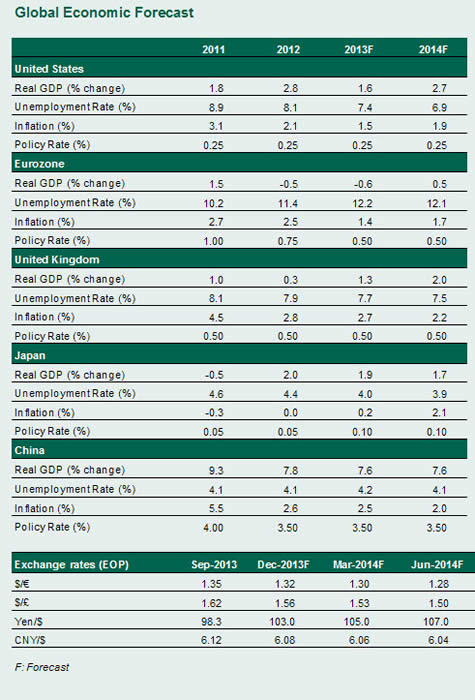

UNITED STATES

The United States avoided a fiscal accident after Congress struck a deal to end the partial government shutdown and bought time to resolve differences over the federal budget. Assuming political discord will not result in another standoff, the U.S. economy is projected to show steady and stronger growth in 2014 compared with 2013. The unemployment rate is predicted to gradually trend down, while inflation is unlikely to be problematic and should hold within the Federal Reserve’s 2% long-term target. The Fed is expected to commence a reduction in asset purchases in early 2014, assuming fiscal uncertainty is not on the horizon. Headwinds from China and the eurozone are less threatening compared with the situation three months ago. A recovery of the lost ground for the dollar should follow after the budgetary impasse led to a decline in the value of the greenback vis-à-vis major currencies.

EUROZONE

Tentative signs of recovery continue to emerge across the eurozone, with this year’s contraction likely to turn positive in 2014. However, the pace of growth remains very uneven across the region. Germany’s real gross domestic product (GDP) growth will likely accelerate to 1.5%-plus in 2014 from 1.0% in 2013, but growth in France will likely be no more than 0.5% in 2014 after a nearly steady reading in 2013. Italy is expected to remain mired in recession well into next year; Spain will fare little better. Inflation is expected to remain very subdued in Europe. The European Central Bank will likely keep the refi rate at the record low of 0.5% through the end of 2014. Overall, real economic growth will remain severely constrained as long as bank lending is subdued and national governments focus on fiscal reforms. High rates of unemployment will continue to be a challenge, with the rate for the eurozone as a whole remaining just above 12% through 2014. Renewed debate over Greek or Portuguese debt sustainability, or unexpected political turmoil in Italy, could trigger another round of market volatility.

UNITED KINGDOM

Economic recovery continues in the United Kingdom, with real GDP growth headed for 1.3% this year and to as much as 2.0% in 2014. Inflation is slowly abating and should be close to 2.0% by the end of next year. The “forward guidance” policy being pursued by the Bank of England suggests that policy rates are unlikely to increase as long as the unemployment rate remains above 7.0%, which is likely after 2014.

JAPAN

Positive economic data continues to support Prime Minister Shinzo Abe’s vision of a Japanese resurgence. Real GDP growth is forecast to come in at 1.9% this year and fall to 1.7% in 2014 as fiscal stimulus offsets an expected drop in spending due to a consumption tax hike that takes effect next April. The Bank of Japan (BOJ) will very likely maintain the current 0.1% target policy rate, and it has stated its willingness to step up quantitative easing if the economy falters. The yen is expected to continue weakening moderately to 103¥/US$ by the end of 2013. The BOJ will miss its 2% inflation goal in 2013, with prices forecast to rise by 0.2%; however, the bank will hit the target next year as the consumption tax increase push prices up by 2.1%. Benign unemployment is expected to hover at 4%. Risks to Japan include global economic deterioration and a halt to implementation of fiscal and structural measures to complement monetary policy.

CHINA

China’s economy expanded at an annualized pace of 7.8% in the third quarter, prompting the government to declare that its 2013 growth target of 7.5% will be met and possibly exceeded. The government is emphasizing how this subdued rate of growth is to be expected from here forward as the economy moves away from investment spending and toward consumer-driven growth. The yuan has responded favorably, strengthening above CNY6.10/US$ and is expected to appreciate about 1.5% throughout this year and next. Reported inflation is expected to be met with specific policy-tightening measures rather than interest rate hikes, which are perceived as being potentially harmful to lending and the financial sector. The main concern going forward is the rising amount of investment spending supported by excessive and potentially unproductive lending.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

© Northern Trust