The Federal Reserve’s policies may remain easier for longer than previously thought

November 15, 2013

- The Federal Reserve’s policies may remain easier for longer than previously thought

- What’s the best way to arrest falling labor force participation?

- Look for the Fed to adopt a lower unemployment target

Here we are, still two weeks before Thanksgiving, and Christmas displays have been out for two weeks already. I know how important the season is to merchants, but isn’t it a little early to be focusing on December’s business?

That said, Asha and I have been focusing a lot on the December business of the Federal Open Market Committee (FOMC), whose next meeting is still more than a month away. It promises to be one of the most closely watched in some time, for a variety of reasons.

While the debate will be active, we think that the Fed could decide to become even more accommodative than it has been in the past. There are two main reasons we feel this way:

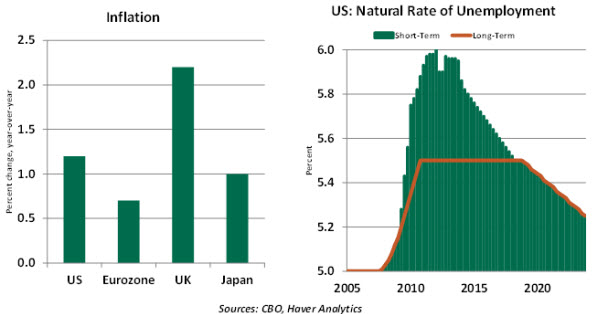

- The rapid deceleration of the price level places inflation well below the target of 2%. This is a global phenomenon, prompted by global overcapacity. Monetary policy must move back toward its objective for the price level.

- The United States clearly has quite a bit of cyclical unemployment, which will take a while to work off. But recent analysis from the Fed and the Congressional Budget Office reinforces the notion that 5.5% is still viewed as a long-term natural rate, and policy is likely to remain focused on achieving that outcome.

Following are specific discussions of labor market factors that are important to understanding the Federal Reserve’s perspective.

Participation Complication

My father was an electrical engineer. His inventions took a long time to develop, and doubt was often a prelude to success. Drawn from that experience, one of the life lessons he tried to teach me was to keep focused on goals, even when things aren’t going so well.

We lost Dad 12 years ago, but I still think about him often. His teaching came to mind recently as I was contemplating the Federal Reserve’s campaign to restore better hiring conditions. In my view, the Fed should persevere, even in the face of doubt.

Nearly six years after the Great Recession began, the labor market is still disappointing. To be sure, the current unemployment rate of 7.3% is down from a peak of 10%. Perhaps Americans should be thankful for the progress made, given the plight of European job-seekers. But joblessness has exceeded 7% for almost 60 months in a row. The only other time that’s happened in American history was during the Great Depression.

And a main contributor to the improvement in measured unemployment has been a significant exodus from the labor force. People who cease active job searches are no longer considered when the “headline” unemployment rate is measured. More than 11 million people have joined this category since the end of 2008.

Taken together, these developments have led some to suggest that the Federal Reserve’s program of quantitative easing has not been effective and should be curtailed. A review of some of the dynamics behind labor force participation, however, leads to a different conclusion.

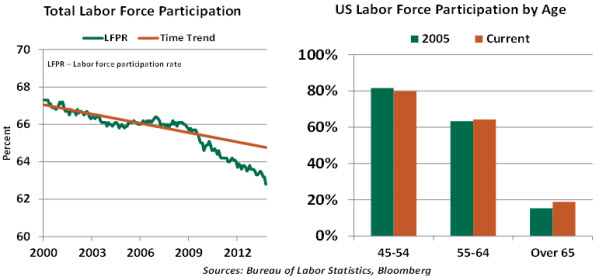

Some of the decline in labor force participation is due to the business cycle, but some is a reflection of longer-running themes. The chart on the left, below, separates the two by illustrating the declining time trend and the underage which has developed since 2008.

A review of some of the key themes follows.

- The retirement of the post-war baby boomers is moving people out of the labor force and will continue to do so in the coming decades. As shown in the right-hand chart above, participation rates for those older than age 65 are about a quarter of what they are for 50-year-olds. This is a natural life-cycle progression and not a result of sluggish economic growth. Former colleagues illustrated this trend carefully in a recent Chicago Fed Letter.

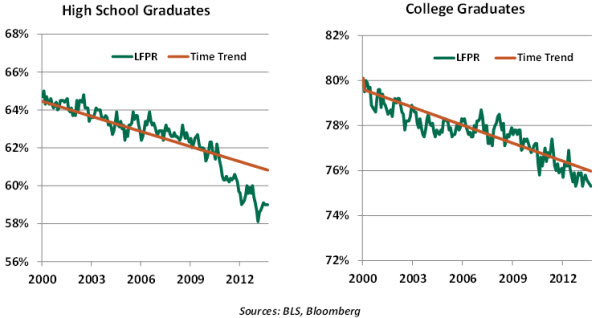

- Participation rates among workers younger than age 24 have fallen steadily for 15 years. There may be secular reasons for this: more young people pursuing more school for longer periods and devoting more time to their studies, for example.

However, this trend has accelerated since the recession, especially among workers younger than 20. It appears that roles traditionally accepted by those in their teens and early 20s are being taken by more experienced workers. This has a bit more of a cyclical quality to it.

- An additional 2.1 million Americans have entered the disability rolls since 2006. Skeptics wonder if the program has become an extension of unemployment benefits and note that workers accepting disability are extremely unlikely to return to work.

