Many investors have expressed concerns over the quality and general integrity of financial reports filed by Asian companies. Often cited as a reason to be less trusting are less stringent regulatory laws that have created a historical culture of accepting transgressions in corporate governance. Complicating matters are the size and maturity of capital markets in the region, particularly when compared to more advanced economies. Also, there are challenges faced by minority shareholders from company executives unaccustomed to outside interests in the management of their company. All of these are real concerns for investors in the region, and in many cases, can only be addressed through experience in different countries, industries and cultures—and even the variety of families that run each business.

As fundamental investors, being able to understand the myriad of complex accounting practices used in Asia, and ultimately being comfortable with them in order to make investment decisions, is critical for firms like ours. In what will be a series of commentaries, we will aim to dissect in more detail the often esoteric approach taken by many Asian companies to financial reporting and the communications around earnings management. This first issue will focus on “the numbers” and begin by looking at how we evaluate the quality of financial reporting. It will also explain what the role of forensic accounting—the process of taking a deeper look into a company’s accounting practices—plays within our firm.

At Matthews, the consistency with which a management team applies sensible and responsible accounting rules during both good times and bad is something we constantly evaluate and this presents a useful starting point for our discussion. Areas we pay specific attention to include determining whether the accounting policies a company elects to use increases management’s influence in setting executive compensation. For example, a company that incentivizes management with 10% growth in earnings per share (EPS), might see a consistent 10% improvement in its EPS year after year. In this instance, less volatile patterns of EPS are suspicious and we would tend to take a closer look into this area of their books.

We also pay attention to free cash flow generated by a company. While free cash flow is a fairly simple concept (cash flow from operations less capital expenditures), we tend to focus on those instances in which a company boosts cash flow from operations. For example, securitizing account receivables gives an exaggerated picture of the sustainable cash flow generated.

Related party transactions are another key area of concern. We tend to closely monitor these disclosures and try to understand the economic rationale behind these transactions. Corporate balance sheets are another factor to consider. For instance, there are many times when investors focus solely on the income statement. However, management might bypass the income statement altogether, and this may pose another red flag if the firm has unrecognized losses on its balance sheet without a credible economic explanation.

Choices in Economic Realities

My job as an analyst involves trying to peer beneath the financial statements to find the true value of a company’s assets, liabilities and earnings power. Companies publish financial statements to communicate the economic reality of their firm to outsiders—these include interested parties such as equity holders, creditors, customers, employees and the government.

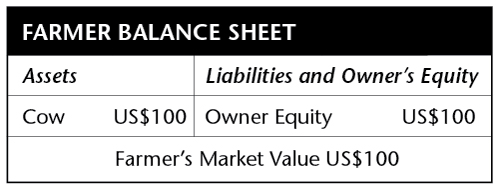

Given that each business is unique in many respects, generally accepted accounting standards offer management teams numerous accounting choices. An ethical management has to choose between multiple options. The illustration below explains that it is not always feasible to reflect economic reality, despite management’s best efforts. Imagine a simple business—a farmer who has no other assets than cash of US$100 and no liabilities. The farmer buys a cow for US$100.

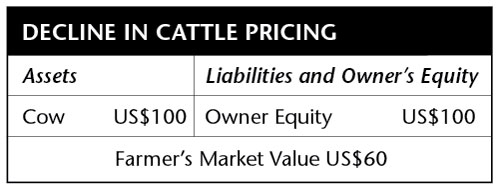

Decline in Price of Asset

Subsequently, the cost of cattle drops and the cow is now worth US$60. Let us assume that this drop is temporary for a period of two to three months. Nevertheless, the economic reality is that the farmer’s asset has declined in value. Therefore, does the farmer recognize a loss of US$40 and revalue his assets to US$60?

An argument against this devaluation, and a valid one at that, is that the farmer has a buy and hold strategy – i.e., he does not plan to sell the cow in the foreseeable future. Therefore, the farmer sees no value in reducing his net worth (which might lead to other adverse consequences). Irrespective, the market value of the cow is now US$60. Here, we have the economic value (as shown by market value) less than the stated book value.

Increase in Fair Value Price of Asset

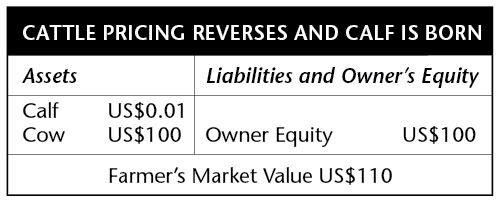

Let us now assume that the cattle market reverts and the market price of the cow is back to US$100 at the end of the three-month period. There is also more happy news for our hypothetical farmer. The cow gives birth to a calf worth US$10. The principles of conservatism in accounting state that since there were no significant expenses incurred in the calf’s coming into existence, the calf (at best) has a token value ($0.01) on the balance sheet.

Necessarily, the balance sheet of the farmer remains the same, despite having a calf that is worth US$10 on the market. The market value of the farmer is US$110 though the book value remains at US$100. i.e., the farmer will sell the cow and calf only for a price greater than US$110. Here, we have the economic value greater than the stated value.

We see in this example the difficulty that can arise in analyzing accounting statements to understand the true economic worth even when management is not indulging in creative accounting practices. Moreover, despite the efficiencies of the market mechanism, market prices might not reflect what the man in the street would think of as normal prices, especially at times of stress. With this as a backdrop, we now consider cases in which companies are actively “creative” in reporting numbers.

