- The world needs to do more to stimulate spending

- Moderate gains are seen for U.S. holiday sales

- The Federal Reserve may change its policy mix

I don’t know why, but controversial topics often come up at my Thanksgiving table. At a time when we are supposed to be celebrating food, fellowship and family, someone always seems to steer the conversation to climate change, college costs or Congress. In that event, I try to fill everyone’s mouths with mashed potatoes as quickly as I can.

Last year, we got a modest break from that ignominious tradition. My guests got onto the topic of holiday shopping, moving from theory to practice by taking out their smart phones and initiating transactions. I’m not sure all of that commerce was in keeping with the Thanksgiving spirit, but I was thankful not to have my guests throwing dinner rolls at one another.

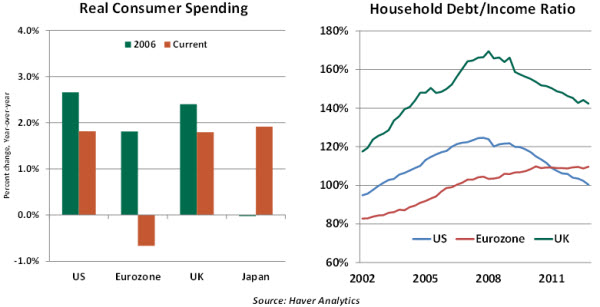

The attention paid to consumer spending is especially acute as the holidays approach, but it has become a year-round and global focus. One of the reasons that international economic growth remains subpar is relatively weak consumption.

Spending by American and British households is expanding at a pace far below pre-crisis standards, and real personal consumption in Europe continues to decline. Only Japan, which is emerging from a long spending malaise, is showing noticeable improvement.

The reasons for this are not hard to identify. Unemployment remains elevated in most developed countries, and income growth has been slow. Deleveraging has been an imperative for households, and consumer credit has been harder to come by in many places.

While equity market recovery has boosted wealth, the distribution of that wealth has not been terribly even. In many quarters, there remains a need to rebuild net worth to compensate for crisis-era losses. Retirement looms for the postwar generation, and being financially prepared will require greater contributions of annual saving. So frugality may linger, even as debt levels in the United States and the United Kingdom move back toward pre-crisis levels.

The sluggish spending habits of households in the developed world have reverberated in emerging markets, whose progress has been achieved largely through the export of goods. Annual merchandise export gains for China, Brazil, and India have fallen from the 30% range in 2011 to less than 10% today.

So a key for policy-makers is finding or creating pockets of consumers who are still in a good position to spend. One means of doing this is to pursue a weakening of one’s currency, hoping domestic goods win global market share. Many countries have stated this aim, but except for Japan, their efforts have really not been that successful over the past 12 months.

The search for demand then alights on countries that should be in a good position to spend more but are not doing so. There are two primary candidates.

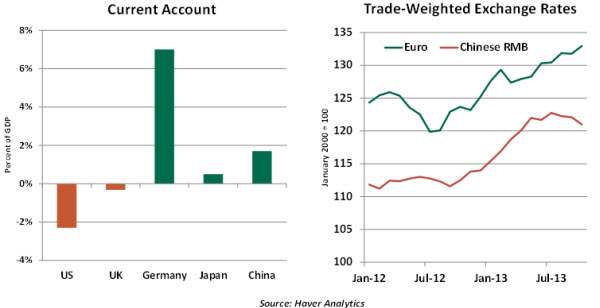

- Germany has received a lot of criticism for its emphasis on pushing exports instead of stimulating its consumer sector. Germany’s current account surplus (the excess of exports over imports) rose to more than 7% of gross domestic product (GDP) in the first half of this year. In nominal terms, Germany’s surplus is larger than China’s.

By contrast, real consumption has grown only about 1% over the past 12 months in Germany, despite the lowest unemployment rate in the eurozone (5.3%) and solid gains in wages. Germany’s household debt-to-income ratio is only about 75%, well below levels seen in the United States, Britain and elsewhere in Europe. And the German federal budget is essentially in balance, potentially offering room for stimulus.

Yet the monetary and fiscal tone coming from Berlin is anything but stimulative. German representatives were not pleased with the recent decision by the European Central Bank (ECB) to lower interest rates and have pushed austerity over growth as the path to long-term prosperity. The euro has been a strong currency over the past year, preventing peripheral countries from improving their exports.

Further, the Germans would be unlikely to allow the ECB to venture into quantitative easing, a step many feel must ultimately be considered to avoid a prolonged European malaise.

Last month, the U.S. Treasury Department criticized German policy in its “Report to Congress on International Economic and Exchange Rate Policies.” Calling for stronger demand growth, the report suggested that German strategy is inhibiting the ability of other countries to achieve a better equilibrium. The International Monetary Fund and the European Commission quickly agreed.

- Household spending in China has been growing rapidly at a recent pace of about 9% annually. But this is from a very modest base; Chinese consumption is only 36% of GDP, a little more than half the level seen in the United States.

There are certainly cultural underpinnings for this, namely the responsibility borne by Chinese families for elder care. The country’s one-child policy has created a demographic imbalance that makes this a particularly costly obligation.

The Chinese have pursued an export-led growth model for the past generation, and they manage their currency accordingly. Even though the Chinese renminbi has strengthened over the past year, many analysts think it would be stronger still if allowed to float freely. The recently concluded plenary session of the Chinese central committee touched on rebalancing the composition of growth, but any change is expected to be gradual.

