Dear Bernanke - You Can't Have Your Cake And Eat It Too

Disclosure:I am longSSO,TBF. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

The U.S. stock market continues its euphoric rise into record territory despite continuing weakness in economic data. Recent comments from Federal Reserve Board Chair, Ben Bernanke, indicating that the Fed does not have a predetermined plan to stop its stimulus plan has investors increasing their allocations to equities.

However, 30 year U.S. Treasury Bond prices continue to fall causing long term interest rates to rise. Some of the decline in bond prices can be attributed to profit taking and/or investors shifting into equities, it should be noted that unlike equity markets, long term bond prices have failed to rally after comments from Ben Bernanke. This may be an indication that bond investors are still worried about the Fed's future plans.

At some point the current disconnect between bond and equity prices will revert to the mean as higher interest rates will have a negative impact on the economy. This will most likely occur in one of two ways:

1) The Fed will increase their purchasing of long term bonds in order to lower long term rates.

2) Equity investors will begin to worry about rising long term rates and shift out of equities.

I believe the Fed is trying to walk a fine line by letting rates rise just enough to cause a minor shift out of equities in order to remove some of the leverage out of equity markets.

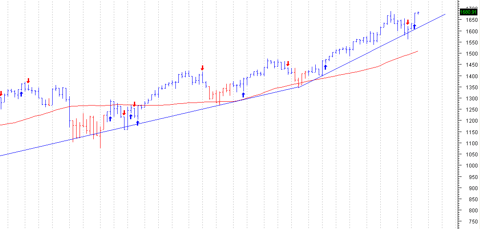

As the S&P 500 Index (SPY) continues its euphoric rise, investors are "buying the dips" in belief that the Fed will continue its current stimulus policy.

SPX Weekly Chart:

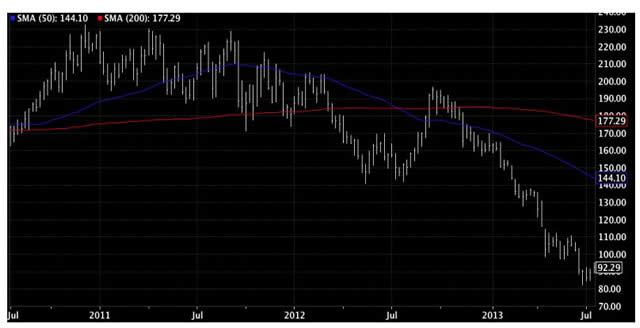

Long term US Treasury bond prices continue to fall and may be headed to levels not seen since 2011.

TLT Weekly:

30 year US Treasury yields are rising, even with an increase in US bond purchases (verses the hinted slowdown in purchases). This may be an indication that the sell off in bonds may be more emotional and less logical.

This may cause prices to drop to 2011 levels where technical traders will begin to shift back into bonds.

Meanwhile, gold (XAU) prices continues to drop. Indicating that investors are not worried about inflation:

Weakness in copper prices year to date is showing that global growth is not expanding which should keep the Fed from ending their stimulus programs.

Continued economic weakness is also supported by comments from shipping companies. FedEx's 45% drop in 4th quarter profits and an outlook for a 2014 GDP of 2.3% demonstrates that global growth is not expanding.

Recent comments from the Fed and the current rise in long term interest rates is a sign that Ben Bernanke may be trying to deflate bubbles that are forming in the economy.

Bernanke's short term objective may be to try to remove some of the leverage in the current market in order to prevent a much larger future stock market drop – while trying to keep the US economy expanding.

Disclaimer

This is provided for information purposes only and should not be used or construed as an indicator of future performance, an offer to sell, a solicitation of an offer to buy, or a recommendation for any security. Riverbend Investment Management, LLC (Riverbend) cannot guarantee the suitability or potential value of any particular investment. Risk Disclosures: The goal of Absolute Return money managers is to achieve positive returns regardless of those earned in financial markets or shown in benchmarks. They seek to do this, using non-traditional investment techniques and asset categories. Of course, there can be no guarantee that any investor will achieve the goal of the managers, that profits will be made, or even that losses will be avoided. Strategy and asset allocation decisions may not always be correct and may adversely affect account performance. The use of leverage may magnify this risk. Leverage and funds employing derivatives carry other risks that may result in losses, including the effects of unexpected market shifts, default and/or the potential illiquidity of certain derivatives. Bonds are affected by changes in interest rates, credit conditions, and inflation. As interest rates rise, prices of bonds fall. Long-term bonds are more sensitive to interest-rate risk than short-term bonds, while lower-rated bonds may offer higher yields in return for more risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. Additional risks are listed in Advisor's Brochure Form ADV, which will be provided by advisor and which prospective investors are encouraged to read. As individual tax rates vary, taxes have not been considered. Various minimum holding periods for each fund may be utilized to comply with trading restrictions. As supplemental information, a listing of all assumed trades and other data used to generate the referenced results is available upon request. Inquiry for more current results is advised. Inherent in any investment is the potential for loss as well as the potential for gain. A list of all recommendations made within the immediately preceding year is available upon written request. The investment return and principal value of an investment will fluctuate; investors' shares, when redeemed, may be worth more or less than their original cost. Actual performance may be materially lower or higher than the performance shown. PAST RESEARCH REPORT RESULTS DO NOT GUARANTEE FUTURE RESULTS.

Copyright 2013 Riverbend Investment Management, LLC. All Rights Reserved.

http://riverbendinvestments.com