Manufacturing surveys are upbeat, but should we trust them?

September 6, 2013

- Manufacturing surveys are upbeat, but should we trust them?

- The August employment report leaves lots of room for improvement

I am one of the few remaining traditionalists who balances my checkbook every month. The task has become much more challenging over the years, what with the proliferation of electronic bill payments and debit card purchases that my wife refuses to record. Fortunately for our finances, she rarely deigns to record her paychecks, either.

Reconciling numbers is sometimes a difficult thing. Economists are struggling, at present, to reconcile very encouraging reports on the manufacturing outlook with relatively soft readings on consumption. If demand is modest, why does prospective supply seem to be so strong?

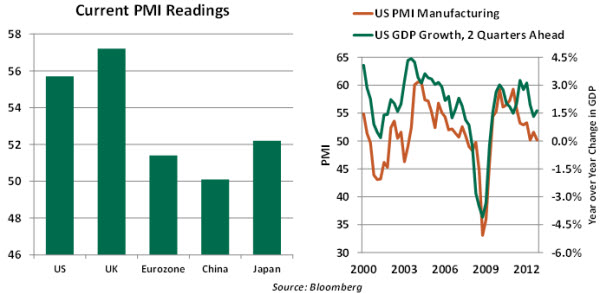

The happy side of the current conundrum is a series of national Purchasing Managers Index (PMI) reports from key areas. These readings suggest strong manufacturing activity in the months ahead, and they have been reliable leading indicators of overall economic performance.

This predictive power leads analysts to pay a good deal of attention to PMI readings. Interestingly, though, the process used to assemble them is far from a hard science.

The PMIs are assembled through a survey, not a hard count of economic output or production schedules. In the United States, 400 managers are polled and asked to indicate simply whether conditions are better, worse or the same as they were during previous months.

The responses are then scored: 1 for better, 0.5 for the same and 0 for worse. The results are aggregated across survey participants, and that outcome is multiplied by 100 to get the index. A reading of above 50 is interpreted as a sign of expansion; below that, retreat.

The design has some potential flaws. By limiting respondents to three options, the survey may not capture the intensity of advance or decline being observed. Further, the U.S. edition of the PMI does not weight responses by the size of the firm. (International versions of the PMI do.)

Finally, manufacturing accounts for only about 13% of U.S. gross domestic product (GDP) and about 16% in the European Union. So the manufacturing PMI gives direct evidence on a fairly modest fraction of the overall economy. In recent years, purchasing manager indexes covering the service sector were introduced but have yet to garner the same following.

Still, PMI levels seem to provide very broad insight into economic conditions. Respondents often have a unique window into future trends, gleaned from the incredible amounts of data they gather or license. Technology has greatly deepened the link among sales, inventories and orders over the past generation, providing foresight in real time.

Still, PMI levels seem to provide very broad insight into economic conditions. Respondents often have a unique window into future trends, gleaned from the incredible amounts of data they gather or license. Technology has greatly deepened the link among sales, inventories and orders over the past generation, providing foresight in real time.

It was partly on the basis of strong PMI readings that the Bank of England and the European Central Bank opted to keep their monetary policies on hold this week. While both contemplated changes to their forward guidance and quantitative easing programs recently, positive signals put those steps on the back burner.

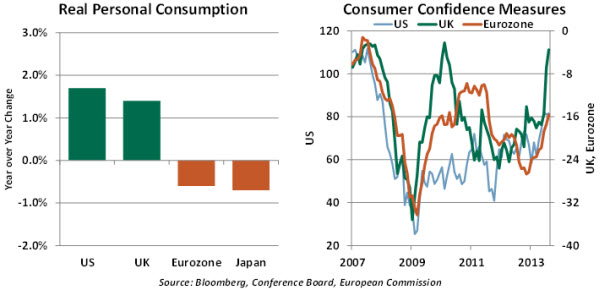

Perhaps purchasing managers are seeing something promising on the horizon. But for the present, their end customers are still proceeding with caution. Spending growth has been tepid, at best, over the past year.

One need not look far for the root causes of soft consumption. Unemployment is still elevated in the developed world; income growth has been modest, especially among the middle classes; and the damage done to some household balance sheets has enforced a new ethic of saving. Consumers in the United States remain averse to taking on much leverage; revolving debt (which includes credit cards) has grown by only 1% over the past 12 months.

Nonetheless, surveys of consumer confidence reflect expectations of better things to come. Measures for the United States, the United Kingdom and the eurozone have all improved during the summer.

It isn’t unusual for households to share optimism in response to a survey while remaining conservative with their wallets. Unlike the PMIs, consumer confidence surveys do not have a reliable tie to economic activity and are often far more volatile. So reconciling sentiment with sales is challenging at present.

It is also difficult to reconcile the outlook of purchasing managers and households with some of the potential worries on the horizon. The tension in the Middle East raises the prospect of broad conflict and has already resulted in much higher oil prices. The prospect of a renewed fiscal imbroglio in the U.S. Congress is similarly dispiriting. Uncertainty over monetary policy, and its potential effect on world markets, is high.

I would certainly like to embrace the notion that better economic times are ahead. And I have to tip my hat to purchasing managers, who collectively have a great track record at foreshadowing economic turns. But for now, the numbers aren’t quite adding up.

As I do at home when this happens, I’ll have to spend some time looking for the debit or credit that I am missing. When I find out what that is, I will be sure to let you know.

