Global deleveraging has a long way to go

September 20, 2013

- Global deleveraging has a long way to go

- Fiscal drama and the economy

- Funding for economic statistics needs to be enhanced

When I was a younger man, I was deeply into sports statistics. I could rattle off scoring marks and world records across a variety of countries and athletic endeavors.

Three things conspired to curb my enthusiasm. First, I became a dad, and portions of the hard disk that is my brain had to be repurposed to remember trivial things like my children’s birthdays and concert schedules. Second, sports metrics became more complicated as performance could be broken into ever-finer elements. And third, performance-enhancing drug use by athletes made me wonder whether they set the records, or whether the pharmaceuticals did.

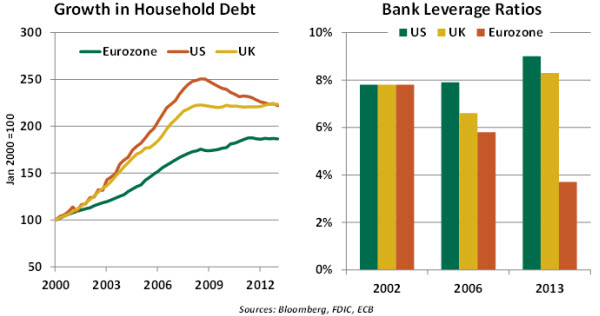

Leverage was the performance-enhancing drug that allowed consumers, businesses, banks and governments to set records that have since been called into question. To continue our reflection on how well we’ve recovered from the financial crisis, it’s worth seeing where we stand in bringing leverage down to more manageable levels.

The inventory will show us that this effort is still very much a work in process. While some borrowers are in much better condition than they were five years ago, the balance sheets of others are still heavily laden with debt. These burdens could limit spending, and therefore economic growth, for years to come.

The early part of this century was characterized by rising fortunes and falling interest rates. Rising asset values seemed to offer plenty of security for borrowing, and very modest carrying costs made payments eminently affordable. The move to low rates was initiated by easy monetary policy and accelerated for some countries by the implementation of the euro and rising investor enthusiasm for emerging markets.

Banks aided and abetted this trend, leveraging their own positions to offer leverage to others. The ratios shown above may actually understate this trend, because they do not fully reflect the substantial off-balance-sheet activities that many financial institutions had undertaken.

Rather than serving as a check on this activity, regulation actually provided a tail wind. International capital standards allowed the use of models, which showed increasingly benign results as the business cycle gained strength. Some supervisors embraced the notion that markets would mete out discipline if excess appeared, and declined to provide it themselves.

The reversal of asset price increases reversed this best of all possible worlds. And almost overnight, debt that seemed manageable became much less so. Austerity set in at many levels, and remains largely in place today.

The belt tightening that ensued has been quite painful. While the cost of carrying consumer debt has fallen in most of the world, the amounts of debt outstanding remain elevated. The lion’s share of household debt buildup came in the form of home mortgages, which have very long maturities and take a long time to pay off.

The belt tightening that ensued has been quite painful. While the cost of carrying consumer debt has fallen in most of the world, the amounts of debt outstanding remain elevated. The lion’s share of household debt buildup came in the form of home mortgages, which have very long maturities and take a long time to pay off.

The recovery in house prices has helped to reduce the number of homeowners who are “underwater” on their loans, but that still leaves them with large principal balances to pay. While foreclosures have tapered off, the U.S. still has a backlog of more than 1 million awaiting dispensation.

High levels of unemployment, very modest wage growth, and the need to rebuild retirement savings will certainly limit the ability of many households to deleverage. We may be five years into a 10-year process of balance sheet repair at this level.

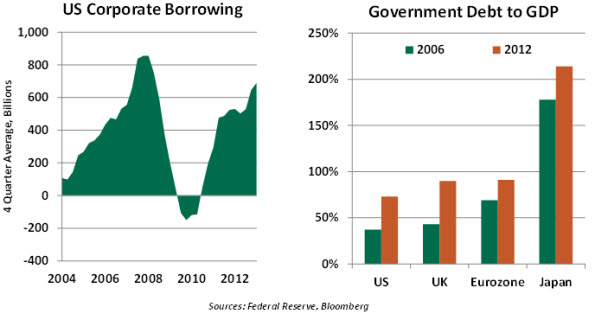

Corporations, for the most part, brought their indebtedness under control fairly quickly. (Some very large companies have achieved this with the help of their governments or through the bankruptcy process, but these are exceptions.) Firms moved rapidly to reduce their reliance on leverage after the crisis, and have returned to it less because they need it and more because it is far cheaper than other forms of financing.

At the public level, deleveraging is far off in the future. Many countries, in fact, continue to add to their indebtedness at an unsustainable rate. One hopes that this will generate growth that will defray the debt, but the spending restraint recommended by prudence or forced by international investors has been, and will remain, a limiting factor for economic progress.

Many certainly expected deleveraging would take quite a bit of time, given the huge buildup of borrowing and the depth of recession. But time may be getting short; with some global interest rates on an upward march, the carrying cost of credit may soon follow suit. And this will make the challenge of deleveraging even more difficult.

Addiction is a serious subject, and recovery takes a lot of time and hard work. But it is a path that must be followed, because the alternative is entirely unpleasant. The reward will be economic and market performance that we can trust is genuine, not artificial.

