In 2003, we first launched our Matthews Asia Growth strategy to U.S. investors. Today, we celebrate not only a decade of investment in Asia via this strategy, but also the region’s remarkable growth and evolution during this period. Many of its economies are now fundamentally stronger and consumption has been on the rise, laying the foundation for Asia’s prosperity.

As with any 10-year period, the decade saw varying economic cycles and developments, including the rise of China and India as well as significant market corrections triggered by the 2008 Global Financial Crisis and subsequent rallies in 2009. Asia has evolved from being considered an “interesting but obscure” part of the world to the frontline asset class for global equity investment.

Just over a decade ago, consumerism throughout much of Asia was a far cry from what it has developed into today. While many Asian economies have been well-suited to be good manufacturing and production hubs for foreign multinational corporations, this did not immediately translate into higher GDP per capita. In the late 1990s and early 2000s, few Asian countries had reached the US$5,000 mark for GDP per capita—considered a tipping point for consumption growth. Only the “Asian Tigers” of Hong Kong, South Korea, Taiwan and Singapore had managed that feat, and it was no coincidence that they were also the focus of investment in Asia back then.

In 2003, GDP per capita for China was about US$3,200 (in PPP or purchasing power parity terms), and that of India was approximately US$1,800. A comparison of the MSCI All Country Asia ex Japan Index against other indices such as MSCI EAFE (Europe, Australasia and Far East) or MSCI Global, in the late 1990s showed Asia to generally be an inferior investment destination. Still undeveloped capital markets, corruption, weak political systems and slow economic growth were some of the main factors that hampered many countries in the region. However, rising incomes led to a growing middle class and higher consumption levels. By 2013, India’s per capita GDP reached US$4,000, and in China the figure more than tripled its 2003 level, reaching about US$9,800.

In considering Asia’s milestones, let us focus on the following three points:

Where are we now in terms of growth trajectory? Why should we still be excited about growth perspective in Asia?

How should one invest in Asia?

How should investors think about Japan in the context of Asia?

The Sweet Spot

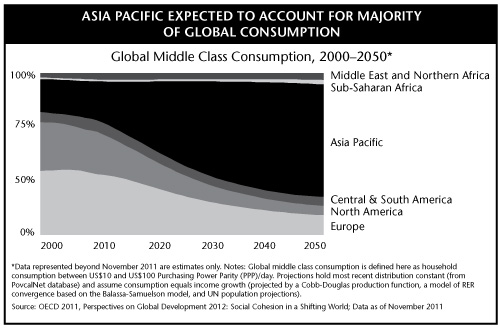

Asia’s evolution in the last 10 years has been quite remarkable. Asia ex-Japan’s nominal GDP per capita increased from US$1,560 to US$5,044, up 223% from 2003 to 2012. However, during the previous 10 years its increase was just 62%, from US$866 to US$1,400. But where are we now after the brisk growth of the past decade?

On the surface, the “real” growth rate across Asia appears to be slowing to 4% to 5% at the moment. However, I suspect that this is just the beginning of a vast consumption growth story. The greatest acceleration has historically happened at a GDP per capita level of US$5,000 to US$15,000 and many Asian economies have now reached this “sweet spot.” These countries have now reached the level of economic growth comparable to Japan in the period between 1960 and 1980, when its consumption blossomed.

And the driver of domestic consumption is rapid wage growth: Japanese consumers in the 1960s continued to upgrade their consumer “wish list” as their wages climbed by double digits every year. With the exception of developed Asia, wages today in many Asian countries are also rising by double digits. This is a good reason to get excited about the future of Asian consumers.

How to Invest in Asia?

While investors may receive general exposure to Asia’s overall development via index funds, such funds tend not to capture the growth of firms benefiting from the rise of middle class consumers—a key focus of us at Matthews. We believe in the benefits of a more concentrated actively managed portfolio. Higher concentration means that we are quite selective in our approach. In my opinion, selection and focus are critical in gaining meaningful exposure to Asia’s rising middle class.

Over the last decade, Japan has been one of the most problematic parts of Asia. But toward the end of 2006, its equity markets managed to keep up somewhat with the rest of the world before fading again from the global investment map as the yen continued rising against the U.S. dollar between 2007 and 2012. However, beneath the surface, Japanese corporates made significant adjustments, cutting costs to bare bones and boosting revenue and profits by expanding to regional Asia markets.

It is important to note that this was not possible 20 years ago when consumer markets in Asia were still too small for Japanese firms to tap for its exports and services. Not only has this become a viable option for Japan but in many cases, Asia’s regional markets are more profitable for Japanese firms than its own domestic market. Asia’s rising middle class population is a very positive development for Japanese corporations.

