Closing the books on the U.S. budget… for now

October 18, 2013

- Closing the books on the U.S. budget… for now

- Do we need a debt ceiling?

- Study of financial market function earns the Nobel Prize

To be quite honest, we are weary of talking and writing about the U.S. budget saga. We share the general disappointment in the conduct seen over the past two weeks, and there are important issues here and overseas that have been crowded out by the circus in our Capitol. Nonetheless, here are some final thoughts on the American fiscal situation.

- The extension of the debt ceiling may last longer than initially thought. The limit has been suspended through February but may not become truly binding for a while thereafter. Federal receipts are usually quite strong from January 1 through our personal income tax date on April 15, limiting the Treasury’s need to issue new securities. Depending on how cash flows, the next debt ceiling stress may not occur until late next spring.

That timing might be fortunate politically, as it would delay the next round of wrangling until after the spring primaries. That might offer some additional room for compromise.

- The American government was the subject of scorn from a wide array of foreign capitals. U.S. Treasury securities are widely held in Asia, and U.S. equities are a key part of portfolios around the world. The threat that political dysfunction here could diminish the value of those assets prompted sharp rebukes.

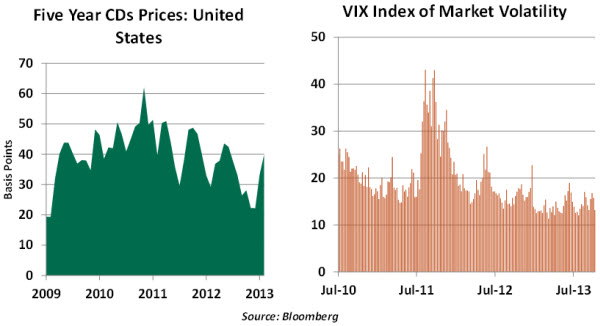

While the rhetoric reached significant peaks, market-based trouble signals were more muted. Credit default swap prices on the United States rose just a little bit but will likely recede quickly, if past patterns are any guide. Measures of market volatility barely budged. Neither escalated anywhere near as much as they did during the debt ceiling crisis of summer 2011.

Analysts seemed united in their expectation that things would get worked out by the 11th hour, and so they stayed the course. So this sorry episode may be costly to the country’s reputation but not to market performance.

On the one hand, the resilience of markets is impressive and reassuring. On the other, it is worrisome. A bit more bearishness might have brought more pressure to bear on policy-makers, signaling the consequences of their inaction. And if, one day, we fail to meet a deadline, the correction could be alarming.

- Having just gotten back to work, the statistical mills that produce economic indicators are facing a significant backlog. In some cases, raw information is in hand, awaiting compilation and review. In others, data collection is significantly behind schedule. The much-anticipated employment report for September, delayed since October 4, will be released next Tuesday. But there could be a delay of up to two weeks in the release of some other measures.

When the figures are eventually released, they will need to be taken with a grain of salt. Sample periods may not match intended schedules, potentially limiting responses and complicating seasonal adjustments. The impact of the shutdown on some series, including those related to the job market, could be significant.

We’re all anxious to see how well the economy held up during the shutdown and how much activity was lost during those two weeks. But it may be quite a while before the information is clean enough to make a determination.

- For this reason, the Federal Reserve may further delay the tapering of its quantitative easing program. Officials have said repeatedly that policy will be data-driven; without reliable data, it will be harder to make a firm case for altering policy.

At its September meeting, the Federal Open Market Committee (FOMC) cited fiscal uncertainty as one of the reasons for sustaining the pace of asset purchases. Uncertainty has been reduced in the short-term but may arise once again when the government’s spending authority expires in January. So it is not clear that this week’s resolution will completely relieve the FOMC.

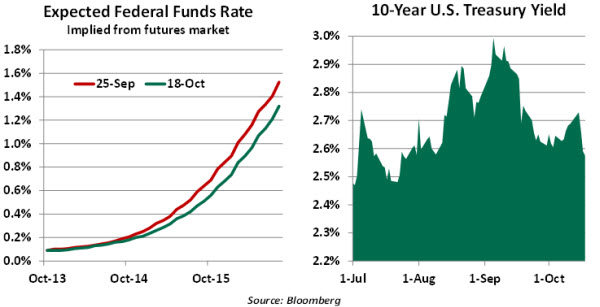

Markets have consequently pushed out their expectations for changes to monetary strategy. The 10-year U.S. Treasury yield, which is quite sensitive to the outlook for quantitative easing, has dropped by more than 40 basis points since early September.