The Annual Fiscal Battle in Washington

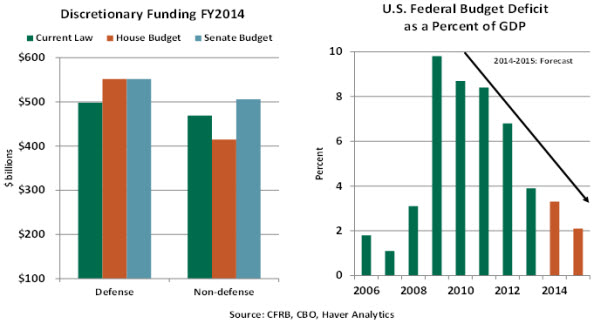

In the next few weeks, the debate over the U.S. federal budget will grab headlines. The most pressing matter is funding the federal government and related appropriations for fiscal year (FY) 2014, followed by the approach of the national debt ceiling.

The federal government will shut down on October 1 if Congress fails to pass appropriations bills or put in place a continuing resolution. The latest rhetoric from Washington suggests a temporary continuing resolution that runs through December 15 will most likely pass. However, the contents of the short-term continuing resolution and details of appropriations for the rest of FY2014 will be contentious.

Per current law, spending cuts based on the Budget Control Act of 2011 (which introduced the concept of the sequester) will result in reduced discretionary appropriations of $20 billion in FY2014 to $967 billion. The FY2013 sequestration came in the form of across the board cuts in both mandatory and discretionary spending. For FY2014, Congress can arrange expenditure reductions as it chooses, as long as the top line target is met.

Per current law, spending cuts based on the Budget Control Act of 2011 (which introduced the concept of the sequester) will result in reduced discretionary appropriations of $20 billion in FY2014 to $967 billion. The FY2013 sequestration came in the form of across the board cuts in both mandatory and discretionary spending. For FY2014, Congress can arrange expenditure reductions as it chooses, as long as the top line target is met.

There is a wide gap between the goals of the House and Senate and they are consequently promoting different options, which will have varying effects on the deficit trajectory. Ideally, a comprehensive budget that includes a realistic path for debt and a more permanent setting of the debt ceiling would be the best plan; unfortunately, this outcome has a very low probability. Realistically speaking, a short-term fix at the sequester levels appears most likely.

The second challenge for Congress is to raise the current statutory debt limit of $16.7 trillion by mid-October, when projections suggest that we will run out of room to borrow. The current state of these negotiations is not constructive, with Republicans demanding a delay in the implementation of the Affordable Care Act (ACA) in exchange for a higher debt limit.

Market volatility is a given as these discussions evolve in the very near term. Failure to meet debt obligations for political reasons will have a far more significant impact on markets than a temporary government shutdown.

Market volatility is a given as these discussions evolve in the very near term. Failure to meet debt obligations for political reasons will have a far more significant impact on markets than a temporary government shutdown.

Stepping away from the short-term fiscal drama, expansionary fiscal policy was widely accepted as necessary after the financial crisis broke out in 2008, but it has fewer advocates now. The difference in opinion is mostly due to a failure to differentiate between short-term and long-run effects of expansionary fiscal policy.

The fear that accumulated debt and associated high interest rates which might “crowd out” private sector investment is one argument marshaled in favor of fiscal austerity. This is sound economic reasoning; however, it is inapplicable in the current situation.

At present, the economy seems starved of demand, so incentives to lift demand are still suitable. At the same time, policies dedicated to promoting long-term growth like investments in infrastructure, education and research should be a focus of long-term fiscal policy.

Finally, broad fiscal issues like broad tax and entitlement reform deserve attention, but will likely not be solved in the upcoming round of negotiations. The political calculus simply does not seem to allow for a reasoned discussion on these two subjects. But the entitlement calculus is especially critical to long-term fiscal health, and cannot be ignored indefinitely.

The fact that the United States and other advanced countries can still raise money at historically low interest rates buys time for fiscal policy plans. But the window for success is getting narrow. Excessive political partisanship may prove very expensive in the long run.

Good Data, Good Decisions

During challenging budgeting times, everything deserves a hard look. But in one case, I would recommend a hard look at increasing, not decreasing spending.

One of the more important elements of any budget is revenue growth. In the broad case of our federal budget, revenue is critically dependent on gross domestic product and costs are often driven by inflation. Forecasting these with any accuracy requires sound information on output and prices. Further, the wisdom and performance of key economic policies can only be evaluated ex ante and ex post with relevant readings on the results.

A handful of statistical agencies in Washington do yeoman’s work to provide this information for the benefit of both public and private users. The Bureau of Economic Analysis, the Bureau of Labor Statistics and the Census Bureau are central to this effort.

Measuring the economy has not gotten easier over time. The shift from industries that are easy to count (manufacturing, mining, agriculture) to those that are more difficult (banking, health care) has required careful thought and new collections of information. The agencies have become very resourceful about this; they’ve embraced the use of technology aggressively to remain as efficient as they can.

Measuring the economy has not gotten easier over time. The shift from industries that are easy to count (manufacturing, mining, agriculture) to those that are more difficult (banking, health care) has required careful thought and new collections of information. The agencies have become very resourceful about this; they’ve embraced the use of technology aggressively to remain as efficient as they can.

Unfortunately, the funding for these efforts has fallen, by 5% in the most recent fiscal year. And the sequester threatens more reductions in 2014.

In lean times, budget line items that are investments look like costs. The returns that accrue to the devotion of dollars are often overlooked. But in the case of economic statistics, a very modest devotion of additional resources would help us keep up with some very critical variables and pay for itself by enabling more precise management of the economy. Here’s hoping that Congress is not penny wise and pound foolish on this front.

© Northern Trust