Hong Kong: A Gateway to Chinese Companies

While many investors and businesses in Hong Kong are struggling with China’s slowed-growth policy, increased rates on commercial rentals, and government intervention to cool the residential property market, we at Royce are looking for opportunities in Hong Kong-listed companies—our primary entrance to gain access to Chinese companies—whose valuations are reflective of the macro challenges facing their economy.

Readers also enjoyed:

Hong Kong is among the most dynamic cities on the planet, and locals have a remarkable ability for reinvention. The port city on the South China Sea has moved from being a manufacturing center in the 1960s and ‘70s to a service economy currently rivaling that of New York or London. Yet on my most recent visit, I found the mood on the ground to be rather somber. The Business Confidence Index in Hong Kong in the second quarter of 2013 was at 9% (the difference between the percent of establishments choosing “better” and those choosing “worse”), which was well below the average of 11.53% between 2006 to 2013 and the record of 32% for the third quarter of 2006.1

One sobering change has been government intervention to cool the property market: More than 30 policies intended to curb apartment prices have been implemented since October 2009. These include a 15% tax on foreign buyers, a double stamp duty, which doubles the stamp duty on residential and non-residential purchases of more than $2 million H.K. ($258,000 U.S.), and capital gains taxes of 15% on property resold within six months of purchase. Such measures have irked some members of the business community as well as investors who think the policies are too restrictive and believe the market will naturally cool when interest rates rise.

June 22, 2013 article from South China Morning Post

To understand the motivation behind the government’s actions, consider that after the global financial crisis of 2008 Hong Kong’s property market rebounded strongly in 2009. By December 2009, residential property prices had risen 30% as the city drew a record $73 billion in capital inflows between October 2008 and November 13, 2009.2 In October 2009, a developer sold a duplex for a world record of $88,000 H.K. ($11,300 U.S.) per square foot for a total price of $439 million H.K. ($57 million U.S.).3 Donald Tseung, the Chief Executive of Hong Kong, stated in December 2009, “We are very concerned about the risk of an asset bubble.” Since Hong Kong’s currency is pegged to the U.S. dollar, the Hong Kong Monetary Authority was forced to adopt the Federal Reserve’s monetary policy of low interest rates. The government did not have the option to increase interest rates, which only spurred it to find other ways to intervene in the real estate market.

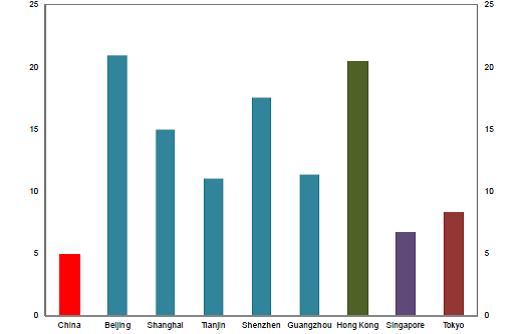

The first measure was to restrict the amount that banks could lend to buyers of luxury homes valued at $20 million H.K. ($2.6 million U.S.) at 60%, down from 70% in October 2009.4 Still, property prices in Hong Kong continued to increase. In December 2010, the IMF put out a working paper warning of the potential for a bubble should further measures not be implemented.5 Mass market property price-to-income in Hong Kong was expensive relative to household income when compared to other cities in the region. In 2011, there were protests against property developers and the government as property prices increased by 18% through August 2011;6 since the beginning of 2009 prices have increased by 107%.7 The government responded with further policy actions.

House price-to-household disposable income across markets (levels)8

It appears that the government’s cooling strategies may finally be working. The level of property transactions—usually a precursor for prices—was down 49% in May, the third straight month of declines.9 The number of transactions has dropped by nearly 40% since the start of 2013.10 Prices in Hong Kong have fallen by 2.3% since February when the government implemented the doubling of stamp duties on all property transactions higher than $2 million H.K. ($258,000 U.S.).11

The significant slowdown in transactions has dramatically affected the city’s property brokerage industry. Real estate agents fearing for their livelihood have taken to the streets to protest the cooling measures put in place by the government. Given the buoyancy of the property market since October 2008, the number of real estate agency offices had ballooned to 6,000 (with 300 opening in the last year alone).12 As the market cools, many of these opportunistic entrants will exit the real estate brokerage business and probably aim to enter the next “hot” market.

One of our investments in Hong Kong is a stalwart of the real estate brokerage industry and has been through far tougher times than the current environment. The company and its primary competitor are mainstays of the industry and together control over 60% of the market. Through times of weakness, such as the Asian financial crisis of 1998 and the SARS epidemic of 2003, the company was able to further consolidate the market by buying out weaker competitors. The management team has a very conservative outlook and maintains a cash-rich balance sheet, enabling it to take advantage of weak markets. A significant portion of its cost structure is variable and therefore it has largely been able to weather weak operating conditions. In difficult environments property developers have leaned on the company to help generate sales and increase its commission percentage. We believe the company will come out of this slowdown stronger just as it did during prior downturns.

At Royce & Associates, we like to invest in businesses that come out of weak periods stronger. While the growth rate of China may be slowing, we believe that there are ample investment opportunities in Hong Kong-listed companies—still the primary method of investing in public Chinese companies.”

