- The U.S. employment report puts taper onto the table

- Don't expect further rate cuts from the ECB or the Fed

- Auto sales have been a bright spot amid sluggish consumer spending

Today’s strong U.S. job report will likely prompt the Federal Reserve to taper its quantitative easing program later this month. We’ll have more complete analysis of the Fed’s December meeting for you next week, but we’re guessing that better labor market conditions and an imminent deal on the U.S. Federal budget will support a modest reduction in asset purchases.

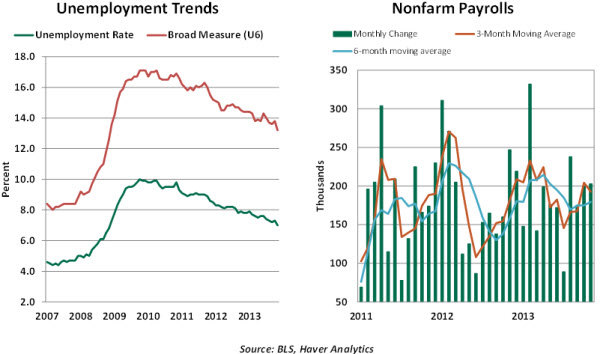

The unemployment rate declined to 7.0% in November from 7.3% in the prior month. Payroll employment advanced 203,000 in November, following a revised gain of 200,000 in October. These numbers are impressive, as are the details.

The noticeable drop of the jobless rate was partly due to the return of furloughed government workers after the partial federal government shutdown in October. In the household survey, employment advanced 818,000, following a 735,000 drop in October.

The November payroll numbers put the three- and six-month moving averages at 193,000 and 180,000, respectively. If hiring proceeds at the 193,000 pace seen in the last three months, then payrolls would match the peak of January 2008 in roughly seven months.

In November, factory employment moved up 27,000, and construction jobs rose 17,000. Private sector hiring increased 196,000, and government employment rose 7,000. In the service sector, retail hiring rose 22,000, education health care jobs increased 40,000, and business services employment rose 35,000.

The average workweek increased one-tenth to 34.5 hours, while hourly earnings shot up 0.2%, taking the year-to-year gain to 2.0%. The payroll and earnings numbers point to a moderate increase in personal income in November. The 0.4% jump in the manufacturing man-hours index suggests a strong increase in factory production during November.

Without doubt, the November employment report calls for examining both the timing of tapering and the current forward guidance of monetary policy. The minutes of the October Federal Open Market Committee (FOMC) meeting drive home the point that the Fed is ready to taper asset purchases, if economic data offer the necessary justification.

To be sure, there is still room for improvement. The November participation rate (63%) erased the October decline, but it is below the September reading of 63.2% and close to the cycle low. The participation rate has dropped 0.6 percentage points since the third round of quantitative easing (QE) was announced, and the unemployment rate has declined 0.8 percentage points. Also, long-term unemployment (unemployed for more than 27 weeks) inched upward in November (37.3% versus 36.1% in October).

Fed rhetoric suggests that a discussion of tightening monetary policy would start at a 6.5% jobless rate. Given the downward drift in the participation rate, we might see a lowering of this level. Such a modification of the forward guidance could also occur at the December 17-18 FOMC meeting.

The discussions there will certainly be intricate, with a lot to consider. But the Fed is getting what it has been wishing for, and that’s not a bad thing.

Too Much Negative Talk

As a practitioner of the dismal science, and a risk manager to boot, I am often accused of being overly negative. An economist, after all, is someone who can find the dark cloud behind any silver lining.

Some monetary authorities have also been thinking negatively recently as they contemplate reductions to interest rates. Some are even thinking about pushing past the zero lower bound. In Europe, the possibility that that member banks might be charged for leaving funds on deposit with their central bank has generated a great deal of discussion and, in some quarters, consternation.

We do not think that moving official interest rates down or into negative territory would be effective in promoting economic objectives. Harmful unintended consequences could easily arise. While every alternative deserves exploration during challenging times, we expect central banks to look elsewhere in their search for new ways to promote growth.

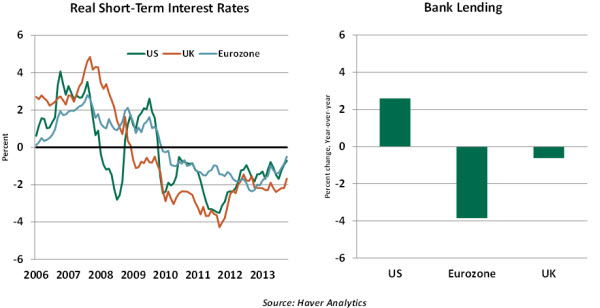

Since 2008, short-term interest rates in the United States, Great Britain and continental Europe have been reduced about as far as they can go. When inflation is factored in, real interest rates have been in negative territory for quite some time in these markets. Yet despite the allure of higher loan yields, credit growth remains suboptimal.

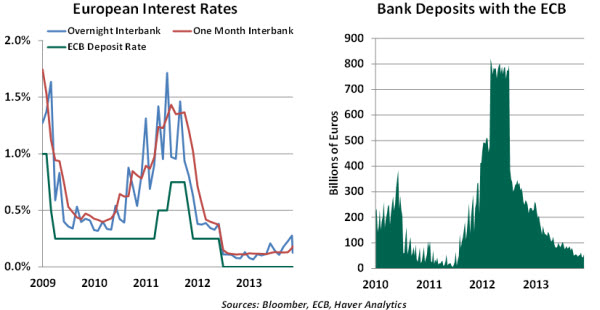

This leaves some to wonder whether lower interest rates on reserves might prompt financial institutions to lend more. In the case of Europe, where the rate paid on deposits with the central bank is already zero, this would require moving interest rates into negative territory.