In sum, then, we have too much supply and not enough demand in the world today. This is one reason why growth has been slow and why inflation has been falling in developed nations. Finding a path to better consumption levels will be a key challenge for 2014; those countries in the best position to lead this effort must step forward.

In the meantime, we can all do our parts by being generous this holiday season. But please: wait until after Thanksgiving dinner to do so.

Checking the Pulse of the U.S. Consumer

As the holiday season draws closer, one wonders if American consumers will go on a spending spree. Real consumer spending has advanced at a tepid 1.9% pace in the first three quarters of the year. Tracking the usual drivers of consumer spending, such as employment, income, wealth and credit trends, offers hints about the likely nature of holiday sales.

Hiring has improved in the last three months, but the number of people working part time and those unable to find jobs for more than six months are each holding at worrisome levels, despite 17 quarters of economic growth. As a result, real disposable income grew 1.6% from a year ago in the third quarter, representing a small improvement from the first half of the year but remaining significantly below trend.

On the bright side, the upward trend of equity and home prices has lifted the net worth of households, which should be supportive of spending. But the gains in wealth have been significantly uneven in this recovery. The Pew Center notes that 7% of the population experienced a 30% increase in wealth, while the net worth of the remaining 93% declined 4% in the two years ended 2011.

These numbers indicate that high-end retailers may benefit more in this holiday season than others. Anecdotal information indicates that major retailers such as Walmart and Gap announced discounts a month earlier than typical, implying holiday sales could cluster in November.

It is noteworthy that the mix of household purchases is skewed toward durable goods such as cars, furniture and other such items, while purchases of clothes and toys have taken second place. This pattern may continue to prevail in the holiday season.

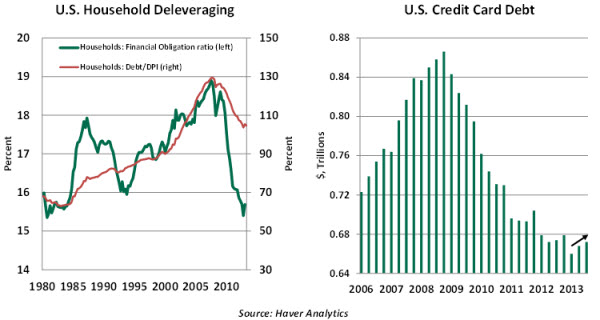

An increase in outstanding credit card debt over the last three quarters points to willingness of households to resume shopping with credit cards. Also, bankers have somewhat eased lending standards for households. Lower gasoline prices should ease budget pressures. Each of these trends augurs positively for consumer spending.

Consumer sentiment measures dipped in recent surveys. The partial government shutdown most likely played a role, and surveys in the weeks ahead should show an improvement.

All things considered, the main factors governing consumer spending point to a moderate gain in consumer spending this holiday season. But results may be somewhat uneven and for some retailers, unsatisfying.

Fed Weighs Options to Temper Tapering Impact

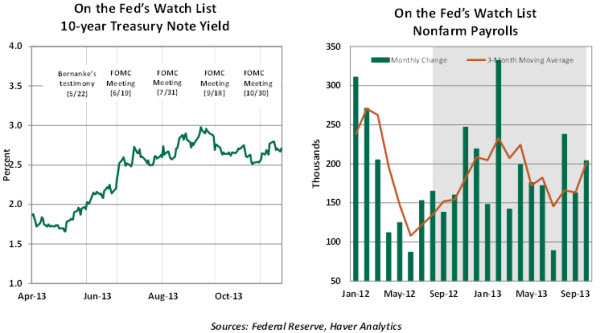

The most important takeaway from the minutes of the October Federal Open Market Committee (FOMC) meeting is that the committee remains keenly interested in reducing asset purchases from the current pace of $85 billion each month.

The Fed’s intent to taper is reinforced by the fact that the discussion included scenarios where it could scale back asset purchases before the underlying strength of economic activity is confirmed. The minutes note that under such circumstances it would engage in alternative actions that could offset the effects of reduced asset purchases.

One way to do this would be to modify forward guidance, the indication of how policy is likely to evolve in the future. The Fed’s pledge to keep short-term rates near zero until unemployment falls to 6.5% is the current expression of this tactic.

The FOMC discussed different forward guidance options in October. The degree of support for each option varied, as did the respective shortcomings that were noted. Changes to forward guidance could involve a lower unemployment threshold or a lower bound for inflation.

Whatever course is ultimately selected, one hopes that it is communicated clearly to the markets. In order to engineer a smooth transition of long-term rates back to normal levels, investors need to have a better picture of how the Fed will manage its huge portfolio of bonds. So far this year, the Fed has been less than successful in this endeavor.

The November employment numbers and the state of fiscal uncertainty will be front and center in deliberations at the December meeting. We are not convinced that a December announcement for tapering carries a strong probability, partly because Congressional decisions will remain unknown until the 11th hour. It also is unlikely that a single jobs report will make a substantial difference in the Fed’s forecast of employment conditions.

Navigating with forward guidance will be a challenge, particularly in an economy Fed Chairman Ben Bernanke called “fragile.” Therefore, the Fed is likely to err on the side of caution.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

© Northern Trust