The Year in Review

December 20, 2013

The end of the year is a time of reflection. The spirit of the holidays invites us to turn inward and renew our commitment to family, friends and community. We hope that the warmth drawn from these associations makes this a special season for all of you.

On an earthier note, inward reflection is also occurring in the workplace, as performance reviews at many companies take place at this time of year. As we contemplated our experience in 2013, a highlight was the opportunity to provide more than 150 presentations in 12 countries on four continents. We have really enjoyed meeting with so many of you and sharing a series of terrific conversations.

We’ve had no shortage of issues to discuss. As this will be our last weekly of the year, we thought we would offer some parting reflections on the year just past.

Following are the things we liked most about 2013:

- The class with which Ben Bernanke handled himself amid a poorly handled succession plan. We wish him great thanks for what he did for us all and success in the next chapter.

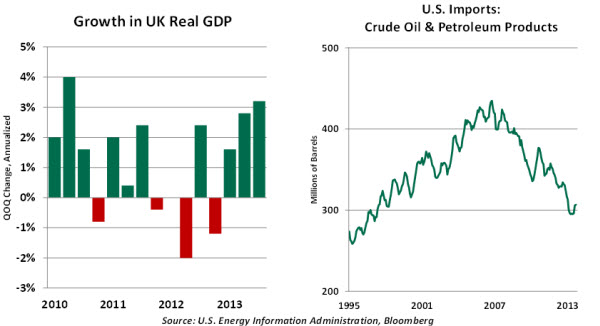

- The surprising pick-up in U.K. economic growth. Mr. Carney’s unofficial unemployment target is within reach, and the Bank of England could join the Federal Reserve next year in beginning a long exit from accommodation.

- The continuing decline in U.S. oil imports, which are now at 15-year lows. America has gone from seemingly intractable reliance on foreign petroleum to the prospect of self-sufficiency in less than a generation. Hard to believe.

- The dumplings in Beijing, salume in San Francisco, ma po tofu in Hong Kong, paella in Melbourne, venison in Stockholm, curry in Singapore, and grouper in Florida. Thanks to all of the partners who hosted (and fed) us so well.

- The stoic resilience of the Irish as they worked through their economic restructuring and made preparations for exiting their EU support program next year.

- The continuing resurgence of the U.S. auto industry.

- Shinzo Abe finally trying something different in Japan. He seems to understand that the definition of insanity is doing the same thing repeatedly and somehow expecting a different outcome.

- The improving state of the U.S. states, where hiring and spending have finally started to expand. Now if they could all just fix their pension systems….

- The (hopefully) ultimate exit of Silvio Berlusconi from public life.

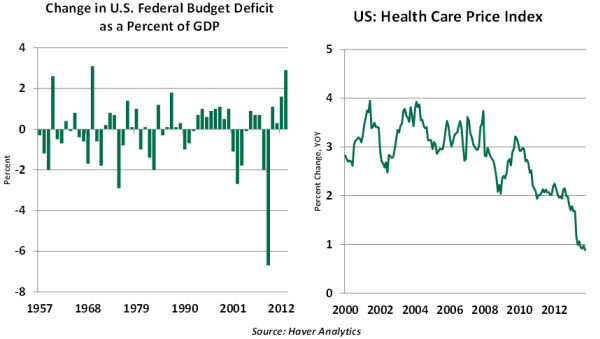

- The U.S. Congress quietly reaching a budget accord at the end of the year, after a noisy government shutdown in October. Whether by luck or design, 2013 saw the biggest one-year drop in the budget deficit as a percentage of gross domestic product (GDP) in more than 40 years. As that headwind diminishes, U.S. growth should gain.

- The moderation in U.S. health care inflation. If recent trends persist, the country’s long-term fiscal position may be much more manageable than people think.

Following are the things we liked least about 2013:

- Central bank communication, forward guidance in particular. Monetary authorities are still looking for the right way to say the right things to the markets. And they are still trying to find the optimal number of voices to express these thoughts.

- The growing Chinese property bubble and the willingness of many to explain it away.

- The hype about the re-shoring of manufacturing to the United States because of low energy costs. Simply not in the data at the moment.

- The handling of the Cyprus banking crisis and slow movement toward banking union in Europe. Until credit flows more freely ¬– and across more national borders – Europe’s recovery may remain constrained. And Europe’s politics may get more complicated.

- The continuing shrinkage of personal space on airplanes. The middle seat, next to a babe in arms with a raging cold, is no fun at all.

- The near U.S. default amid a fight over the debt ceiling. Completely unnecessary, and internationally embarrassing. Here’s hoping that we don’t have a re-run next spring.

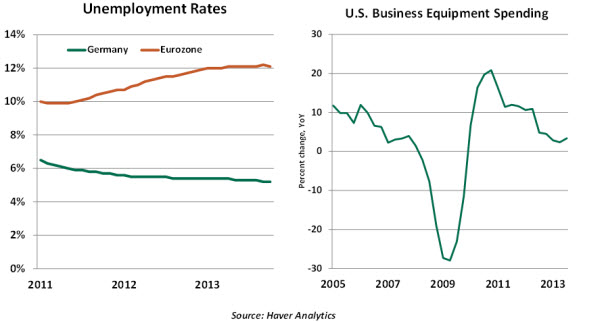

- The continued rise in unemployment across most of Europe, and the deeper fragmentation of performance between North and South.

- The frustratingly slow pace of U.S. business investment. We won’t get decent growth or productivity without it.

- Detroit, Puerto Rico and a handful of others casting an undeserved dark shadow over other issuers of municipal debt.

- The aborted candidacy of Larry Summers for U.S. Fed chairman. You just don’t campaign for a job like that, and vetting should be done outside the media’s glare. Fortunately, the process ended in the right place.

- Brazil’s and India’s struggles. It’s great when foreign capital is flowing in, but you must remember that the distance between the front door and the back door is not that great.

Our global economic outlook for 2014 will be in your hands in early January. We’re actually becoming much more upbeat about economic prospects in the quarters ahead. We’ll look forward to serving you and sharing more great exchanges in the New Year.

With warmest wishes,

Carl and Asha

© Northern Trust