Global policy-makers increasingly at odds with one another

August 30, 2013

- Global policy-makers increasingly at odds with one another

- Foreign exchange reserves may hold key to stabilizing emerging markets

- Geopolitics weigh heavily on energy markets

This week marked the 50th anniversary of The March on Washington. I was but a tot back then, but I’ve viewed Dr. Martin Luther King’s “I Have a Dream” speech many times since. The era, the setting, the words, the spirit: I get chills every time I listen.

Setting aside differences and joining hands… that is a theme I wish economic policy-makers around the world would embrace. Wouldn’t it be grand if Democrats and Republicans; monetarists and new Keynesians; emerging and mature markets; central bankers and legislatures could work together for the common good?

Unfortunately, the tide of cooperation is at low ebb. And global market and economic performance is the poorer for it.

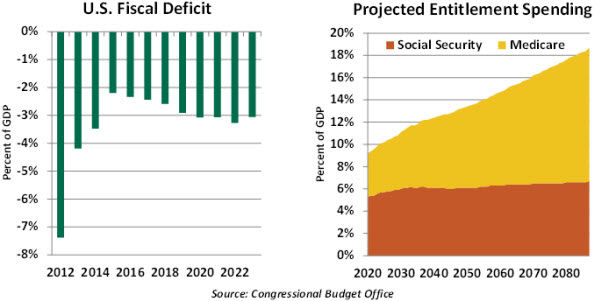

Beginning in the United States, battle lines over the federal budget are once again being drawn. Since the fiscal cliff was averted last January, the intramural acrimony within Congress has been more muted. Thanks to very strong growth in revenue, this year’s American budget shortfall will be the smallest in five years. The latest nonpartisan projections show the deficit remaining at 3% of gross domestic product (GDP) for the foreseeable future.

Some are delighted by this achievement and feel as if there is room to peel back and offer more support to economic growth. Others remain frightened by what lies beyond the next decade, when the costs of retirement and healthcare threaten to overwhelm the nation’s finances.

With the end of the fiscal year just five weeks away, Congress must pass a continuing resolution to sustain disbursements. (Adopting a comprehensive budget would be preferred, but this modest-sounding goal has not been achieved in four years.) Further, recent reports suggest that the U.S. debt ceiling will be reached in October, about a month earlier than previously thought.

Prospects for dealing with these deadlines don’t appear to be the brightest. Treasury Secretary Jacob Lew insists that Congress pay the bills it incurred without modification; House Speaker John Boehner recently said he was ready for a “whale of a fight” over the debt ceiling. Some public posturing is to be expected, but markets may have to brace for stressful interval as summer ends.

A few miles down the National Mall at the Federal Reserve sits a crowd of interested observers whose pursuit of improved employment conditions was hindered by the budgetary restrictions that Congress put into place. With economic growth moving ahead at a decent pace in the second quarter, a tapering of monetary accommodation may be in the offing. But additional fiscal restraint or a fiscal impasse could change that calculus quickly.

The Fed is dealing with its own internal divisions, trying to mediate between those who think that quantitative easing has become either ineffectual or dangerous and those who would prefer to press on. Divides are evident in the minutes of private meetings and in public comments. With so many slots on the Federal Open Market Committee turning over in the coming months, it is difficult to know whether forging consensus around monetary policy will become any easier.

The Federal Reserve and Congress have sniped at each other more and more often since the 2008 financial crisis. Ben Bernanke has not shied away from highlighting the need for more supportive and stable fiscal policy while also taking his share of barbs during official testimony from those who are dissatisfied with monetary policy.

Policy coordination faces a new level of challenges in the international arena. At the recently concluded monetary policy conference in Jackson Hole, Wyo., the governor of Mexico’s central bank said, “It would be desirable to have monetary policy coordination. To have the central banks of advanced economies to go in different directions, can become a source of instability.” Echoing this concern, International Monetary Fund Managing Director Christine Lagarde warned that financial market reverberations “may well feed back to where they began.”

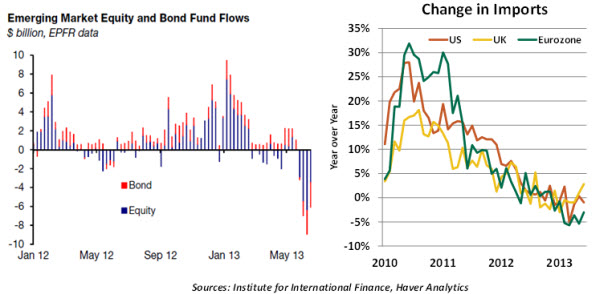

Quite a few observers have tried to lay responsibility for recent emerging market turmoil at the Fed’s feet. This seems like a stretch. While long-term U.S. interest rates have risen, they remain at very modest levels, hardly high enough to induce much capital flight. And it bears remembering that U.S. monetary policy is still extraordinarily easy.

The more plausible root cause is the impact that soft global conditions have had on exports from developing countries. As growth in emerging markets moderates, policy problems that were obscured by recent prosperity come to the surface.

Attempting to optimize policy across a wide range of nations is an impossible task. As a case study, Europe’s once-popular monetary union now finds its members going in different directions and struggling to coordinate a way out of a lingering malaise. The Group of Eight meetings most often produce a lot of pomp but little meaningful policy. Leaders who show too much support for the global collective risk the loss of domestic political support.

So while policy-makers should think beyond their specific realms in setting course, a segregation of responsibilities may be the best way to organize things at present. Ending this sort of segregation would certainly have tested Dr. King’s great powers of inspiration, and sadly, there is no economic heir to that great mantle on the scene today.

