Income inequality is rising, but it’s not clear what to do about it

July 26, 2013

- Income inequality is rising, but it’s not clear what to do about it

- Brazil’s struggles come at a delicate time

- Detroit’s road to bankruptcy does not set a path for others to follow

One of the neighbor’s children is interested in economics. He recently stopped by and asked what economic titles I might recommend for his summer reading list. I was flattered, but shocked; I thought young people his age spent their summers at the pool, at the movies, or at an endless series of overnight camps where you could sneak around without parental supervision. At least that’s what I did way back when.

I tried to sell him on some escapist fiction, lest he really open himself to teasing. But insisted. So I shared my copy of The Worldly Philosophers, Robert Heilbroner’s profile of leading economists through history. I read the book as a collegian and found it illuminating.

I saw the young man a few weeks later, and he said he was enjoying the book. He was surprised, he told me, to learn that Karl Marx was an economist. He was, indeed, and spent hours in the reading room of the British Library in London working toward the conclusion that the extremes of capitalism would ultimately be its undoing. Marx was right in one regard: free markets can create extreme outcomes. But these extremes have not created the widespread regime changes that Marx may have anticipated or hoped for.

Around the world today, economic inequality is rising both within and among countries. And this has raised alarm among policy-makers. But before seeking to address it, we must answer some to key questions: What is the root cause of divergent fortunes? Does inequality affect economic performance? Would redress represent a net positive? Some reflections on these topics follow.

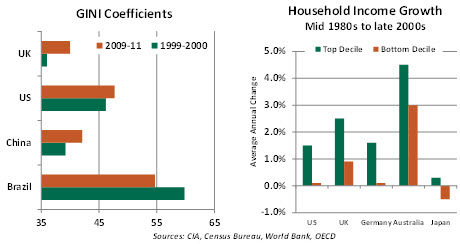

The most common way of measuring income inequality is with a “Gini coefficient.” It is based on the shape of a country’s income distribution; if everyone earns the same income, the Gini coefficient for that group is 0; if all income goes to one person, the Gini coefficient is 1.

Gini coefficients look at trends over the entire income spectrum. Cross-sectional perspectives, which look at the relative fortunes of those at the top and bottom of the ladder, are also very instructive. By either measure, income inequality has grown almost uniformly across nations, and those at the extremes have seen their lots diverge substantially.

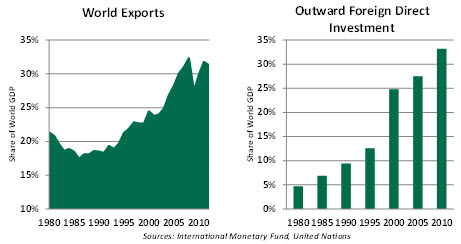

There are three leading explanations for these developments. The first is advancing “globalization,” which might be defined as broadened trade channels that facilitate distributed production and access to finished products from all over the world. Clearly, the volume of international trade and cross-border investment mushroomed in the last generation.

This process tended to reward skilled workers at the expense of those carrying more basic backgrounds. It is worth noting that the metaphor of white collar versus blue collar is too narrow; many professional job categories also were importantly reshaped by global competition (data processing, for instance).

The second is technology. Factory robotics curtail the need for assembly-line workers; enhanced connectivity has broadened access to competitive alternatives; and the technology industry itself has rewarded those with the talent to design new devices and the software that makes them useful.

The third is changing policy. Alterations to competitive restrictions, labor laws and tax codes are all thought to have played a role in accelerating inequality in many countries.

It’s certainly true that these elements are somewhat intertwined. Globalization does not occur without the establishment of free trade agreements or zones, which are the province of policy. Globalization would not be possible without the considerable application of technology. So it is very difficult to determine which of these has been most influential.

At many levels, globalization and technology have aided economic growth. And while threatening to some classes of workers, the increased access to goods at more modest prices has helped living standards. But recent studies seem to suggest that rising inequality may limit the strength and duration of economic expansions. Social stability also may be threatened by excessive inequality. Some have expressed surprise that increasing income gaps and high levels of unemployment haven’t yet kindled broad unrest in certain parts of the world.

Addressing inequality will be challenging. Tax changes to divide the pie more equitably could diminish the incentives that brought the pie to its current size. Curbing global and technological change will be exceedingly difficult, given the momentum these forces have gathered.

But there is one avenue of redress. Studies continually point to education as cause and potential remedy of income inequality. As we highlighted in our recent View from Here commentary, cultures must continually invest in education to preserve competitiveness and provide opportunity. Those cultures that fail to win the race between schooling and technology have worker skill levels that put them on the wrong side of globalization.

The concept of equality is central to the visions of many nations. This typically refers to equality of opportunity, not necessarily outcome; but there is mounting evidence that inequality of outcome creates inequality of opportunity. Reversing this negative cycle will be essential to keeping Marx in his place.

Facing Boo-Birds in Brazil

Attempting to open the Confederation’s Cup football tournament last month in Brasilia, President Dilma Rousseff was shocked to be shouted down by some 70,000 fans of the Seleção Brasileira. Indeed, last month’s large-scale protests caught Brazil’s political class off guard. But to those acquainted with Latin America’s largest economy, the rising discontent is no surprise.

