Merkel’s win is unlikely to lead to any changes in the Eurozone

September 27, 2013

- Merkel’s win is unlikely to lead to any changes in the Eurozone

- Extra lift from exports is not guaranteed

- Robust growth is a challenge in India, Brazil and Indonesia

For most of this year there had been a tacit assumption in Europe that major decisions regarding the eurozone’s future would have to wait until after the September 22 German federal election. This has duly returned Angela Merkel to the post of Chancellor, but the makeup of her government will not be decided for weeks. Pressing eurozone issues such as further debt relief for Greece or creating a banking union will not be tackled in earnest until the end of this year. Even so, the stance that Germany takes on these issues is unlikely to be any different.

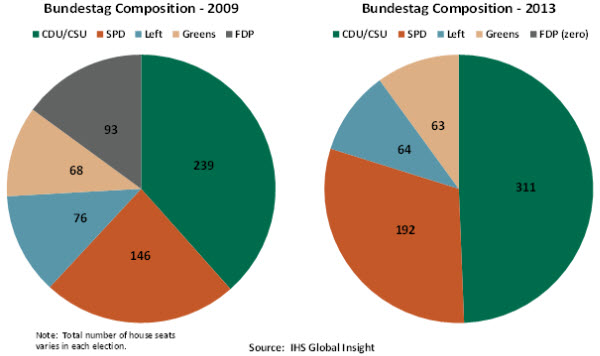

Let’s start with the domestic politics. The morning after the election, the headlines hailed the triumph of “Mutti” (Mother) as Merkel’s Christian Democratic Union/Christian Social Union (CDU/CSU) enjoyed its best result in decades, just five seats shy of an outright majority. In contrast, the center-left Social Democrats (SPD) suffered their second-worst performance in post-war history. The Free Democrats (FDP), junior partner in the 2009-13 coalition, collapsed altogether, failing to hit the 5% threshold needed to claim seats in the lower house.

A CDU-SPD grand coalition seems likely; but in the last such coalition in 2005-09 the parties had a similar number of seats and the SPD still suffered its worst ever result in the 2009 election. This time the party is clearly in Merkel’s shadow and leery of joining a coalition only to lose votes again in the 2017 election. The SPD may even leave Merkel to go it alone. Given that it took 65 days to reach a coalition agreement back in 2005, the negotiations will take at least as long this time around.

Whatever the outcome, we will not see major changes either in Germany’s own fiscal policies or in the country’s stance toward fellow eurozone members. Domestically, both the SPD and CDU are bound by constitutional debt limits and commitments to existing objectives. This leaves little room to maneuver in terms of meeting eurozone partners’ demands to stimulate German domestic demand. Economically, Germany remains the eurozone powerhouse; previous reforms have boosted its competitiveness and lowered its unemployment rate.

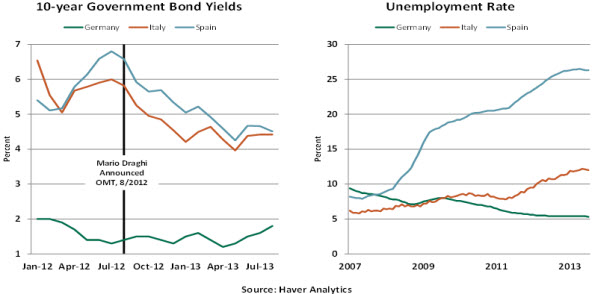

When it comes to relations with the rest of the eurozone, the Federal Constitutional Court has already weighed in on the parameters of aid to other sovereigns and would nix anything that looks like debt forgiveness. Next month the Court will rule on the constitutionality of the European Central Bank’s Outright Monetary Transactions (OMT) bond buying program, which is credited with bringing stability to the eurozone markets over the past year without even being used. An adverse ruling from the German Court could become a major headache for Merkel and the rest of the ‘zone, roiling the markets without any changes in economic fundamentals.

