India: Broken promise or temporary hiccup?

August 23, 2013

- India: Broken promise or temporary hiccup?

- Bond markets appear unmoved by central bank guidance

- Rising mortgage rates are taking some of the steam out of housing

Events of the past two months lead one to wonder whether the bloom is significantly off India’s economic rose. Like other members of the BRIC (Brazil, Russia, India and China) club, investors are asking tough questions about the country’s future. Yet there are factors that set India apart from other emerging markets that may help it fare somewhat better in the decades ahead.

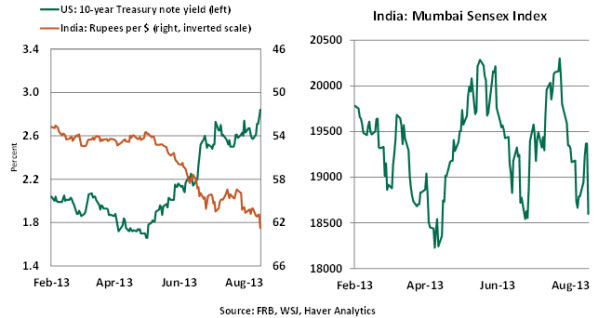

Recent events have certainly been very challenging. The rupee plunged nearly 17% since May, the Sensex equity index lost 10% in the past month, and capital outflows are mounting. The economy grew only 4.8% from a year ago in March, a far cry from the 8.0% average during the last decade.

India and other emerging economies have attracted funds in search of yield as major central banks engaged in ultra-easy monetary policy. But the possibility that the financial accommodation will taper has sent capital in the other direction, hindering India’s currency and asset prices.

Problematic fiscal and current account deficits and recent low growth rendered India vulnerable. Policy-makers, aware of market sensitivities, tried to enforce fiscal discipline. Cuts in oil subsidies accounted for a part of the reduction in the budget deficit; ironically, the recent weakness of the currency presents a short-term risk as every rupee decline vis-à-vis the dollar increases the cost of maintaining the subsidy that remains.

Unlike other emerging markets, India has run a trade deficit of more than 3% of gross domestic product (GDP) since mid-2011, and it’s a source of pressure on the exchange rate. Exports from a year ago dropped for two straight quarters, after double-digit gains in 2010 and 2011. Exports are critical for growth in India, as they accounted for more than 20% of GDP in the last seven years.

It is certainly hoped that a turnaround in global growth would reverse the weakness in exports. India’s export strength derives from services, a situation that differs markedly from other emerging markets and supports expectations of a revival. The country does not face a severe shortage of foreign exchange reserves of the sort that prevailed in 1991. But markets are jittery, given the sub-par growth performance.

Inflation is a problem in India. Increases in consumer prices moderated after hovering above 10% in the closing months of 2012 and early part of this year. This puts the central bank in a bit of a bind; tightening would fight inflation and support the rupee but would harm economic activity. India’s central bank is under political pressure to take suitable action to promote growth, but recent policy action focused on currency stabilization, which reinforces its independence relative to most other emerging markets. The policy easing cycle that began in April 2012 is not over, but further cuts will be delayed until the currency stabilizes.

Markets will focus on long-term issues after the dust from the tapering tremor settles. As globalization unfolded during the last two decades, India’s labor cost advantage and an educated English-speaking labor force helped bring about a period of high growth. Although some of the low-hanging fruits have been picked, the advantage of low labor costs should prevail for a few more years.

Critical inputs, such as infrastructure and an educated work force, are necessary to restart the torrid growth of past decades. Reliable power supply and adequate fuel are missing in India. The corrupt bureaucracy of India is a long-standing issue that needs addressing. Byzantine rules around land acquisition make it hard for businesses to build factories. The reform package unveiled last year touches on some aspects of these impediments to economic growth, with the few reforms it includes yet to take full effect.

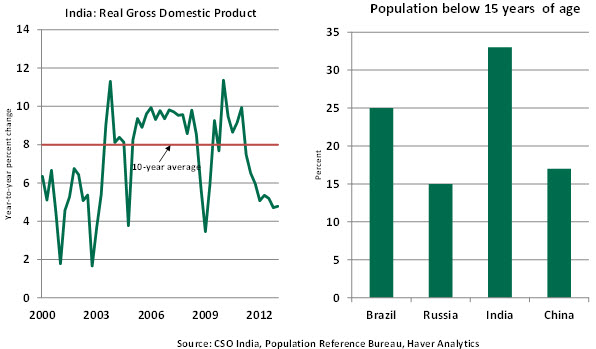

India is in a sweet spot in terms of demography, as it is a young nation with 33% percent of its population younger than age 15. Brazil is close to India’s status, with 25% of its population in this age group, while China and Russia have 17% and 15%, respectively. For the demographic dividend to pay off, the quality of education must improve to enable millions to become part of a productive labor force. The economic spillovers of an educated workforce will go a long way toward reducing the stark inequality that has persisted for generations.

Will India and the rest of world navigate successfully through the current turmoil? Cautious optimism is not out of line for India, because foreign exchange reserves are adequate and a flexible exchange-rate regime to mitigate the impact of portfolio capital outflows is in place. Short-term market volatility and a growth setback for India are certain. The lower value of the rupee reduces exports of India’s trading partners and earnings of multinationals. Overall, short-term pain cannot be ruled out.

The door to long-term economic growth in not closed, for now. If India is to become more investor-friendly, political leaders after the May 2014 elections will be forced to deregulate large parts of the economy, cap the fiscal deficit and improve revenue collection.