We are frequently on the ground in Asia, mining the region for the most attractive growth opportunities across developed, emerging and frontier Asia markets. And we believe that some of the most exciting opportunities could be uncovered in countries, such as Myanmar and Cambodia, that tend not to make financial headlines quite as often as China and India. My approach is to keep my eyes wide open in search of the next investment idea from any corner of the region. This is why I spend so much time on the ground exploring opportunities. I am increasingly optimistic about the region’s future, and believe the next decade will be even more exciting than the last.

Taizo Ishida

Portfolio Manager

Matthews Asia

Reflections on Growth 1990s Style

While the past decade has seen dramatic changes throughout Asia, its evolution is even more astounding when we consider the roots of its development over the past quarter century.

Matthews Asia has in the past often been mistaken for value investors due to our relatively deep company research and low portfolio turnover. But we considered ourselves fundamentally driven growth investors. By the time we launched the Asia Growth strategy in 2003, the breadth and depth of the markets had expanded dramatically. The ability to apply multiple investment disciplines within the Asia markets is an established fact. And whichever yard stick is applied, the challenge of investing in the growth region of the world remains exciting.

The creation of the Asia Growth strategy, which I had the pleasure to lead at its launch, marked our first full asset class vehicle. Growth remains a primary driver in our thinking at Matthews. And our belief in both the future of Asia and the potential of its multitude of publicly listed companies remains undiminished as the region moves into a new era. Twenty five years ago there were some little known markets in which few investors dared to tread. Hong Kong, South Korea, Taiwan and Singapore had been dubbed the Four Tigers in the mid-1980s and “emerging markets” became a new investment concept. Back then, Japan utterly dominated Asia’s investment landscape and the Tigers, along with Malaysia and Thailand, were an afterthought for most experienced regional investors.

But Japan had clearly matured in the previous decade and was trading at astronomical valuations. So a few people, including Matthews Asia founder Paul Matthews, chose to focus on the new Asian “miracle” economies. My first Asian investment mentor used to describe this as, “investing in growth companies in the growth part of the world.” The word “growth” was a constant in every presentation.

Growth was invariably described by GDP or trade statistics that were generally very impressive. The vast majority of professional investors were “top down,” choosing the best looking economies and investing in the few blue-chip companies available at the time to foreign investors. Some struggled with Asia’s general lack of transparency, poor accounting and short corporate histories. And some markets, like South Korea, had strict limitations on foreign ownership. Asking which country you were “overweight” in and why was about as far as most fund analysis went.

In the 1990s, my issue with “value” was that, given the poor regulatory environment back then, one was highly dependent on the integrity of company management and its treatment of minority shareholders. Investing in the “value” side of the markets often meant investing with the most dubious management teams. We watched many U.S. firms that tried to set up in Asia in those years fall afoul of a great value investment that was undone by duplicitous or incompetent management—the type of management we were willing to pay a premium to avoid.

To offer some context and historical perspective, when Thailand’s currency collapsed in the summer of 1997 and the Asian Financial Crisis began (still fondly called the IMF Crisis by many in Asia), our bottom-up or company-driven growth style was put to the test. Because we believed in company visits as a key part of research, our contact with senior managers was a critical source of information. While the general economies were doing horribly, individual companies that had seasoned management were often handling the crisis reasonably well and even benefiting from the elimination of low-quality competition. Our confidence in the management teams underpinned our commitment to remaining fully invested and not looking for ways to remove risk from the portfolios. Many of our competitors were holding large cash positions in the belief that they could get back in the markets when the worst was over. We had no such confidence in our ability to time markets.

When the markets finally turned in August 1998, the rally was explosive. Markets were often led by companies with both good growth potential and respected management teams—the kind of companies in which we were always interested. Many investors were convinced that this was a “dead cat bounce,” meaning just a brief recovery. By the time the recovery was visible in the economic statistics, many companies had doubled or tripled in price. We had become utterly convinced that the key to our investment style was our focus on companies, without leaving behind a keen understanding of each country’s unique social, political and economic environment. Companies live in an ecosystem that must be well understood, but in the final analysis, it was selection of companies that became the foundation of our process at the end of a fascinating decade of growth and volatility.

Some investors today are understandably concerned by the issues of the moment, such as the current tensions between Japan and China. But many of us at Matthews have spent our careers tracking Asia’s rise and know that managing portfolios based on the political posturing of the day is a sure way to miss the opportunity to participate in the region’s rise.

While there are several markets in Asia that straddle the line between developed and developing, many growth opportunities exist—most obviously in economies that are considered frontier and emerging. We will continue to adhere to our philosophy of bottom-up investing that has been tested over 20 years, and offer investors unique strategies for investing in these dynamic markets.

Mark W. Headley

Chairman

Matthews Asia

The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. Matthews International Capital Management, LLC does not accept any liability for losses either direct or consequential caused by the use of this information.

© Matthews Asia