The global productivity “bust” is largely cyclical

- The global productivity “bust” is largely cyclical

- The Bank of England tries forward guidance

- Will low labor force participation keep the Fed from tapering?

How productive are you? After a strong cup of coffee, I can simultaneously run a forecast, write 6,000 words and mediate the latest dispute between my wife and my children. When the caffeine wears off, I can barely tie my own shoelaces.

Productivity is a terribly important concept in the realm of economics. It has strong links to hiring, inflation and national income. With the world mired in a period of very modest growth, enhancing productivity may hold the key to achieving escape velocity from this low orbit.

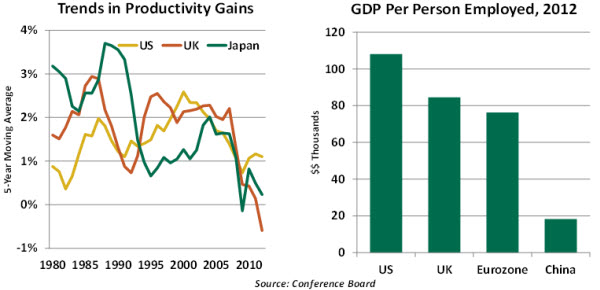

Simply stated, productivity is how much output can be produced by a given input. Labor productivity (how much product a person can make in a given time) is the most common expression of this concept. After averaging close to 2% annually in the decade leading up to the recent recession, productivity in major economies has dwindled significantly since then.

Productivity is critical at many levels. Workers who are more productive typically have higher living standards; societies that are more productive enjoy a competitive edge. Some have the perception that enhancements in productivity (like mechanization of work) threaten workers, but in the long run enhancements make workers more valuable.

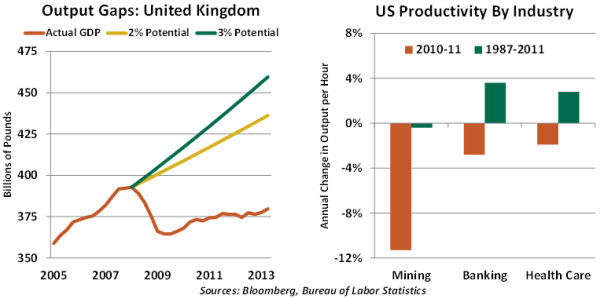

The ability to make more with less also reduces stress on resources and therefore limits inflation. Economists utilize the concept of “potential growth” to express how quickly gross domestic product (GDP) can expand in the long run without placing pressure on prices. Potential growth is typically calculated by adding the growth of the labor force and productivity growth; the difference between this level and actual growth creates an “output gap.”

For central banks, the proper derivation of potential growth is critical to setting monetary policy. If an output gap is especially large, stimulus is called for. With short-term interest rates near zero in many places, this corresponds to additional quantitative ease. As output gaps narrow, accommodation must be withdrawn.

It was only 10 years ago that Alan Greenspan took a risk by betting on a “new paradigm” in which technology and globalization were combining to raise productivity and allow economies to grow more rapidly without stressing inflation. At the time, it seemed like real growth could proceed at 3% annually or even better without placing undue pressure on the price level.

Today, expectations are more modest. The Federal Reserve’s and the Bank of England’s long-term projections are presently centered on 2.3% growth. In each market, there remain substantial differences between the actual level of GDP and the level that would have been achieved had the two economies followed their long-term growth path. The size of this shortfall is very sensitive to assumptions about long-term productivity.

There are a variety of theories that attempt to explain the apparent productivity “bust.” Many contend that this is exclusively a cyclical problem; global demand has been very soft, so productive resources are not being used to the fullest. The thinking goes that as conditions improve, output can be expanded for a time without a commensurate increase in inputs. This would be the case for heavy industry, which has seen productivity fall drastically of late.

Others wonder whether recent readings are simply a measurement problem. Productivity in two other American industries – financial services and health care – figured strongly in the new paradigm but has dropped off sharply. Measuring output in service sectors is not the most precise of exercises; therefore, some observers are skeptical about recent readings.

The worry, though, is that something more permanent is at play. Investments in capital help productivity; levels of this activity have only recently returned to their pre-crisis peaks. Financial stress, especially in Europe, may be limiting funding for invention and the means to capitalize on it. Once a great source of productivity gains, infrastructure of all kinds is aging in many countries, and governments lack the funds to modernize it. Aging populations and the quality of education at some levels may also be hindrances.

In a provocative paper entitled “Is U.S. Economic Growth Over?”, Robert Gordon, an economist at Northwestern University, suggested that the benefits of the recent technology revolution will peter out quickly. With no new innovations in sight, this would leave us with very modest annual growth in productivity and GDP.

Others are more sanguine. It certainly appears that the penetration of advanced technology is far from over and is in its initial stages in some places. As prospects for growth recover, rewards to potential innovators will rise and risks may moderate. And one never knows when the next major wave of change may arrive. Who among us thought 30 years ago that a single device would do as many things as a smart phone does today?

Key to restoring productivity growth will be supportive policy. Austerity measures that fail to distinguish costs from investments (in education and infrastructure, for example) will prove very counterproductive in the long run. As economic conditions improve the standing of public budgets, one might hope for increased emphasis on the renewal of human and physical capital.

To sustain my personal productivity, I’ve decided to install a coffeemaker in my office with cycling tied to market volatility and the volume of emails I receive from home. With the economy struggling and teenagers at home, I’ve stocked the cabinet with French Roast.