In sum, today’s unfavorable market sentiment should fade, and India’s virtues of democracy and demography should stand out compared with its peers. Not all emerging markets are the same; one hopes investors will regain their appreciation of this nuance ¬– and of India.

Failing to Follow Guidance

The Federal Reserve’s annual monetary policy conference at Jackson Hole, Wyoming, convenes this weekend. The agenda is designed to examine the effectiveness of unconventional monetary policy, comparing the use of quantitative easing (QE) and forward guidance. The papers presented at the conclave typically study subjects over long time periods. But a very recent sample suggests that the use of forward guidance by at least two central banks has been somewhat ineffective.

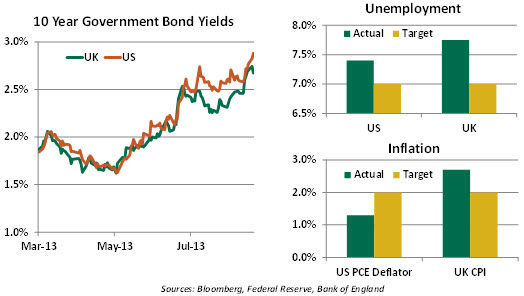

Earlier this month, the Bank of England (BoE) announced its intention to keep its benchmark rate at 0.5% until U.K. unemployment drops below 7%. As the BoE’s internal forecasts don’t anticipate reaching this objective until 2016, this statement was an attempt to anchor longer-term interest rates or even induce them to fall somewhat.

Throughout this summer, the Federal Reserve has stressed that any tapering of its quantitative easing is expected to be very gradual. This statement was also intended to keep longer-term interest rates anchored.

Unfortunately, investors apparently are not heeding these messages. Long-term interest rates have marched right through forward guidance to much higher levels over the past two weeks.

The bond price retreat has occurred in spite of some fitful times in emerging markets that would normally prompt a flight to quality. Inflation expectations in both the United Kingdom and the United States have been declining, so that does not account for the fixed income sell-off.

A more plausible explanation is that there is some doubt over the commitment of the two central banks to the promises that they have provided. The minutes of the BoE’s Monetary Policy Committee (MPC) revealed less-than-unanimous support for the forward guidance announced by Governor Mark Carney. Some MPC members preferred a different formulation, while others instead favored additional quantitative easing.

In the United States, minutes of the July Federal Open Market Committee (FOMC) meeting reflected an active debate over the possible tapering of QE. Some members expressed reservations about the Fed’s most recent form of forward guidance, which suggested that asset purchases could end by mid-2014 if the unemployment rate falls to 7%. Conditions may require altering that threshold, a move that could compromise credibility. The minutes also reflected a range of views over how healthy the labor market is at this stage.

Additional uncertainty over American monetary policy likely stems from the potential lineup changes at the Fed, which we discussed in our August 16 weekly. Speculation over Chairman Ben Bernanke’s replacement continues to dominate the business pages, despite reports that President Barack Obama will wait until Fall to forward a nomination. Questions about whether today’s forward guidance will remain in place next year are on the minds of portfolio managers, who are demanding higher term premiums.

In general, we have been very supportive of the incremental openings in central bank communication that have progressed over the past 30 years. They offer markets more insight, in a more timely fashion.

But when there are significant internal divisions, the mixed messages that emerge from central bank minutes and speeches can diminish the effectiveness of forward guidance. In this case, perhaps it’s better to air dirty laundry in private.

Opportunity Lost?

Housing is among the brightest lights in the American economic firmament. Starting from a very low, recession-beaten base, home sales, construction and values all recovered fairly nicely. In some areas of the country, conditions are reminiscent of the halcyon days of 2005.

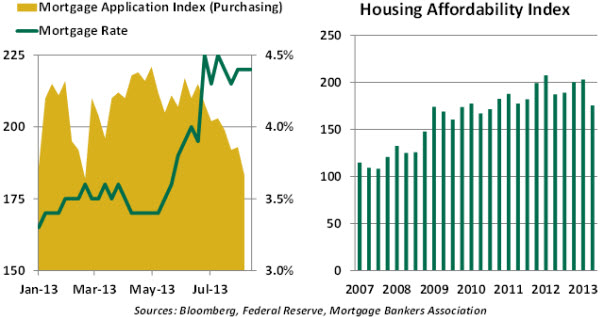

But the momentum may be difficult to sustain. With long-term bond yields rising, mortgage rates followed. Higher borrowing costs have had a pronounced effect on mortgage applications. When combined with the recent escalation of house prices, housing “affordability” took an important step back last quarter after improving consistently since the market bottomed.

Reports suggest that investors have been very active in acquiring blocks of homes, especially in areas where distress lowered values and turned homeowners into renters. These are largely cash transactions, so higher mortgage rates should not curb the enthusiasm as long as the rental economics continue to make sense.

For first-time homebuyers, and for existing homebuyers whose equity has risen to the point where they can contemplate moving, the rise in mortgage rates will be meaningful. On a $250,000 property, buyers are looking at monthly payments that are more than $100 per month higher than they were last spring.

Some suggest that the housing recovery needs to be better balanced, with owner-occupiers accounting for a larger share of purchases. Excessive investor demand might be destabilizing when the attraction of another asset class prompts a reallocation of capital.

Two policy steps will aim to aid this transition. First, the Fed is likely to reduce its purchases of Treasury securities more significantly than its purchases of mortgage-backed bonds if and when the tapering of QE commences. And debate over the future of Freddie Mac and Fannie Mae seems to have picked up, with broad access to credit among the objectives.

So you may not have completely missed the boat if you waited to buy property… but if you need a mortgage, the ship may be about to sail.

© Northern Trust