The June employment report was mostly good news. The civilian unemployment rate held steady at 7.6% and payrolls moved up 195,000 during June. The positive tone of the labor market report reinforces the Fed’s current preference to reduce asset purchases later in the year, possibly at the September FOMC meeting.

Details of the June household survey show that the participation rate (63.5%) has registered gains of one-tenth in each of the past two months, a hopeful sign we are tracking closely. The employment-population ratio also moved up by one-tenth to 58.7%, the best reading in seven months.

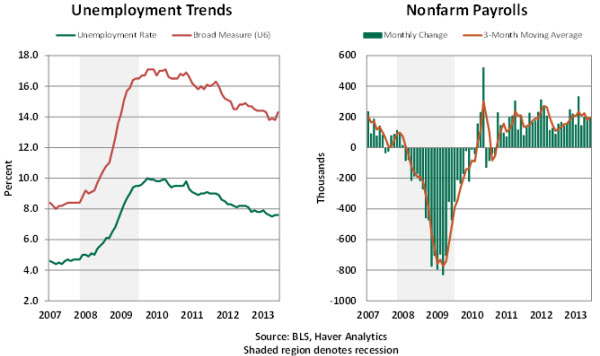

The increase in the broad measure of unemployment (U6) to 14.3% in June from 13.8% in the prior month reflects an increase in discouraged workers and part-time employment for economic reasons. This flaw reduces, slightly, the glow of the June report.

From the details of the establishment survey, revisions added 70,000 more jobs in the April-May period. The three-month moving average of job creation stands at 196,000, a recovery after a brief slip in the March-May months.

Manufacturing employment fell (-6,000), the fourth monthly decline, while construction hiring advanced 13,000. In the service sector, retail (+37,000), leisure and hospitality (+75,000), professional and business services (+33,000) and health care (+20,000) are the components that stand out in the June employment report.

Federal government jobs excluding postal service jobs fell 5,000, putting the second quarter loss at 20,000 jobs compared with a 14,100 reduction of payrolls in the first quarter, which suggests a small impact from sequestration that commenced in March 2013. Payrolls have risen at local governments in the second quarter, but state government hiring fell in each of the three months of the second quarter.

Hourly earnings rose 0.4% in June, the largest increase since November 2008. The strength in earnings and employment bodes positively for income growth in June and should be supportive of consumer spending.

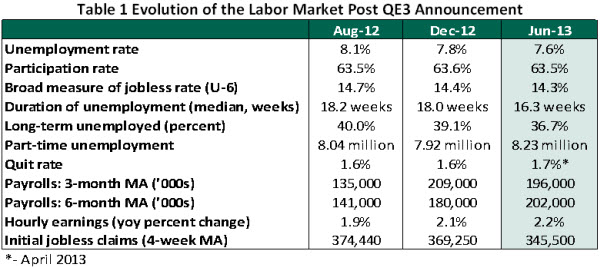

Given the fact that developments in the labor market rule the direction of monetary policy, it is a good time for taking stock of labor market conditions following the Fed’s third round of asset purchases announced in September 2012 (labor market information about August 2012 was on hand at this point) to put today’s numbers in perspective. Details in Table 1 suggest that considerable progress has occurred on several fronts in the labor market following the open-ended third round of quantitative easing (QE3).

The odds of a September tapering have increased but are conditional on labor market conditions continuing to evolve at least as favorably as viewed at the present time. The important caveat is that the Fed's forward guidance has stressed the importance of improvements in the “outlook” of the labor market and inflation to consider tapering, which implies that economic data between now and the September FOMC meeting will play an important role in the timing of tapering of asset purchases.

Note: This is an abbreviated comment due to vacation schedules and short holiday week.

© Northern Trust