The European Central Bank (ECB) would not be the first central bank to take this step. Both Switzerland and Denmark have negative deposit rates at the moment, and others have had them at times in the past. In many of these cases, however, rates were pushed below zero to limit unwanted deposit inflows that were swelling bank balance sheets and creating unwanted strength in local currencies.

The ECB is far larger than the central banks in Switzerland and Denmark and has the complication of setting monetary policy for a set of countries whose economic fortunes have diverged considerably in the past five years. So there really is very little history to guide an assessment of what might happen in Europe if the ECB pushes rates below zero.

An initial worry about the efficacy of this strategy involves technology. There may be systems still in operation that won’t easily accommodate a negative sign in an interest rate field. ECB President Mario Draghi has insisted that this will not be a constraint, but the readiness of back offices is a source of mild uncertainty.

A second concern is how the movement in official rates would ripple through to other markets. Financial companies might react to the drop in the rates they earn by offering sub-zero rates to depositors. Proponents of the strategy might hope that this would prompt more spending and less saving. But faced with having to pay banks to safeguard their money, some depositors may choose to hold currency or hard assets (like precious metals) instead. This would have the effect of reducing the liquidity in the banking system and potentially impeding the flow of credit.

Interbank lending rates are tied closely to central bank benchmarks. If the ECB were to establish a negative deposit rate, indexes like the London Interbank Offered Rate (LIBOR) would be under downward pressure. This would reduce the yield on bank assets (many loans are tied to LIBOR) and place additional stress on bank earnings.

Further, you could see a diminished supply of wholesale funding available in this scenario, as those lending in the short-term money markets seek acceptable yields. Negative rates on repurchase agreements (repos) could lead potential borrowers of securities to withdraw from the market. Given the reliance of some institutions on these sources, the potential disruption could be significant.

A final question about the negative rate is whether it would prompt very much additional lending. In the United States, the Federal Reserve has had only fleeting conversations about lowering the rate it pays on excess reserves. Modest lending growth in the United States is largely the result of slack credit demand; banks have all the incentive they need to lend more, given that excess reserves yield only 25 basis points. So the Fed has refrained from further reductions in this compensation.

In Europe, the dynamic has been somewhat different. There is demand for additional credit, but much of it is coming from peripheral countries where banks are troubled and borrowing rates are high. Banks in the northern part of the continent are healthier and have reserves to lend but have been reluctant to expand their exposure to southern states.

A negative deposit rate would certainly incent a reallocation toward lending, but levels of excess reserves in Europe are very modest at the moment. With capital requirements rising and an asset quality review on the horizon, European banks have been very conservative about adding credit risk. And with the financial situation in peripheral countries still very fluid, it is not clear that 25 or 50 basis points of additional incentive would be enough to tip the scales.

In sum, the risks certainly seem to outweigh the rewards of negative rates for major central banks. It might be better for them to accentuate the positives of other measures.

Autos Sales Drive Ahead

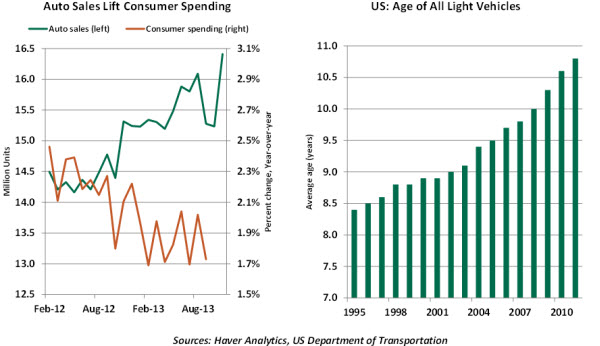

Consumer spending in 2013 could possibly stand out as the slowest in the last four years, barring exceptional strength in the fourth quarter. But buried in the tepid trend of consumer spending is strong growth of auto sales. Auto sales shot up to 16.4 million units in November, which puts the year-to-date average at 15.6 million units.

U.S. auto sales bottomed at 10.4 million vehicles in 2009. They advanced in each of the next four years and should close 2013 with the best tally since 2007. The forward momentum of world auto sales this year has also been a big plus for auto industry.

Aggressive incentives to promote sales in November are only one part of the auto sales story. Auto sales have performed significantly better than overall consumer spending because consumers are able to obtain car loans with relative ease. The underlying collateral held its value very well during the financial crisis, and auto lenders are not enduring the broad re-regulation and restricting experienced by their counterparts in the mortgage business.

Attractive auto loan rates (about 4.5% for a 4-year loan), which are close to the historical low of 4.13%, remain supportive of the upward trend of auto sales.

Also, the average age of a motor vehicle on the road is close to 11 years, a far cry from the situation a decade ago. Replacement demand is a big factor driving auto sales at the present time. If employment conditions improve in the months ahead, today’s rosy sales trend could even gain momentum.

The strength in auto sales has translated to a pickup in auto sector employment in the first two months of the fourth quarter after a deceleration in hiring during the third quarter. The spillover effects of strong auto sales should be visible in spending and employment, if the current sales trend is maintained.

Given where automakers and auto sales were during the depth of the financial crisis, the current renaissance has been very impressive. And there may be even better times ahead.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

© Northern Trust