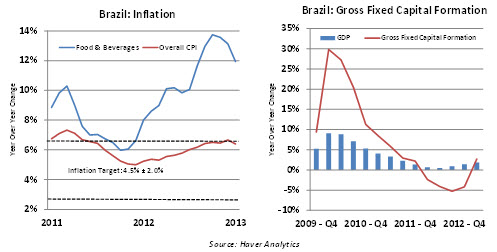

Inflation has reared its head this year, skipping around the 6.5% upper bound of the Banco Central do Brasil’s target range and bringing back memories of 90’s hyperinflation. Particularly devastating are surging food prices, up 12% since last July due to a series of price shocks in the past year. Pocketbooks squeezed and stomachs growling, Brazilians took to the streets.

Inflation has reared its head this year, skipping around the 6.5% upper bound of the Banco Central do Brasil’s target range and bringing back memories of 90’s hyperinflation. Particularly devastating are surging food prices, up 12% since last July due to a series of price shocks in the past year. Pocketbooks squeezed and stomachs growling, Brazilians took to the streets.

Yet the discontent reveals deeper flaws in Brazil’s economic model. After a decade of impressive expansion averaging 3.7% gross domestic product (GDP) growth from 2000-2010 (despite contracting in 2009), the economy recorded near-stagnant 0.9% growth in 2012 and faces an uphill struggle to reach 2.2% growth this year.

Since the first signs of slowing in 2010, policymakers set aside more orthodox economic policies in favor of an interventionist approach, with monetary easing, loan programs, and ad-hoc tax breaks. These steps were aimed at propping up private consumption, the backbone of the Brazilian economy (66% of 2012 GDP). In this regard, Brazil looks very different from other emerging economies, which rely much less on domestic demand and a lot more on exports.

As recently as March, Ms. Rousseff was calling on the central bank to prioritize growth over inflation. Yet these interventions have backfired. The inconsistent policy mix saw investor confidence plummet, especially in the face of rising inflation. Annual inflows of foreign direct investment bottomed out in the first quarter of 2013, their lowest point since 2010. Private consumption grew 3% last year while gross fixed capital formation contracted by 4%.

By April, Ms. Rousseff vowed to fight inflation with gusto and the central bank began to hike the SELIC rate, but policymakers have left unaddressed the structural issues that threaten Brazil’s competitiveness: infrastructure bottlenecks, labor market rigidities, overly-complex tax codes, and elevated levels of corruption.

If rising prices brought the people into the streets, ire at the political class will likely keep them there over the next year. Brazil plays host to the 2014 World Cup next June and prepares for general elections the following October. Ms. Rousseff is feeling the pressure as her approval rating plunged from 74% in June to 49% in July; recent polling shows she would still win the election if held today but face a run-off against Marina Silva, a former Green Party candidate. Interestingly, Ms. Rousseff’s mentor and former President Luiz Inácio Lula da Silva would fare much better than she would if he were to run.

Investment has picked up this year and inflation began to decline in July, but in an election year with a struggling economy, structural reforms and the fiscal restraint needed to truly tackle inflation are not likely. Ms. Rousseff will hope that monetary tightening is enough to beat inflation and boost confidence. If not, she may face the boo-birds again next year.

Motoring into Bankruptcy

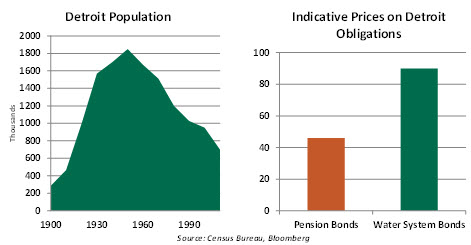

Detroit’s decision to file for bankruptcy protection was certainly not unexpected. In its wake, some have suggested that Detroit could be the tip of a public finance iceberg that will sink other cities and counties, and with it, the municipal bond market. But it is very, very difficult to leap to that conclusion.

First, Detroit’s circumstances were extreme. The city’s population is less than half of what it was at its peak. The area’s economy was far too deeply concentrated in a single industry that proved vulnerable to global competition. Property tax receipts, the lifeblood of city revenue, have dropped alarmingly as homes fall into foreclosure and values in some neighborhood dwindle to almost nothing. (The estimated median house price in the city of Detroit is only around $17,000, a shocking figure.) While other locales certainly have their share of political dysfunction, Detroit’s was among the very worst.

Secondly, the municipal bond market is extraordinarily heterogeneous; issues and issuers vary considerably. Even within Detroit’s debt mix, there are bonds whose values are holding up very well in the wake of the bankruptcy and those which are virtually worthless. And the overall municipal market did not experience a significant correction in the wake of Detroit’s filing. It’s always been critical to do careful homework when investing in the municipal sector.

Finally, the bankruptcy rules for public bodies differ substantially from those that apply to individuals or corporations. Filings must have the approval of the state in question; satisfying this requirement may be easier in some places than others. Lawsuits are expected to have a substantial influence on the timing and outcome of Detroit’s resolution, and court decisions could certainly vary from state to state.

Certainly, Detroit’s plight will be closely watched. The city is not the only place weighed down by bond payments and pension obligations. But it is unlikely that Detroit will lead a convoy of other cities into bankruptcy.

© Northern Trust