Five years ago, I spent the weekend in the office with a group of very anxious people. I recall the Chicago Bears football game playing on a TV in the conference room, but no one was paying attention to it. It was a different bears’ game that worried us.

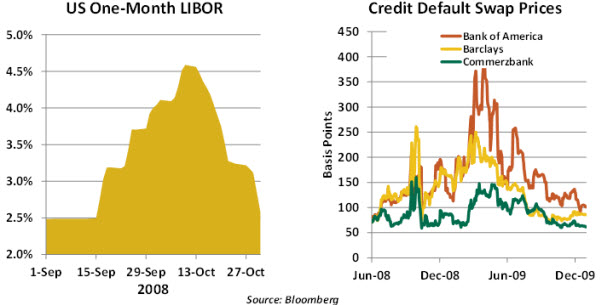

The first cracks in the new paradigm of prosperity had appeared more than a year earlier when two subprime mortgage funds sponsored by Bear Stearns collapsed. Bear Stearns itself fell in the spring of 2008, and IndyMac followed in July. The financial markets had been unsteady throughout the summer, and the solvency of key institutions became the subject of intense speculation.

We had tried for months to anticipate what might transpire, playing out a series of scenarios and trying to plan strategy for each of them. But when Lehman Brothers failed the following Monday morning, reality outstripped even the most pessimistic projections.

No matter where you were or what you were doing at the time, that fateful fall was a defining interval. We all endured a roller coaster of disbelief, panic, anger and exhaustion. We ultimately weathered that terrible storm and set the groundwork for recovery. And we vowed to learn from the experience so it would be much less likely to recur.

One would hope that we’d be back to normal by now, but all evidence suggests that the remnants of the global financial crisis are still very much with us. Economic conditions seem stuck at a new, more modest normal, and efforts to reform the financial system have shown mixed results at best. Perhaps it’s a good time to revisit that fateful time, see how far we’ve come and determine how far we have yet to go.

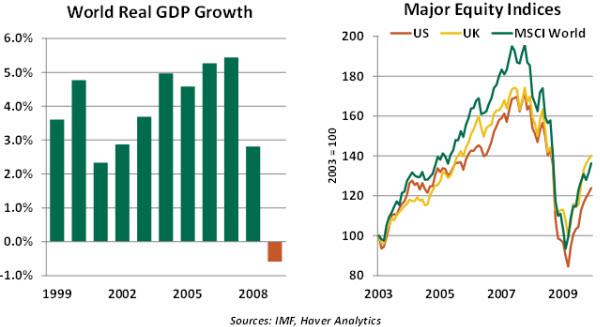

We’ve almost forgotten, but the years leading up to the crisis were enormously successful. Economic and market performance through 2007 was stellar.

Unemployment had been driven to very low levels. The eurozone was a great success, and emerging markets were… emerging. We dared to think that management innovations and enlightened policy-makers had made the global business cycle obsolete.

As it became apparent that this assumption was untrue, the market corrected swiftly. People and financial statements which had been highly trusted could no longer be counted on. Rumor traveled faster than fact.

The demand for liquidity went well beyond what could have been anticipated. With short-term credit constricting, players resorted to selling assets into already-distressed markets to raise money. A negative cycle reinforced itself through collateral calls and cash shortages. Trust was a scarce commodity, and the pricing of credit-sensitive products reflected that.

Policy-makers raced to gain understanding and forge the tools needed to contain the damage. And that they did, throwing almost everything against the wall and hoping at least some of it would stick. Federal Reserve Chairman Ben Bernanke said at the time, “There are no atheists in foxholes and no ideologues in financial crises.” Governments that had tried to draw a dark line between the private sector and the public sector nonetheless used taxpayer funds to support faltering financial institutions. Stabilize first; philosophize later.

There are certainly those who look back and question some key decisions made in the heat of the moment. Among the benefits of having avoided the worst is the luxury of reflecting critically on that period. But it is an imperfect exercise. Choices made in the autumn of 2008 were based on incomplete information and under the worst pressure.