It may fall, therefore, to Janet Yellen to contemplate initiating the tapering program as she begins her watch. The pressure will be high from the very start.

Debt Ceiling Double Jeopardy

The United States is the only nation with a debt ceiling. In our view, this is not a claim to fame.

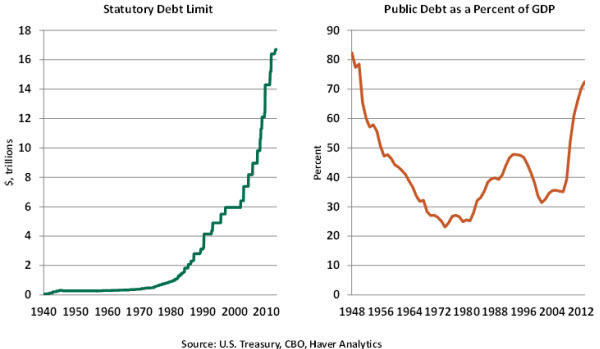

The federal debt ceiling, put into place in 1917 as the country was preparing for war, was originally designed to place limits on specific borrowing instruments. In 1939, Congress enacted the aggregate limit on overall public debt. Disagreements about the debt ceiling are a part and parcel of Congressional practice, but the debt ceiling stand-offs in 2011 and 2013 were particularly severe.

At first blush, the notion of a debt ceiling is peculiar because Congress passes bills that determine spending and taxes. When combined with economic developments, these decisions influence the federal budget deficit. How much the nation borrows is really determined by the budget process, and adding a debt ceiling on top of the process can be viewed as somewhat redundant. From a rational standpoint, the debt ceiling should be tied to the budget passed for each fiscal year, if we need to have a debt ceiling at all.

Further, the debt ceiling has been raised 75 times in the last 50 years, which begs the question of whether it is truly a ceiling.

Arguing to cap the debt at a certain level is not a sign of thrift if spending and tax bills are not consistent with it. All that the debt ceiling seems to have done in the last several years is create an artificial brink that raises risks for the markets and the economy. While politically unlikely, eliminating the debt ceiling has a lot of attraction.

Nobel Laureates: Bringing Science to Portfolio Management

When I was a graduate student at the University of Chicago, it was said that one went there to seek Fama and fortune. At the time, Eugene Fama was breaking new ground with statistical work into the performance of assets, earning him the moniker, “The Father of Modern Finance.”

On Monday, Fama shared the Nobel Prize in economics with Lars Peter Hansen and Robert Shiller. All established great reputations by studying data to better understand market function; this technique was revolutionary at the time they started but has become second nature today.

Among Fama’s contributions is the efficient market hypothesis, which is often misunderstood. There certainly have been questions raised since the 2008 financial crisis about the collective wisdom of markets, but that experience may actually bolster Fama’s conclusions.

At its root, the efficient market hypothesis says that investors collectively analyze and incorporate news into asset prices quickly. As conditions change, so do markets. The speed of adjustment, and the rewards that accrue to those with better information, make it very difficult for individual investors to beat the market with stock-picking.

This finding gave rise to index funds, which simply mirror market aggregates as opposed to managing actively to earn incremental returns. Index funds have become a huge part of institutional and personal portfolios.

During the crisis, new information – much of it unfavorable – was coming at a very rapid rate. Distributions of expectations were moving to the negative. And so from this perspective, the market correction that ensued was not entirely irrational. The fact that markets have recovered since then is likely the result of more uplifting information as opposed to investors regaining their poise after losing their heads.

Reading Fama’s seminal text, “The Foundations of Finance,” was not pleasant at first. It is dense with Greek letters. But the concepts within have proven immensely powerful. Our congratulations go out to all of this year’s winners and to the Swedish Academy for making an enlightened set of selections.

© Northern Trust