The Bank of England Takes a Page from the Fed’s Playbook

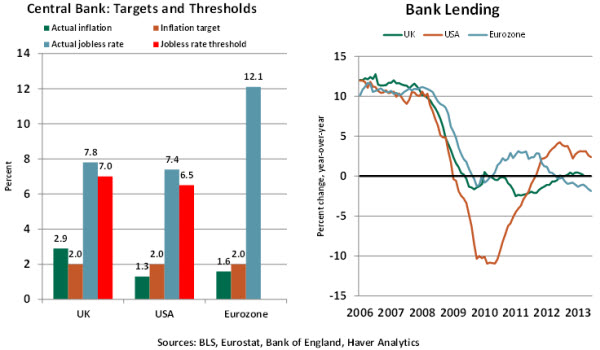

Governor Mark Carney, new at the Bank of England (BoE), took a strong step this week by working with his Monetary Policy Committee (MPC) to implement “forward guidance” designed to spur U.K. economic activity. In the British form, forward guidance consists of maintaining the current low policy rate until the unemployment rate declines to 7.0% (7.8% is the latest number) and not reducing the £375 billion of assets the BoE bought between 2009 and 2012. The BoE stands ready to buy more assets if the jobless rate continues to hold above 7.0%.

While not wholly unexpected, the move to target unemployment might seem out of line with the BoE’s single mandate to control inflation. Price stability is the primary obligation of the BoE, unlike the Federal Reserve’s dual mandate of price stability and full employment. Linking monetary policy actions to the status of the labor market raises the question of whether the BoE has tacitly embraced the Fed’s dual mandate. To some, this has been the case for more than three years, given that inflation has exceeded its 2% target.

To address these concerns, the BoE attached three “knockout” conditions to its forward guidance. First, the BoE’s monetary policy stance is subject to change if the MPC deems inflation will exceed the 2% target by 50 basis points or more 18 to 24 months ahead. While the latest U.K. inflation reading shows a year-over-year increase of 2.9%, non-recurring increases in taxes account for a good portion of this. The MPC views risks around 2% inflation as broadly balanced for now, but markets will be extra sensitive to the MPC’s inflation forecast and unemployment numbers in the months ahead.

Second, the MPC would tighten monetary policy if medium-term inflation expectations were unmoored. For now, this does not seem to be a worry.

Third, the MPC would raise the policy rate if the Financial Policy Committee (FPC) warned that easy monetary policy is a “significant threat” to financial stability. The Fed and European Central Bank (ECB) have different organizational structures tracking sources of financial risk and instability. The findings of the Fed’s Office of Financial Stability Policy and Research, an advisory body, and the ECB’s biannual Financial Stability Overview do not trigger monetary policy actions. Effectively, the BoE has placed financial stability on a nearly equal footing with inflation and unemployment by including the FPC within the forward guidance framework. The MPC and Financial Policy Committee nexus in constructive, but it should be noted that disagreements may surface down the road.

Our July 12 comments noted that forward guidance per se is not sufficient to ensure growth. For forward guidance to succeed, banks must pass on low rates to businesses and households, which in turn invest and spend. Bank lending in the United States has recovered, and bank balance sheets are healthy. By contrast, European banks are capital-constrained, and lending is significantly weak in the U.K. and continues to contract in the eurozone. Credit-starved conditions translate into weak economic growth. So, the risk of a weak impact of forward guidance is a valid consideration.

Further, many think that the BoE must increase its quantitative ease at some point to address Britain’s large output gaps. Nonetheless, forward guidance represents a significant first step in the Carney regime, likely the first of many.

Will the U.S. Participation Rate Stabilize?

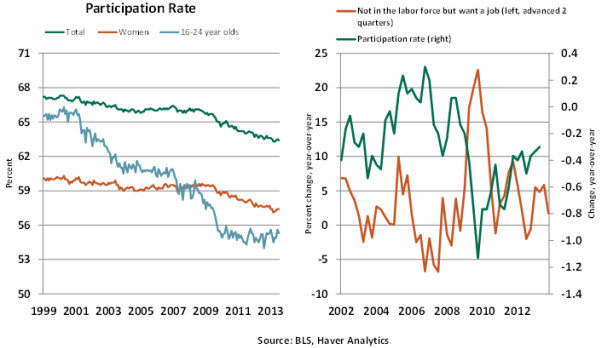

Assessing whether the decline in the jobless rate to 7.4% in July from 8.2% a year ago is truly a sign of improving U.S. labor market conditions is not straight-forward. The labor force participation rate has declined to 63.4% from 63.7% in this period. A pickup in hiring is usually associated with an increase, not a decline, in the participation rate.

Establishing the imminent trend of the participation rate is critical because the Fed has identified employment thresholds to guide its monetary policy actions. The Fed plans to have completed tapering of asset purchases at around a 7.0% jobless rate and would consider raising the federal funds rate when the unemployment rate hits 6.5%.

If the participation rate declines due to demographic factors and is not a result of an increase in “workers not in the labor force but who want a job,” a lower unemployment rate would denote improving labor market conditions. On the other hand, if an increase in this pool of workers has accounted for lower participation and unemployment rates, the Fed’s current unemployment thresholds must be lowered accordingly.

So what do the numbers indicate? The total participation rate reflects lower participation for most age groups in the past year. The participation rate of women and 16- to 24-year-olds appears to be stabilizing in the last six months. These data suggest that demographic factors are exerting a smaller adverse impact on the participation rate.

From a cyclical perspective, a large number of workers who left the labor force during and after the Great Recession wanted a job. The good news is that the tally of these workers shows a decelerating trend of late, which may presage an increase in the participation rate.

It is important for observers not to overly fixate on the specific unemployment thresholds that the Fed has cited as potential turning points for policy. They are guideposts, not triggers, and officials have consistently said they will look at a range of indicators before concluding that employment conditions are truly improving. The labor force participation rate is certainly one of these, and it deserves close attention.

© Northern Trust