Taper Vs. No Taper - Let's Meet Somewhere In The Middle

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…)

To Taper or Not To Taper…

Volatility in the US equity and bond markets has risen since Ben Bernanke and the rest of the Federal Reserve Board mentioned thepossibility of taperingits bond purchase program - in other words, a potential end to the "free ride" the Fed has been giving investors.

However, economic data is still weak and a reduction in economic stimulus by the Fed may harm the US economy.

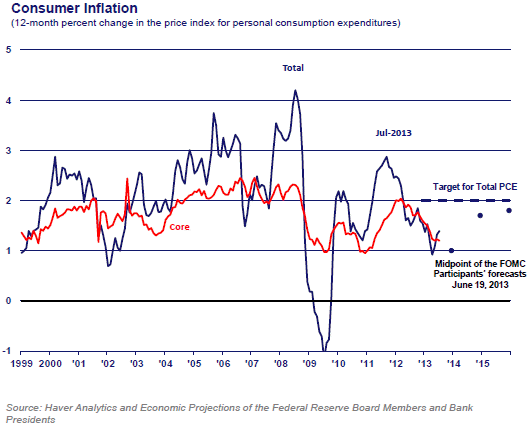

The Fed Mandate

In 1977, Congress amended The Federal Reserve Act, stating the monetary policy objectives of the Federal Reserve as:

"The Board of Governors of the Federal Reserve System and the Federal Open Market Committee shall maintain long run growth of the monetary and credit aggregates commensurate with the economy's long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices and moderate long-term interest rates."

Fed projections (provided by the Federal Reserve Bank of Chicago) show future target rates for inflation and employment rising, and gives the Fed a compelling reason to slow down its stimulus program by tapering the purchase of US bonds in order to keep long-term interest rates low.

However, current economic data shows that the projections may be a bit optimistic

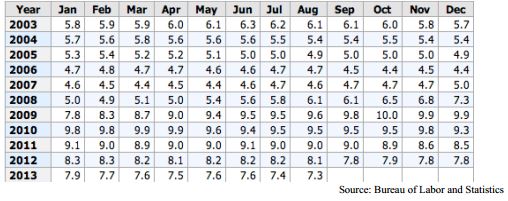

Weak Economic Data Continues

Last week's unemployment number declined to 7.3%, continuing a downward trend in

unemployment since 2011:

The problem the Fed is facing, however, is the actual unemployment rate may be

much higher than what the “official” rate shows.

Variable Purchases/Tapering May Be What's Coming Next

Job creation, year to date, remains lower than in 2012. In 2012, a monthly average of

182,000 new jobs were created. In 2013, the average has dropped slightly to 180,000

jobs per month.

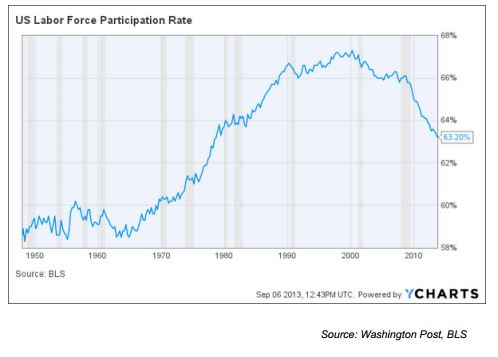

In fact, the actual cause of the drop in unemployment may not be that more people

are finding work, but that more people are giving up.

The participation rate in the labor force continues to drop (those who are not actively

looking for work are not labeled as unemployed):

Popping The Bubbles Before They Get Too Big

The question facing investors is if the employment picture is not really improving, then

why would the Fed slow down its stimulus program?

The Fed may be worried about future inflation spikes caused by bubbles forming in

the economy due to a perception of risk-free money – for example in the US stock

market.

Investors continue to drive the stock market to record highs despite any real growth in

corporate earnings. The idea that the Fed will continue to put an ever rising floor on

equity prices has created a perceived environment of practically risk-less investing.

This environment has allowed stock market multiples to expand dramatically without

any real earnings growth.

Variable Taper/Purchase

Going forward we may see the Fed try to keep investors more on their toes by

introducing a more “variable” taper/purchase program.

The average annual amount purchased by the Fed may remain the same (only time

will tell), but we may see Bernanke and company start to adjust purchase amounts

more frequently – thus giving the illusion of tapering without damaging the fragile US

economy.

By adding this element of the unknown, the Fed may be hoping to remove the

perception of risk-less investing in equities and any other bubbles that may be forming

in the US economy.

Disclosure

This is provided for information purposes only and should not be used or construed as an indicator of future performance, an offer to sell, a solicitation of an offer to buy, or a recommendation for any security. Riverbend Investment Management, LLC (Riverbend) cannot guarantee the suitability or potential value of any particular investment.

Risk Disclosures: The goal of Absolute Return money managers is to achieve positive returns regardless of those earned in financial markets or shown in benchmarks. They seek to do this, using non-traditional investment techniques and asset categories. Of course, there can be no guarantee that any investor will achieve the goal of the managers, that profits will be made, or even that losses will be avoided. Strategy and asset allocation decisions may not always be correct and may adversely affect account performance.

The use of leverage may magnify this risk. Leverage and funds employing derivatives carry other risks that may result in losses, including the effects of unexpected market shifts, default and/or the potential illiquidity of certain derivatives. Bonds are affected by changes in interest rates, credit conditions, and inflation. As interest rates rise, prices of bonds fall. Long-term bonds are more sensitive to interest-rate risk than shortterm bonds, while lower-rated bonds may offer higher yields in return for more risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. Additional risks are listed in Advisor's Brochure Form ADV, which will be provided by advisor and which prospective investors are encouraged to read. As individual tax rates vary, taxes have not been considered. Various minimum holding periods for each fund may be utilized to comply with trading restrictions. As supplemental information, a listing of all assumed trades and other data used to generate the referenced results is available upon request. Inquiry for more current results is advised. Inherent in any investment is the potential for loss as well as the potential for gain. A list of all recommendations made within the immediately preceding year is available upon written request. The investment return and principal value of an investment will fluctuate; investors' shares, when redeemed, may be worth more or less than their original cost. Actual performance may be materially lower or higher than the performance shown.

PAST RESEARCH REPORT RESULTS DO NOT GUARANTEE FUTURE RESULTS.

Copyright 2013 Riverbend Investment Management, LLC. All Rights Reserved.

http://riverbendinvestments.com