Having the SPD in government will not prompt Germany to forgo demanding reforms from others in return for aid. The party supported all the austerity measures demanded over the past few years. More to the point, the government will be constrained by the anti-euro Alternative for Germany (AfD), a party created only a few months ago that came close to winning parliamentary seats. The AfD wants to break up the currency zone and cease aid to Greece. Along with other euro-protest parties across the EU, the AfD will gain a platform in the May 2014 European parliament election, when voters are more willing to support “fringe” parties.

Most important, a grand coalition in Berlin will not mean a shift in Germany’s stance on the pressing issues facing the eurozone: the creation of a banking union and the need for more financial assistance for Greece and Portugal. Banking union involves the creation of a eurozone-wide resolution agency to break the toxic link between sovereigns and national banks, avoiding a repeat of the problems seen in Ireland and Spain where hefty banking sector liabilities overwhelmed the public debt. The SPD seems more inclined to push for such a union, but Germany will not change gears on this issue. A comprehensive banking union would trigger rulings from the German Constitutional Court; it would also mean eurozone-wide scrutiny of Germany’s own troubled regional “landesbanks.” Instead, Berlin will likely accept a more limited solution, with the cross-border resolution agency only having authority over the largest 130 eurozone banking groups (which will be directly supervised by the ECB from next year).

Finally, whatever her government’s composition, Merkel will have to use her vaunted mediation skills to steer Germany and its partners through two upcoming challenges. It is widely acknowledged that Greece will need another round of financial aid next year, to meet a €4 billion funding “gap” in its current lending program. Portugal is approaching the end of its three-year International Monetary Fund-European Union (EU) bailout program but is unlikely to be able to return to full market funding by mid-2014. Both countries have such hefty public sector debt burdens that it is hard to envisage either one returning to sustainable growth without some form of debt forgiveness. Merkel will be constrained in this not only by the AfD nipping at her heels but also by the Constitutional Court.

With German coalition negotiations likely dragging well into the fourth quarter, the October 24-25 EU summit is likely to focus on the banking union question. The difficult decisions about aid and debt relief for Greece and Portugal will have to wait until the summit in mid-December. Meanwhile, Italy’s political instability could trigger a government collapse in Rome at any time, while in France sluggish growth and reluctance to reform will continue to challenge the outlook for the region.

The German election was a watershed for Merkel personally, but once the coalition negotiations are done nothing will fundamentally change where the rest of the eurozone is concerned.

Insights from Trends in U.S. Exports and Imports

World trade collapsed after the 2008 global financial crisis, inclusive of a sharp plunge of U.S. imports and exports. Has the momentum of U.S. exports and imports been restored after the recovery? What messages are embedded in post-crisis trade flows? These two questions are explored here.

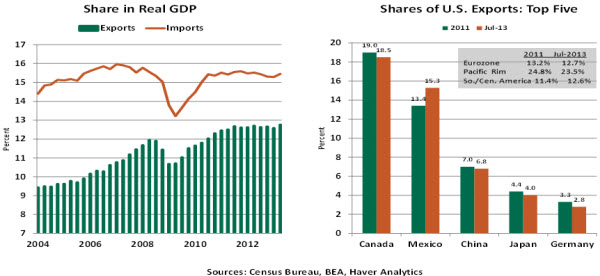

In absolute terms, the inflation adjusted levels of exports and imports of goods and services are both significantly higher than the pre-crisis peak, while the share of exports and imports in gross domestic product (GDP) has a different story to tell. The share of exports of goods and services has marched past the peak registered in 2007 (see chart), while the import share is yet to match the high seen in 2007.

A careful inspection shows that the share of exports shot up in the early stages of the recovery but has barely budged since the third quarter of 2011. The small uptick in the second quarter of 2013 reflects a surge in petroleum exports; not clear if this is a durable trend.

Digging further into details of exports, weak economic conditions in the last two years among major trading partners of the United States, excluding Mexico and parts of South America, have inflicted damage on export shares.

Exports to the eurozone made up 15% of U.S. exports in the early part of the recovery. This share dwindled to a low of 11.7% in February 2013; a small turnaround is in place. Tepid growth in the eurozone will not be adequate to lift exports to this region.