Foreign Exchange Reserves – How Much Is Enough?

Of late, foreign exchange (FX) reserves are mentioned frequently in news reports about emerging market developments. This concept is usually the province of economic wonks, but lay people may have to take notice because FX reserves could mean the difference between stability and instability for some countries.

FX reserves largely consist of foreign currencies held at central banks; in some countries the finance ministry is involved. The U.S. dollar is by far the major reserve currency held by central banks across the world, followed by the euro, the pound sterling, Japanese yen and Swiss franc.

FX reserves are earned by exports of goods and services from a country. Central banks hold foreign exchange reserves to be able to purchase and protect the value of their currencies.

The role of foreign exchange reserves is best understood within the context of the exchange rate system. Most countries operate under a flexible exchange rate system or a fixed/pegged exchange rate system, inclusive of several variations between these two extremes.

Under a fully flexible exchange rate system, the price of a country’s currency – the exchange rate – is determined by the currency’s supply and demand. Advanced economies operating with a flexible exchange rate system seldom use foreign exchange reserves to influence the exchange rate, excluding special circumstances.

By contrast, emerging markets hold foreign exchange reserves to manage the value of their currencies and to prevent disruptions in capital market access. Markets compare a country’s trade flows with its holdings of foreign exchange reserves to determine if it has enough to meet its obligations.

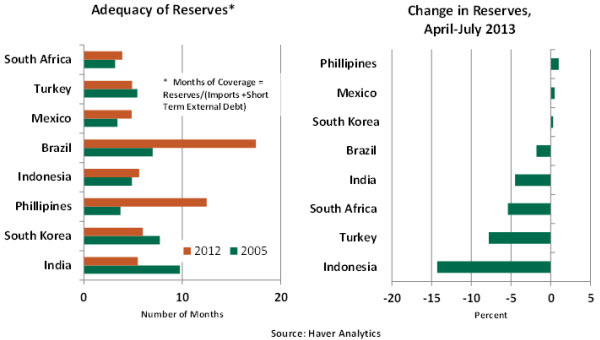

If a country is running a large trade deficit, it will need adequate foreign exchange reserves to pay for imports. Further, it needs a buffer against the potential loss of short-term foreign investment. How much is sufficient for a rainy day? A rule of thumb is to hold enough foreign exchange reserves to pay for three months of imports and outstanding short-term external debt.

In 2012, most of the major emerging markets satisfied this litmus test. This represents a sea change from the status of Asian economies in 1997, when foreign exchange reserves were inadequate to defend their respective pegged rates and several Asian currencies were forced to switch to some form of flexible exchange rate system. This had disastrous economic consequences.

More recently, the trend in reserves has turned more troubling. Several key markets have already spent important portions of their FX buffers in a futile effort to stabilize their currencies. Indonesia, Turkey and Brazil have been among the most active in intervening, and these countries face additional depletion as their trade deficits widen. There is talk that emerging markets are working on coordinated intervention in the foreign exchange market to contain losses; even if they do, success is not guaranteed.

Foreign exchange reserves are like a canary in the coal mine, chirping warning signals about emerging markets. Markets will, therefore, track foreign exchange reserves closely in emerging markets during the months ahead.

Higher Oil Prices – Economic Fundamentals or Fear?

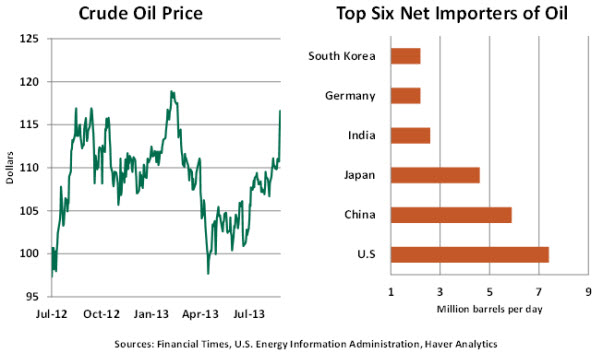

Brent crude oil is trading at $115 per barrel (bbl), up from $99 in April. Some suggest the high for oil prices is not here yet. Why is the price of crude oil moving up?

Starting with the fundamentals, much of the world economy is operating in either first gear or reverse gear. Overall tepid global business conditions rule out demand for oil as the major driver of the recent jump in oil prices. Moreover, near-term projections of economic growth are lackluster for major advanced and emerging economies.

Warning signals from other related market indicators are absent. The six-month oil futures contract is trading around $110/bbl, while the two-year contract is quoted at $98/bbl. If demand were the driving force, prices of other commodities associated with strong business momentum would be trending up. On the contrary, broad commodity indexes are trading roughly 4% below their year-ago readings.

From the supply side, production setbacks in Libya and Iraq have affected the supply of oil, but they are not of the order that is close to a supply shock – yet.

Clearly, the political turmoil in Egypt and Syria, which could carry over to the region as a whole, has raised the risk of a supply disruption. As tensions escalate, so will the price of crude.

Central bankers will be in a tight spot as they try to factor into policy the impact of higher oil prices. Countries with high energy imports and depreciating currencies will fare the worst; monetary authorities in several emerging markets have been forced to raise rates in the face of declining economic fortunes.

It is unfortunate and ironic that energy stress is occurring in selected parts of the world amid reports of a potential global energy glut. What this reinforces is that the energy market is not completely global, given the costs and challenges of production and transportation. One can only hope that peace advances and prices per barrel fall… and the sooner the better.

© Northern Trust