FOMC Preview: Less quantitative easing and more forward guidance

December 13, 2013

- FOMC Preview: Less quantitative easing and more forward guidance

David Stockman, budget director under President Reagan, was in town this week. Stockman was a hero of mine in the early 1980s for daring to challenge the notion that federal budget deficits don’t matter. His recent work, “The Great Deformation: The Corruption of Capitalism in America,” extends that cynicism by presenting an outlook that is a long way from the “morning-in-America” optimism of his former boss. “I am not drinking the Kool-Aid,” he told us. After listening to him, I considered switching to vodka myself.

Stockman spared no one in his economic critique, with Congress and the Federal Reserve singled out for particular excoriation. While I find his perspective a bit too dark for my taste, I do concur with his suggestion that the Federal Reserve should find a way out of quantitative easing (QE) soon. And I think the Fed will take the first step in that direction at its December 17 - 18 Federal Open Market Committee (FOMC) meeting. Here are the arguments for and against reducing quantitative easing that the discussions will feature.

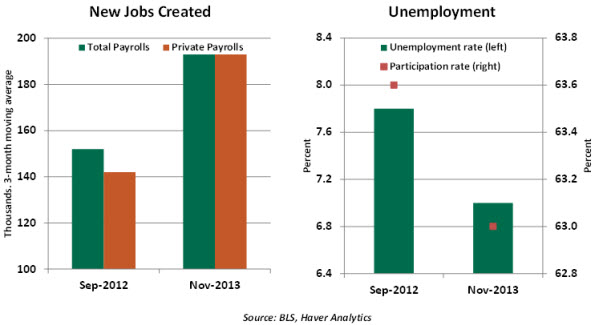

Cautious types will certainly observe that the unemployment rate might be understated because so many people have become discouraged and ceased looking for work. And it is always wise to avoid placing too much weight on recent payroll readings. But it may also be true that employment in the household survey could be understating job creation among very new businesses. And Fed Chairman Ben Bernanke expressed an expectation in June that asset purchases would be concluded when unemployment reached 7%.

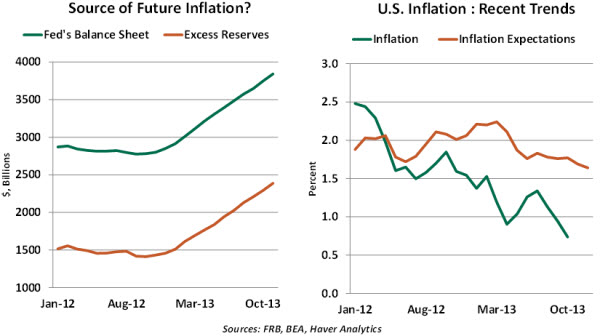

It has certainly been surprising how muted inflation has been over the past two years. If the trend in the right-hand panel continues much longer, we could see damaging deflation set in. To stay focused on this, we expect the Fed to extend the period over which short-term rates will remain near zero by lowering the unemployment threshold that would trigger a rate increase. This application of forward guidance would allow for some reductions in asset purchases.

The fiscal accord reached this week is a welcome change from the near-disaster of October. Government has been funded through next year, and we doubt that debate over the debt ceiling will be as contentious in an election year as it was a couple of months ago. The Fed had cited uncertainty over the U.S. federal budget as a reason not to taper in September; from this perspective, at least, the coast is clear.

Policy uncertainty has hindered economic performance this year. If the Fed can bring a bit more clarity to the future of monetary strategy with its words and deeds next week, the clouds that have limited the vision of business people and investors could lift.

Several other factors lead us to favor a first step toward tapering next week as opposed to the first quarter of next year:

- Markets now seem well-prepared for a reduction in quantitative easing, a contrast to the shock that emerged when tapering was first suggested last May. Equity markets scaled new heights after the strong November employment release, and Treasury bond yields are holding below the highs reached prior to the September FOMC meeting.

- The December meeting will be followed with a press conference, while subsequent meetings may not. Such an important change in policy direction will require some careful explanation, especially since long-term investors will be focused less on the first step and more on what the full path looks like from there.

- In our view, Chairman Bernanke would like to have the long process of policy normalization underway before he departs next month. He may have a limited role at the January meeting, as Janet Yellen is likely to be confirmed as his successor then.

We expect the Fed will announce a reduction of $10 billion to $15 billion in asset purchases next Wednesday. A target of 6% unemployment (down from 6.5%) will become the new benchmark for beginning contemplation of higher short-term rates. The Fed will also publish a new set of economic forecasts that will attract careful review.

David Stockman may be right: we are still at risk of an unpleasant outcome in the long term. But we’re a lot better off than we were five years ago, and we have our central bank to thank for that. It will be tricky to get the Fed out of the economy, but that isn’t to suggest that it shouldn’t have entered in the first place. Next week should be the start of a long good-bye.

© Northern Trust