U.S. economic growth averaged roughly 2.0% in the first half of the year and the average gain of real gross domestic product (GDP) during the entire 16-quarter economic recovery is 2.2%. Real GDP is projected to grow close to this trend in the second half of the year.

The good news is that domestic tailwinds from a healthy banking system and a recovering housing market should remain powerful. Fiscal restraint, which has been significant, should soon be easing. But the upcoming budget drama in Washington threatens; while it appears that we will not face a government shutdown the debt ceiling negotiations could be contentious.

The labor market will remain front and center in the months ahead because the path of Fed policy is tied to changes in employment. Next week’s Fed meeting will offer fresh insights from the central bank, with new projections of economic performance of particular interest.

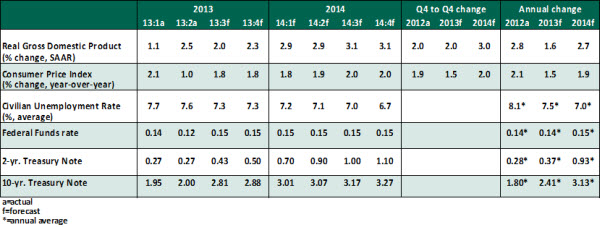

Key Economic Indicators

Key elements of our forecast:

- Major components of consumer spending are on different tracks. Auto sales rose to 16.1 million units in August. Year-to-date auto sales numbers point to a solid increase in 2013 to around 15.6 million units, the highest level in the last six years. However, the non-auto component of consumer spending posted significantly sluggish growth of 1.9% in the second quarter compared with an historical average of 3.4%. Soft service sector outlays should trim the pace of spending in the third quarter, followed by a pickup in the final three months of the year.

- The 125 basis point increase in mortgage rates since the low in May has translated to a decline in the volume of mortgage applications (both purchase and refinance) and bodes poorly for home sales. Sales of existing homes started on a strong note in July (+6.5%), but sales of new homes plunged (-13.4%). Home prices continue to advance at a rapid clip. The housing sector numbers are under close watch. Continued employment gains and the new cycle high for the homebuilder survey in July strike a positive note.

- The Institute of Supply Management’s (ISM) August survey recorded a sharp jump in the index tracking new orders to the highest level since April 2011. Historically, the year-to-year change in orders of capital goods has a strong positive correlation with new orders of the ISM survey. The latest improvement in the index of new orders bodes positively for capital spending in the third quarter.

- Government spending, in general, is expected to trim real GDP growth as the final aspects of sequestration are put in place. A continuing resolution to fund the federal government should pass, but debt ceiling discussions likely will result in market volatility as we approach mid-October when the nation’s statutory debt limit will be reached.

- The second quarter’s sharp 8.6% rebound in exports is not projected to be repeated during the balance of the year. The large reduction in industrial production in the eurozone in July is a reminder that the region is likely to take a few steps back for every step forward. Our forecast assumes a subdued pace of growth in exports in the next two quarters.

- Labor market data should be major market-moving news in the next few months, given that Fed policy is tied to the outlook of the labor market. The downward trend of the participation rate is the unsolved puzzle. A small turnaround of the participation rate from the August low (63.2%) is widely expected. This forecast would imply that the jobless rate could hold steady or move up, depending on the pace of labor force growth and job creation.

- The overall risks to economic growth have changed somewhat since the monthly update in August. The situation in the Middle East continues to be a wild card in economic activity projections. Economic headwinds from Europe and China have moderated, while the increase in interest rates is an additional burden to businesses and households.

- We continue to believe that a September tapering of asset purchases is a close call, given the nature of income economic data. Our most likely case remains one in which tapering begins in December. In the meantime, markets have interpreted the prospects of tapering as tightening and interest rates have moved up rapidly. A strong clarification about the difference between the two is in order. The Fed’s missive on September 18 should help to sort out a few unknowns.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

© Northern Trust