Exports to the Pacific Rim (China, Japan, Malaysia, Australia, Indonesia, Philippines, South Korea, and a few others) peaked at 25.5% of U.S. exports in 2010, only to lose momentum as these economies shifted to a lower gear. The latest reading of export share to the Pacific Rim is 23.5%, with the export volume to China and Japan slipping.

Pulling together export data, the main conclusion is that growth in the euro area and Pacific Rim will play a role in lifting U.S. GDP growth. If these economies falter, the U.S. economy stands to suffer a setback.

U.S. imports have regained most of the momentum lost during the Great Recession. Canada, China, Mexico, Japan and Germany are the top five sources of imports to the United States. Import share of Canada slipped in 2012 but year-to-date numbers point to a pickup.

Data for the first seven months of the year suggest that imports from China could be a slightly smaller percentage in 2013 compared with 2012. Imports from Mexico and Germany advanced in the January-July period. In fact, latest data of imports from Mexico point to the possibility of a record showing in 2013.

Overall, the import numbers suggest that the economic recovery has worked favorably for most major trading partners of the United States. Projections of U.S. economic growth imply that imports should continue to support economic activity of trading partners of the United States.

The U.S. trade deficit in the second quarter stood at $424 billion, down from $455 billion in the final months of 2011. The smaller trade gap reflects a 4.0% increase in exports and a 2.0% gain in imports in the last six quarters. Petroleum exports account for a part of this improvement. Judgments about the longevity and size of benefits from the oil sector are still evolving.

Although exports have weathered the storm reasonably well, the economic status of our trading partners will, at the margin, tip the headline GDP numbers in the quarters ahead.

India, Brazil, and Indonesia – Strong Growth on Hold, For Now

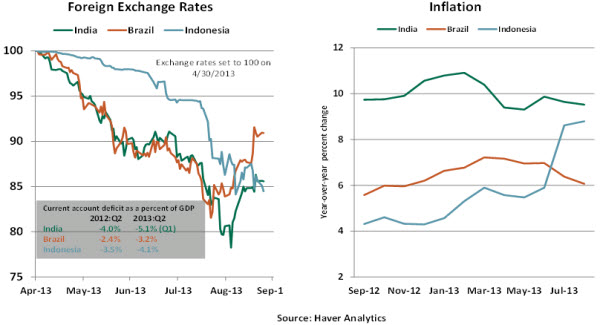

Last week, the Reserve Bank of India raised its main policy rate 25 basis points to 7.50%. The central banks of Brazil and Indonesia tightened monetary policy during August. These central banks have acted to protect their currencies and contain inflation with higher interest rates even though their economies are experiencing lackluster economic growth.

At the low point in the last five months, the Indian rupee had dropped 22%, followed by a small gain in recent days. The Brazilian real registered a nearly 19% loss between May and August 21 (the day before the central bank intervened), while the Indonesian rupiah has plunged 16% in the last four months. If the central banks had failed to act, a depreciating currency would translate into higher import prices and an additional hike in consumer prices when inflation is already problematic in these countries.

Inflation in Brazil is close to the top-end of the central bank’s preferred range of 2.5%-6.5%; higher readings prevailed until the last two months. Indonesia’s inflation numbers are far above the central bank’s target range of 3.5% - 5.5%. Inflation in India has held around a troublesome 10% pace during the past 12 months.

These three emerging markets are also experiencing a noticeably wider current account deficit compared with readings a year ago. A change in investor preference and ensuing capital flight prompted central bank tightening policy actions in order to boost investor confidence, reverse capital flows, stem the loss of currency values and contain inflation.

But this policy panacea for these economic woes has the downside of weakening economic growth. From an investor’s perspective, these emerging markets with worrisome current account deficits, problematic inflation and soft growth prospects are an unattractive investment option, for now.

The tide should turn as these economies stabilize. It is also too early to predict a precise time frame for a reversal of capital flows to these markets. But, we can say with a good deal of confidence that the pace of economic growth will determine the volume of new capital flows to these markets.

© Northern Trust