shock; two recent examples include recent political uncertainty in Italy and a discouraging bailout precedent in Cyprus. Sustained evidence of a weakening in global economic growth also could lend support to the U.S. dollar, albeit for more traditional reasons.

In short, we believe current conditions justify a material deviation in currency exposure compared with certain global fixed income benchmarks, including the Barclays Global Aggregate Bond Index. Our currency risk management — coupled with our expertise in fundamental, bottom-up credit selection and interest rate differentials — remains consistent with Janus’ core fixed income tenets of preservation of capital and generation of risk-adjusted return. In line with that philosophy, we believe it makes sense to minimize exposure to the yen, euro and British pound, favoring instead the U.S. dollar and certain smaller developed and emerging-market currencies, as long as current macroeconomic and fiscal/monetary policy imbalances persist.

Please consider the charges, risks, expenses and investment objectives carefully before investing. For a prospectus or, if available, a summary prospectus containing this and other information, please call Janus at 877.33JANUS (52687) or download the file from janus.com/info. Read it carefully before you invest or send money.

Past performance is no guarantee of future results.

Investing involves market risk. Investment return and value will fluctuate, and it is possible to lose money by investing. The value of securities fluctuates in response to issuer, political, market and economic developments. In the short term, prices can fluctuate dramatically in response to these developments, which can also affect a single issuer, issuers within an industry or economic sector or geographic region, or the market as a whole.

Bond prices generally move in the opposite direction of interest rates, thus a fund’s share price may decline as the prices of bonds adjust to a rise in interest rates.

Foreign securities have additional risks including exchange rate changes, political and economic upheaval, the relative lack of information, relatively low market liquidity and the potential lack of strict financial and accounting controls and standards. These risks are magnified in emerging markets.

The views expressed are those of the authors as of June 2013. They do not necessarily reflect the views of other Janus portfolio managers or other persons in Janus’ organization. These views are subject to change at any time based on market and other conditions, and Janus disclaims any responsibility to update such views. No forecasts can be guaranteed. These views may not be relied upon as investment advice or as an indication of trading intent on behalf of any Janus fund.

In preparing this document, Janus has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources.

Janus makes no representation as to whether any illustration/example mentioned in this document is now or was ever held in any Janus portfolio. Illustrations are only for the limited purpose of analyzing general market or economic conditions. They are not recommendations to buy or sell a security, or an indication of holdings.

Statements in this piece that reflect projections or expectations of future financial or economic performance of the markets in general are forward-looking statements. Actual results or events may differ materially from those projected, estimated, assumed or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to the other factors noted with such forward-looking statements, include general economic conditions such as inflation, recession and interest rates.

Investment Products offered are: NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Janus Distributors LLC (06/13)

FOR MORE INFORMATION CONTACT JANUS

151 Detroit Street, Denver, CO 80206 I 800.668.0434 I www.janus.com

C-0613-39575 06-30-14 188-15-25732 06-13

© Janus Capital Group