Economic performance in recent years has left a lot to be desired, but it certainly could have been far worse. The success of crisis policy is the distance between the depth of the abyss we were gazing into and the modest elevations we’ve reached since – not the gap between where we are and normal economic peaks. And in the United States, almost all special crisis programs have made money without even accounting for broader economic benefit.

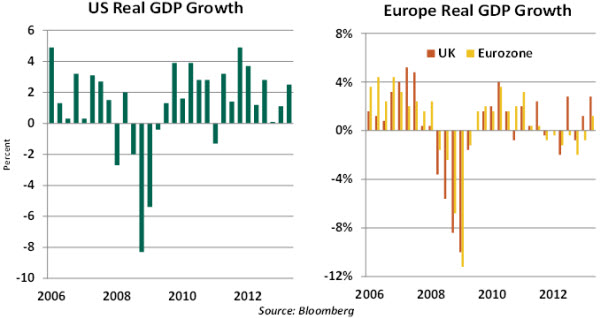

In their widely noted book, “This Time Is Different,” Carmen Reinhart and Kenneth Rogoff find that it takes a long time to recover from economic downturns associated with financial trauma. The current cycle seems to be proving them right.

Growth in the major economies has struggled to reach long-run norms, leaving millions of people unemployed. Slack demand from American and European consumers has, in turn, taken a steep toll on developing economies, which rely on exports for growth. In both cases, economic retreat revealed fiscal stress that led some to cry out for rectitude at a time when countercyclical government spending may have been more appropriate.

There is little doubt that restrictive fiscal policies have hindered global recovery. Encouragingly, though, growth seems to have taken the upper hand from austerity in many national budget battles. Well-structured fiscal investments have the potential to pay off handsomely and are to be encouraged.

By contrast, central banks have pursued a more supportive course. Novel approaches like quantitative easing and forward guidance about policy are now conventional. The zero lower bound for interest rates has not constrained monetary expansion.

The creativity and courage that characterized central bank strategy over the past five years has been hailed by many but it may have reached its limits. The incremental benefits of quantitative easing seem to be shrinking, and fears of bubbles down the road are rising. The market tumult which greeted the Federal Reserve’s hints at tapering suggests that exit from all the accommodation may be a very messy process.

When it set out on the course of quantitative easing, the Fed was certainly aware that unwinding the program ultimately might be very challenging. This is a better problem to have than the one that stared us in the face five years ago. But monetary recovery won’t be fully complete until central bank balance sheets have receded to pre-crisis levels. That could take a number of years.

On the bright side, equity markets in many parts of the world have performed exceptionally well since hitting bottom in the spring of 2009. Household wealth in the United States hit a new peak in the most recent quarter; while many rightfully worry about the distribution of this bounty, aggregate spending power provides a good platform for growth.

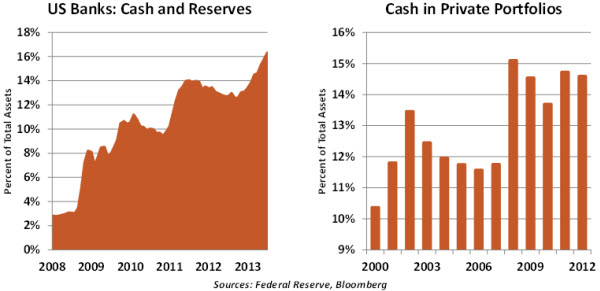

Some wonder, however, how much longer equity markets can improve at rates that are multiples of economic growth. If top-line revenue remains constrained, asset returns may be, too. Further, the mantle of risk aversion that has its roots in the financial crisis remains in place. All this time after the crisis, banks and investors are keeping vast sums in liquid investments which are earning negative real returns.

As soon as the worst had passed, legislatures took steps to ensure that we never, ever have another crisis. Thousands of pages of new financial regulation were drafted, with many thousands more to come. Among the key goals of the effort are:

-

Getting more capital into banks. Leverage can become a performance-enhancing drug for a time, but if it becomes scarce, the withdrawal can be especially painful. Higher capital requirements are being required by regulators worldwide, and stress testing is being liberally applied. In the United States, capital ratios among large banks are almost twice what they were entering the crisis.