But studies have found that recent increases in disability are not out of line with history and evolving demographics. And other research has found little link between the expiration of unemployment benefits and the onset of disability payments.

- Workers with lower levels of education seem to be experiencing much higher levels of cyclical unemployment.

This development has led some to wonder whether there are skills mismatches that are making some workers structurally unemployable. Once again, though, studies of job losses and job creation do not find much of a sectoral mismatch. There is certainly an opportunity to use retraining as a tool to speed re-entry to the labor force; funds appropriated for this purpose may pay for themselves before too long.

Unfortunately, the likelihood is low that new investments in human capital can make it through the fiscal conservatism that has swept through Washington. It may certainly be that the Fed feels as if it needs to keep all of the stops out, given the dysfunction in Congress.

So in sum, the aging of the American labor force seems to be the only structural change that is affecting the aggregate participation rate. Policy should certainly not be aimed at pushing people who want to retire back into the labor force. But a significant deficiency of participation remains and needs to be addressed.

A recent paper by Federal Reserve researchers noted that cyclical unemployment can become structural if workers are out of the labor force for an extended period. Over time, however, the belief is that the displaced will once again become fit for hiring.

The depth of the 2008 recession and the financial crisis it was associated with have certainly increased the economy’s recovery time. Given the frustratingly slow pace of improvement in labor markets, it’s quite natural for doubts to arise about the efficacy of policy.

As my dad taught me, it’s always healthy to look at data and use it to question your strategy. But sometimes, these reflections will confirm your course of action. The weight of evidence suggests that the ultimate goal of 5.5% unemployment does not seem unreasonable. And so the Fed should keep the courage of its convictions and sustain its accommodation.

On Modifying Forward Guidance

The current status of the economy is such that the Fed is not in a position to switch from tapering of asset purchases to tightening of monetary policy. Following tapering, the FOMC will still face the problem of how to continue support for the economy through other monetary policy tools, given the elevated jobless rate and low inflationary environment. Forward guidance allows tinkering of monetary policy with words to support economic momentum in the transition from tapering to tightening.

A part of existing forward guidance consists of holding the federal funds rate at the current low level for an extended period until the unemployment rate touches 6.5%. At this threshold, the Fed would only deliberate about policy tightening and not necessarily tighten monetary policy.

The distance between the current unemployment rate (7.3%) and the unemployment threshold (6.5%) is closing, and the Fed has yet to see the degree of labor market improvement that it anticipates. The declining trend of the participation rate adds to the complexity of the situation.

Therefore, there is a strong likelihood for a modification of current forward guidance pertaining to the unemployment rate. In this context, Vice Chair Janet Yellen presented her version of optimal monetary policy strategy in a June 2012 speech. She defined this approach as one that minimizes the “social cost resulting from deviations of inflation from the Committee’s longer-run goal and from deviations of unemployment from its long-run normal rate.”

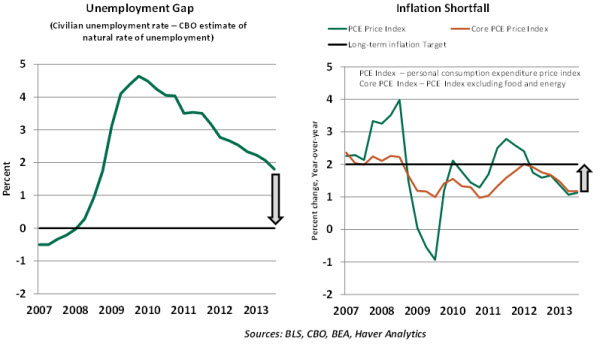

The charts above illustrate the Fed’s predicament. On the one hand, the civilian unemployment is nearly 2 percentage points above the natural rate of unemployment; on the other hand, inflation is running around 1.2%, significantly short of the 2.0% inflation target.

Monetary policy based on optimal control theory involves designing policy to reduce these gaps, bearing in mind that the cost of deviations must be minimized. The recalibration of monetary policy is the result of a sophisticated evaluation of policy outcomes.

In a recent paper, William English, head of the Fed’s Monetary Affairs Division, and his two co-authors extend Yellen’s optimal control policy framework to identify how monetary policy can be fine-tuned to deliver the best policy outcome.

These authors conducted simulations of a simplified Fed model with varying inflation and unemployment thresholds and assessed the policy outcomes. Their study concludes that lowering the threshold to 5.5% would more successfully satisfy the Fed’s dual mandate of full employment and price stability than the current 6.5% threshold.

They also note that the net benefit from lowering the unemployment threshold is greater than raising the inflation threshold. Admittedly, the study includes assumptions, and implicitly the unemployment rate is seen to be a longer distance from the Fed’s goal compared with the inflation target. The results of this study are a direct monetary policy recommendation, with caveats.

The minutes of the July 2013 FOMC meeting include a discussion about a lower threshold for unemployment and suggest that lowering it is within the realm of possibilities.

“… several participants were willing to contemplate lowering the unemployment threshold if additional accommodation were to become necessary or if the Committee wanted to adjust the mix of policy tools used to provide the appropriate level of accommodation.”

In terms of policy choices in the near term, there is concern within the Fed about the efficacy of asset purchases, and the FOMC is hard-pressed to have another tool at hand to provide accommodation as it approaches the current threshold. Strengthening forward guidance with a lower unemployment threshold is a suitable option on the road to normalizing monetary policy.

The current global disinflationary environment enhances the case for a move to a lower unemployment threshold. For all these reasons, a lower unemployment threshold looks increasingly likely.

© Northern Trust