Earlier this year, central bank governors in Southeast Asia declared that the region was eager to integrate their economies into what will be known as the Association of Southeast Asian Nations Economic Community (AEC). The 10-member bloc of the Association of Southeast Asian Nations (ASEAN) is striving to make this partnership—which envisions creating a single market and production base and developing closer economic ties both within the region and the broader global economy —a reality by 2015.

In meeting with companies on research trips, I increasingly see more ASEAN companies positioning their long-term investment plans under the framework of AEC, and outlining the ways in which they can expand their home market footprint into neighboring countries. Given the travails of the European Union, one might have thought that the idea of “economic communities” has been discredited. However, ASEAN is plowing forward with its own initiative, taking inspiration from the achievements of the E.U. while trying not to replicate its troublesome features. ASEAN first adopted its blueprint for the AEC during its 13th ASEAN Summit in 2007, aiming to transform Southeast Asia into a more integrated region with liberalized trade for goods and services, investment, skilled labor and a freer flow of capital. As a result, member countries hope to create a more globally competitive economic bloc, and leverage such appealing aspects as its demographic base, which boasts a combined population of approximately 600 million—nearly half the size of China. The average age in Southeast Asia is 30, compared to 38 for China and 44 for Japan, which is encouraging in terms of prospective labor force growth. By purchasing power, ASEAN’s middle class makes up roughly 18% of its overall population and is expected to surpass 25% by 2015.

To be clear, the AEC initiative is more of an economic bloc rather than a monetary union, which we see in the E.U. with its single currency framework. ASEAN central bank governors understand the intricacies and challenges of a monetary union well and acknowledge the issues that Europe faced through the recent financial crisis. Europe's monetary union was not backed with a fiscal union, which would have allowed them to transfer government spending from less affected to more affected parts of the union.

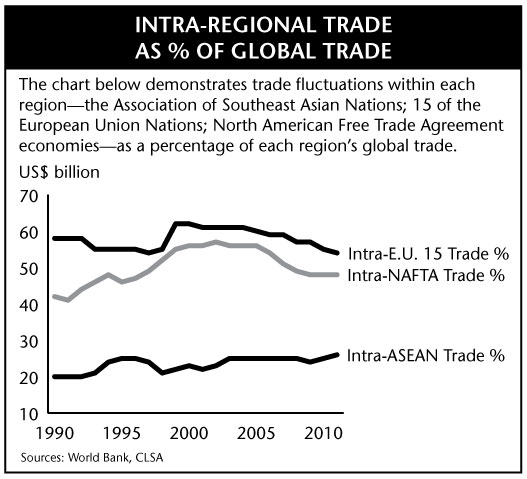

In fact, the desire amongst ASEAN countries to work together has been there for a long time. Since ASEAN was established in 1967, several key trading agreements have been developed including the ASEAN Free Trade Agreement in 1992. However, despite these pacts, member countries have grown less heavily dependent on each other. Over the last four decades or so, GDP per capita of ASEAN founding members have expanded by at least 10 times and in some cases as much as 70 times. However, intra-ASEAN trade has increased only about 15% to 25%. This may seem low compared to 54% for the European Union and 48% for the trilateral trade bloc that makes up the North American Free Trade Agreement. The reasons for ASEAN’s slow integration may be attributed to cultural and political diversity and wide disparity in economic development.

The Integration Process

The initial step to ASEAN integration is the establishment of physical connectivity by member countries. The development of roads, railways and airports to connect member countries is essential for cross-border supply chain integration. Every country has varying resources and competitive advantages. In order for these countries to act as a single production base at a competitive cost, dependable infrastructure needs to be in place.

Secondly, the AEC framework is supported by two other pillars: the ASEAN Political-Security Community and the ASEAN Socio-Cultural Community. These two other communities aim to address issues such as strengthening democratic processes and human rights, enhancing governance and developing human resources—all critical for smooth interregional flow of services and skilled labor. In addition, a special court system has been proposed to adjudicate disputes, help foster the adoption of universal access to primary education in the region and, among other things, promote the more widespread use of the English language.

Another step in the process would be to allow a freer flow of capital that taps access to money beyond the current channels of foreign direct investment. This can bode particularly well for investors over the long run by enlarging ASEAN’s investable universe. Easier flow of capital might be implemented through an integrated banking system or capital market. An integrated capital market may face fewer impediments than banking and such a market may involve equities, bonds and currencies, with the goal of enhancing market access, linkages and liquidity. The first step has been proposed via an ASEAN trading link, an exchange which, in its first phase, would combine Singaporean, Malaysian and Thai exchanges. Later on, it could expand its scope to Indonesia, Vietnam and the Philippines. This sort of capital market initiative is encouraging as it may facilitate efficient reallocation of capital across the economic community and could potentially drive more entrepreneurial activities and deliver faster economic growth. Also, it may increase interregional investment activity among retail investors. With this increased liquidity, more companies may seek to publicly list on exchanges and capital markets could deepen.

Perhaps not surprisingly, along with these loftier goals come bigger challenges. One immediate challenge is enforcement power. The AEC emphasizes consensus building and non-interference in order to maintain stability. ASEAN so far has not pursued the type of tight unified block found among European Union members. Rather, it seems to prefer a looser structure. Without enforcement power, members may find it difficult to advance their objectives given their wide-ranging stages of economic development. For example, in this process, member nations may seek to remove trade tariffs. However, some have recently sought to protect important domestic industries by categorizing them as “strategic” or economically “sensitive.” Malaysia has done this with its auto industry and Indonesia has endeavored to protect its mining industries from such tariff removals.

ASEAN’s financial sector, especially banks, may find even bigger integration challenges. Laws that limit ownership of domestic banks and other regulations that restrict the opening of foreign bank branches in each country are difficult to change. The wide gap in development between the countries makes enforcement more challenging, particularly when member countries are incentivized to consider protectionism first. This is reinforced by the wide dispersion in competitiveness among the ASEAN countries: Singapore is in second position out of a sample of 144 countries, Indonesia lies in 50th place while Cambodia is at 85.*

Despite the hurdles, I believe one of the most important benefits in the AEC initiative is that it presents the opportunity for the economic stakeholders of member countries to rethink their competitiveness.

Recently, one former Bank Indonesia governor publicly expressed the need for banking reform in Indonesia. Indonesia’s Ministry of Industry and Trade selected five focus industries to be intensively developed ahead of the AEC, including cement, textiles, footwear, food and beverages and electronics. Some in the corporate sector have also voiced the need for improving competitiveness in light of the integration plans. One executive from a Thai subsidiary of a global pharmaceutical company has urged domestic scientists to be more involved in research and development to help Thailand’s pharmaceutical industry grow, particularly in preparation for regional integration. He noted that he worried Thai talents may be lured elsewhere in the region (such as Singapore or Malaysia) should Thailand’s own industry not see further industry development. Malaysia’s trade organization came out with a list of niche industries to focus on, such as waste-water treatment and maintenance services for aerospace and oil.

Just how much additional GDP growth can be achieved with a system such as the AEC is arguable. However, in my view, the impact on growth could clearly be meaningful. More importantly, with countries undergoing this integration preparation process, we can expect the development of a more sophisticated and diverse investment universe to become one of the key benefits of the AEC.

*World Economic Forum: The Global Competitiveness Report 2012–2013

In-Bok Song

Senior Research Analyst

Matthews Asia

The views and information discussed in this article are as of the date of publication, are subject to change and may not reflect the writers' current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of any securities or any sectors mentioned herein.

The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. Matthews International Capital Management, LLC does not accept any liability for losses either direct or consequential caused by the use of this information.

© Matthews Asia