In the long run, this should limit the possibility that one firm’s failure will be society’s undoing. But in the short term, lending is being impaired in many parts of the world as banks continue efforts to repair their balance sheets. Further, one wonders how long it will be before the next generation of financial engineers finds a way around the new rules to create leverage that will be harder to see.

It is critically important that we eliminate situations where profits are private and losses are public. Among the forthcoming case studies on this front will be the reform of Freddie Mac and Fannie Mae, which is just now getting attention five years after the two were bundled into the government’s warm embrace.

-

Better appreciation of the interconnectedness of markets and institutions. Who was exposed to whom and for how much? This basic question was one that few could answer accurately five years ago. Without knowing how dense the forest was, policy-makers didn’t know where a firebreak could be trenched.

Today, financial stability units within central banks are collecting data that enable them to map the network more effectively. And many products whose opacity was a problem in 2008 have been brought into the light, and their volumes subsequently have fallen.

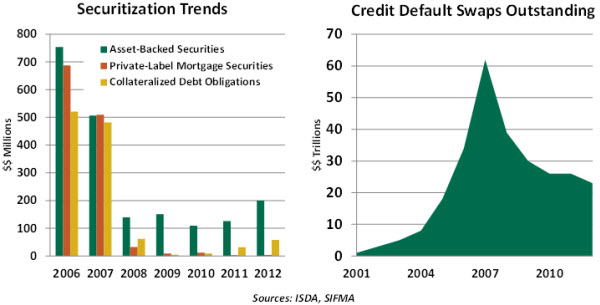

I suspect that few outside of the investment banking community will mourn the halving of the credit default swap market; these instruments became known as financial weapons of mass destruction. But the virtual demise of securitization for all but conventional U.S. mortgages may be a sad development. Well-structured, transparently marketed asset-backed securities are attractive to investors and bring lower costs and greater access to borrowers.

If the originate-to-distribute model is no longer valid, then the pressure on banks to re-intermediate all the credit they spent 25 years selling will be acute. It is not clear whether they can meet this goal, and if they can’t, credit will be harder to obtain and economic growth will be more modest.

As a final thought on this front, the crisis brought financial modeling from the heights of sophistication to the depths of disdain. Assumptions of normal distributions fail when abnormal events occur, and the past is no longer prologue. Sometimes, the skill in using models is knowing when to turn them off; a healthy balance between quantitative and qualitative methods must be sustained.

-

Reinforcing liquidity. No matter how secure that finances may appear on the surface, institutions and individuals can’t survive for long if their financial supporters lose confidence in them. And your assets are worth what the market thinks they are, even if prices may seem divorced from fundamental value. As economist John Maynard Keynes once observed, markets can be wrong longer than you can stay solvent.

Some still debate whether 2008 was a crisis of solvency or liquidity. The distinction may not be that important; either can be fatal, and the two are inextricably linked. Financial companies are, therefore, being asked to keep more liquidity on their balance sheets and to write “living wills” that attempt to outline an orderly resolution should they become imperiled.

For the present, few think that a systemically important firm could be unwound in an orderly way. That day may come, but it seems far off. But the value may lie in the journey and not the destination. The exercise may reveal to bank boards that their firms have become too big and too complex to manage and prompt steps to scale the organization accordingly.

As regulatory efforts progress, rule-writers should keep in mind that the next crisis is unlikely to resemble the last one. Closing one trap door may open others down the road. Further, the banking industry is not a public utility and shouldn’t be turned into one by overly invasive reforms.

In sum, a grade of “incomplete” might be appropriate for efforts aimed at recovering from the crisis of five years ago. The world economy has moved ahead but continues to underperform its potential. Unemployment has fallen but remains far higher than desired; millions of experienced and young workers have been searching for far too long. There are no large banks in imminent danger of failure, but many are struggling to regain a clean bill of health. Reform efforts are incomplete and their impact unclear.

We’ve learned a lot from the experience, but there are certainly lessons we’ve yet to master. As tempting as it might be to dismiss the experience of 2008 as a bad dream, we must seek to hold it in our consciousness long enough to appreciate all it has to teach us. For those of us who lived through that interval, it won’t soon be forgotten.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

© Northern Trust