Why do Companies Manage Numbers?

There are many reasons why management teams may be incentivized to manage earnings. These incentives cover both monetary and non-monetary benefits for insiders. Typical reasons include to meet market expectations, to save face and to increase executive compensation payouts.

Sometimes, companies smooth earnings by saving windfall profits for a rainy day. This is possibly less deleterious even though this behavior is a form of accounting manipulation. Some executives pursue this approach because companies that show stable earnings are looked upon favorably by investors.

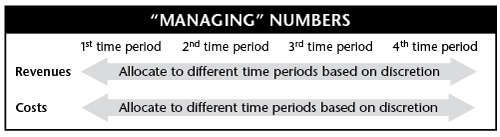

The typical means of “managing” numbers (without resorting to outright fraud) falls into two categories:

- Move revenues across time periods—either recognize revenues before they should be realized, or postpone recognition to a later time. The former increases revenues for the current period at the expense of a future period’s revenues. The latter does the opposite.

- Move costs across time periods—either capitalize costs and postpone recognition to a later time or expense costs before they ought to be recognized. The former increases profitability for the current period at the expense of future period’s profitability. The latter does the opposite.

In both cases, the attempt by management to move revenues/costs across time cannot be sustained indefinitely. So, for instance, when the expensing of a cost is postponed, it cannot be postponed forever. Down the line, management will be forced to incur a higher expense than it otherwise would have. As the next section will highlight, the decisions to move revenues/costs across time periods and the subsequent impact on financial reports are often influenced by a country’s accounting rules together with the motivations of management.

Move Revenues Across Time Periods

Accounting rules provide flexibility in how much a company recognizes as revenues in a particular period. This is especially crucial in industries where long gestation projects are the norm. As an illustration, assume a contract of US$100 million signed for five years during which management uses a “percentage of completion” method. In this method, management has to estimate the total cost of the project, which is anticipated to be US$60 million, resulting in an overall profit of US$40 million.

In the first year, if managers identify that the firm has incurred US$12 million in costs for the project, which works out to 20% of the estimated budget, the company can recognize 20% of the total contract of US$100 million as revenues (US$20 million) and US$8 million as profits. Now, instead, assume there were slippages and the costs incurred were US$18 million in the first year. However, despite the cost overruns, management decides that the eventual total cost of the project is unchanged. The company can now recognize 30% of the value of the project, US$30 million, as revenues, and US$12 million as profits in the first year—simply because it has spent 30% of its costs. Hence, paradoxically, a project that is beyond budget can be shown to have much higher revenues and profits in the earlier period (though of course, the effect reverses by the end of the project).

Another means of moving revenues across time periods is through the use of related party transactions. In order to meet revenue targets, the company might incentivize distributors to pick up inventory, a process known as channel stuffing. Similarly, if a customer is a related party, the company can arrange for financing to the customer through a bank by providing a corporate guarantee. In turn, the customer buys the company’s products and services, thereby generating revenues. Related party transactions are a particular cause for concern in Asia, given that traditional values encourage intermingling of family ties and business interests.

Move Costs Across Time Periods

A common example of moving costs across time periods is expensing versus capitalizing costs. Let’s say that a firm’s management is deciding between two options: capitalize expenses as an asset in the first year of US$100 or expense completely during the first year. Here, capitalizing expenses in the first year will make the income statement that year look better. Profits will be higher than otherwise. However, the company eventually will have to expense this asset in a later year, resulting in lower profits for that year.

An Asian utilities company I was once researching was capitalizing its interest expense. The company’s reporting was nuanced and its decision to capitalize interest correctly reflected the economic reality. However, the interest expense in the income statement appeared suspiciously low and was showing a loan yield of 4%, whereas the normalized loan yield was 7%. The reason for this was because nearly half the interest expense for the year was capitalized. These details were hidden in the footnotes. An investor forecasting earnings using the interest expense as disclosed in the income statement would have had a misleading optimistic picture showing much higher cashflows.

Making Sense of it All

Some of the methods for managing earnings include moving liabilities off balance sheet and bypassing the income statement altogether to make changes directly on the balance sheet. As in any country, outright fraud is typically extremely hard to detect. Therefore, the best way to avoid these situations is to focus on a management team’s track record over a long period; we analyze whether management is taking money out of the company—usually in the form of padding capital expenditure or by padding procurement of products and services.

The process of forensic accounting provides another peek into the companies we select. In several instances, more than any material discrepancy, understanding management’s application of accounting choices helps us glean how it prioritizes long-term benefit versus short-term pain. We tend to like companies that invest for the long term. Accounting choices that demonstrate this intent are yet another supporting point in our research process. None of this, however, is a guarantee against outright fraud or manipulation—and it is ultimately just one of many tools we use. Nevertheless, it helps to provide a more rounded picture of each investment.

Sudarshan Murthy, CFA

Research Analyst

Matthews Asia

The views and information discussed in this article are as of the date of publication, are subject to change and may not reflect the writers' current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of any securities or any sectors mentioned herein.

The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. Matthews International Capital Management, LLC does not accept any liability for losses either direct or consequential caused by the use of this information.

© Matthews Asia