Laboring to Show Improvement

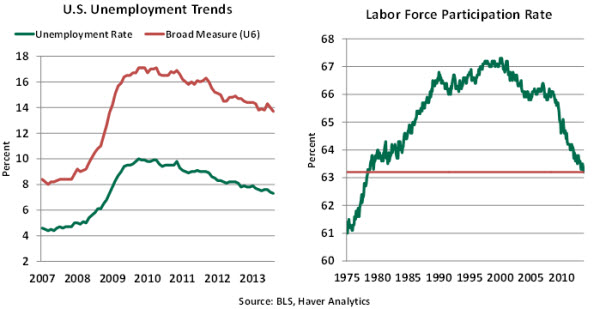

The U.S. unemployment rate ticked down one notch to 7.3% in August, and payroll employment moved up 169,000. These headlines hide the softening picture of the labor market.

Starting with the jobless rate, it fell for all the wrong reasons. The participation rate – the sum of those working and those seeking employment as a percent of the working-age population – declined to 63.2% in August, the lowest since May 1978.

A persistent decline in the participation rate is worrisome because it represents a change in the labor force that will affect the potential capacity of the economy if it fails to reverse course. Some of the recent fall is for secular reasons (retirement, for example), but it appears that some people who want jobs are giving up looking for them.

The median duration of unemployment shot up to 16.4 weeks in August, up from 15.7 weeks in the prior month. The share of long-term unemployment also rose to 37.9%, the highest level in the last five months. Overall, labor market metrics from the household survey are sending a pause signal to the Fed as it debates a reduction of asset purchases.

The median duration of unemployment shot up to 16.4 weeks in August, up from 15.7 weeks in the prior month. The share of long-term unemployment also rose to 37.9%, the highest level in the last five months. Overall, labor market metrics from the household survey are sending a pause signal to the Fed as it debates a reduction of asset purchases.

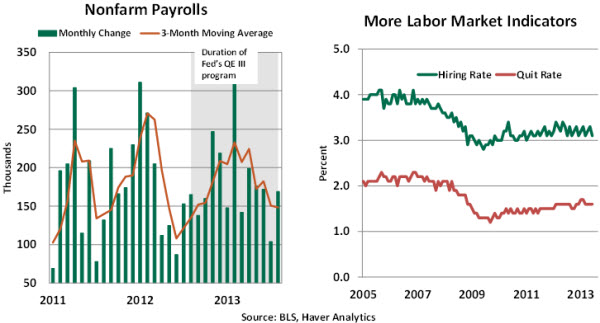

The numbers from the establishment survey also point to a softening trend in hiring. Revisions of payrolls for the prior two months resulted in a net loss of 74,000 jobs. Factory employment rose 14,000, while construction jobs were unchanged. Private service-sector employment advanced 134,000, the smallest monthly gain for the year. A deceleration in private service-sector hiring in the past few months is part of the reason for the softening of labor market conditions.

Federal government employment held steady during August, state government jobs slipped slightly and local government hiring rose 20,000. These numbers suggest that the impact of sequestration has faded away.

The workweek increased 0.1 hour to 34.5 hours in August; hourly earnings rose by 5 cents to put the year-to-year gains at 2.2%. These numbers combined with employment data point to a moderate increase in personal income during August.

Payroll employment is averaging a gain of 148,000 in the last three months, the lowest since September 2012 when the Fed announced the asset purchase program that remains in place today.

At the September 17-18 Federal Open Market Committee (FOMC) meeting, the Fed will look at labor market indicators beyond the headlines of the August employment report.

The official estimate of 11.3 million currently unemployed does not include 866,000 discouraged workers who say they have given up looking for work. In addition, roughly 8 million indicate they are working part-time even though they prefer full-time jobs. The number of discouraged workers has moved up slightly since the Fed began the third round of quantitative easing, and part-time employment has moved down by less than 150,000 in the same period.

The official estimate of 11.3 million currently unemployed does not include 866,000 discouraged workers who say they have given up looking for work. In addition, roughly 8 million indicate they are working part-time even though they prefer full-time jobs. The number of discouraged workers has moved up slightly since the Fed began the third round of quantitative easing, and part-time employment has moved down by less than 150,000 in the same period.

Also, other indicators of labor demand – the quit rate and hiring rate – do not indicate a firming of employment conditions. The latest hiring rate (3.1% versus roughly 4.0% during the previous expansion) has yet to make a significant stride from the levels seen during the Great Recession. The quit rate (1.6% versus 2.0% before the recession began) is low and denotes that workers lack the confidence to quit because they do not expect to be rehired.

The persistent decline of the participation rate suggests that reaching the 7.0% unemployment rate threshold that the Fed deems appropriate to end the asset purchase program and the 6.5% jobless rate threshold that would initiate considerations of a higher federal funds rate may occur sooner than anticipated.

However, it would not represent the same strengthening of the labor market that would be the case if these thresholds were attained with a higher participation rate. So, the Fed may be forced to revisit the unemployment thresholds indicated in its forward guidance of monetary policy.

The Fed has reiterated on several occasions that tapering of asset purchases is tied to the status of the economy and is contingent on an improvement in the labor market outlook. Putting all the major labor market indicators together, the main conclusion is that the labor market is not strengthening. Therefore, in our view, it is hard to justify tapering at the September FOMC meeting.

© Northern Trust