Hong Kong has been a key beneficiary of China’s policy to loosen travel restrictions for its citizens. In 2003, an individual visit scheme was put in place that permits mainland Chinese tourists to visit Hong Kong individually (previously only group tours were sanctioned). Since its launch, the program has expanded to include the residents of 49 mainland cities from four mainland cities, opening eligibility for 270 million people to visit Hong Kong.13 Hong Kong tourist arrivals in 2012 were up 16% year-over-year to 48.61 million, according to the Hong Kong Tourism Board. Mainland China contributed the majority of tourists, with more than 34.91 million arrivals, up 24.2%.14

Hong Kong has also been able to attract businesses eager for access to mainland China. Western businesses that are looking to target China often post their employees in the city. Employees typically find Hong Kong an easy place to live given its large international population, array of international schools, open media, and vibrant restaurant scene. Additionally, mainland Chinese firms interested in tapping the global capital markets quite often have their financial centers in the city. As of late 2012, there were 7,250 mainland and foreign companies running business operations in Hong Kong, a 4.3% increase over 2011.15

While tourism and business growth have had a positive impact on Hong Kong’s economy, they have also caused a staggering increase in commercial rents. In Hong Kong’s Central district, the overall occupancy costs of U.S. $235.23 per square foot per year topped the “most expensive” list for the third consecutive time.16 Hong Kong’s retail space also continued its dominance as the world’s priciest at $4,328 per square foot a month in the first three months of 2013, which according to leading global real estate firm CBRE was nearly 50% higher than second-place New York and about four times as much as Paris or London.17 Foreign retailers view the city as a “stepping stone’ to mainland China and a desirable place to plant flagship stores. I happened to be in Hong Kong during the first outlet opening of U.K. retailer Topshop. In 2012, I saw lines outside the newly opened Abercrombie & Fitch in Central.

Dilip Badlani in Hong Kong's pricey Central District

Several businesses in Hong Kong have seen their margins squeezed as a result of the increasing rents. The strategies that they have employed include limiting their floor space on the ground level of a main street or moving to locations that, while not as prime, are still easily accessible to shoppers. Others have been forced to shutter.

We have seen this rent squeeze affect one of our investments—the second-largest cosmetics retailer in Hong Kong, which has benefited from the large influx of mainland tourist arrivals into Hong Kong. However, its rental expenses as a percentage of revenues have recently hit an all-time high. Management maintains a large ownership of the business and therefore is aligned with shareholders. It has maintained a strong cash-rich balance sheet and has historically had an 80% dividend payout ratio. We believe that over the longer term, rents in Hong Kong will stabilize as a large majority of foreign brands are already present in the city. The number of tourists from China will continue to increase, albeit not at the pace of recent years. This dynamic should favor the company and allow it to enjoy strong prospects.

Since opening up in 1979, China captured the world’s attention with the strength of its economy: 9.6% growth per year. The new leaders of China, however, have targeted a slower growth rate (7.5% growth this year and until 2020)18 as they aim to reduce environmental degradation and achieve more balanced growth. In May, the State Council of China approved measures put forward by the National Development and Reform Commission that include boosting social welfare, taxing products that are resource-intensive and heavily polluting, and expanding levies on natural resources.19

In the first quarter of 2013, the Chinese economy grew by 7.7% and since then there have been a series of disappointing economic reports. In May, China posted its lowest growth rates for exports in a year (up 1%) and imports into China fell (down 0.3%).20 In addition, the HSBC Purchasing Manager’s Index (PMI) was at 48.3 in June, a nine month low which signals a contraction in manufacturing activity.21 Li Keqiang, the new Premier of China, remains unwilling to use government stimulus to meet growth targets. In a speech given to officials in May, he stated, “To achieve this year’s targets, the room to rely on stimulus policies or government direct investment is not big—we must rely on market mechanisms.”22

The government of China has been unwilling to inject fresh liquidity into the banking system; it is focused on financial risks and wants to ensure stability going forward. In reaction, banks have been tightening credit for businesses which are, in turn, feeling the strain. The interbank interest rate surged in June making it harder for companies, especially smaller ones, to borrow money.

Betting on China’s growth in the past has proven to be the right strategy for businesses operating there. However, as its economy matures and growth slows it will not be as easy for businesses to grow. Well capitalized businesses operating with strong management teams who have more targeted growth strategies will be critical to ensuring success on the ground.

One of our investments in China is a leading department store whose management follows this philosophy. It has been operating in China for more than two decades and was among the early entrants into the market. The business model of department stores in China is different from the Western world because the department stores there don’t take as big a merchandise risk. With the exception of cosmetics and the supermarket section, which usually make up approximately 30% of sales, sales are generated via renting space in the department store to concessionaires who then give a percentage of their revenues to the department store owner. Management of the Company is conservative and operates with a cash rich balance sheet. This means the Company can make acquisitions quickly as it does not need to tap the capital markets for funding. It recently was able to complete one such accretive acquisition, and we believe its conservative management philosophy will suit it well going forward.

While the mood on the ground in Hong Kong was not as robust as it has been in the past, I have learned from growing up there that people of the city are resilient and able to weather slowdowns. At Royce & Associates, we like to invest in businesses that come out of weak periods stronger. While the growth rate of China may be slowing, we believe that there are ample investment opportunities in Hong Kong-listed companies—still the primary method of investing in public Chinese companies.

© The Royce Funds