December U.S. employment report clouded by weather-related factors

January 10, 2014

- December U.S. employment report clouded by weather-related factors

- A review of the two U.S. employment surveys

- The ECB reaches a critical stage

We’ve experienced a nearly 60-degree (Fahrenheit) change in temperatures in the last few days here in Chicago. All the snow is melting, creating a fog that could easily compete with London’s version. This makes it terribly hard to see very far.

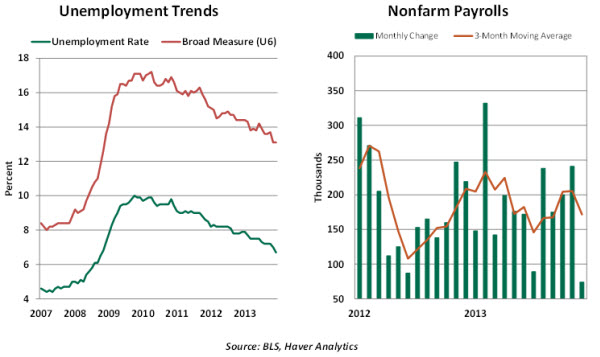

The vagaries of weather took their toll on the U.S. employment report, creating a fog that is difficult for economists to see through. Nonfarm payrolls rose only 74,000 in December, following a revised gain of 241,000 in November. In 2013, job growth averaged 182,000, nearly matching the increase seen in 2012 (+183,000).

Climate change played a significant role in the December employment numbers. The Bureau of Labor Statistics (BLS) reports absences due to bad weather in its survey of households. In December, 273,000 persons were away from work during the survey period because of inclement weather. The count for December is high compared with tallies reported for Decembers over the past decade (the average number absent from work in December is 166,000 over the last 10 years).

The status of these people in the labor force is still classified as “employed” in the household survey. However, they would not be counted in the establishment survey, which leads to a reduction in payroll jobs. We would expect to recover most of these in the months ahead.

Construction employment fell 16,000 in December, probably a weather-related event; this sector added on average 10,000 jobs per month in 2013. The small gain in leisure and hospital industry employment (+9,000), after stronger readings in the prior two months (+32,000 average), may also be attributable to the harsh elements.

The nation’s unemployment rate fell to 6.7% in December, the lowest since November 2008. The jobless rate has dropped 0.5 percentage points in a three-month period, a sizable decline. But, the bullish implications of the decline in the jobless rate must be muted because the participation rate fell 0.4 percentage points in the same period.

Discouraged workers – those who are currently not looking for work because they do not believe that jobs are available for them – increased 917,000 last month. This decline is part of the reason for the drop in the participation rate. The broad measure of unemployment (which includes marginally attached workers and those working part-time but who would prefer full-time work) held steady at 13.1% in December. These numbers suggest that the headline unemployment rate overstates the improvement in the labor market.

Today’s report will not, by itself, cause the Fed to alter its tapering plans. The bar is very high for the Fed to decelerate or accelerate asset purchases, as a steady pace holds out the best hope for orderly markets. The broad collection of U.S. economic data remains encouraging, suggesting that today’s news is a weather-related aberration.

In addition, the minutes of the December Federal Open Market Committee (FOMC) meeting suggest that the members are concerned about advancing asset prices and wondering whether continued asset purchases provide much benefit. These perspectives remain in place and argue for reduced additions to the Fed’s balance sheet.

Hopefully, the weather will stabilize soon, and our vision will be clear. And hopefully, that will allow us to send all of our snow- and salt-crusted clothes to the cleaners!

The Tale of Two Employment Surveys

The December 2013 employment report: Non-farm payrolls increased 74,000, and despite these tepid results, unemployment fell to 6.7% from 7%. Baffling data indeed. In this segment, we will attempt to sort out the confusion about employment numbers.

The BLS publishes the employment report each month using data obtained from two separate surveys – the household survey (which drives the unemployment rate) and the establishment survey (which determines payroll employment). The collection processes and concepts included in the two surveys are different and can occasionally lead to strange-looking outcomes.

The household survey data are gathered from interviews with 60,000 workers and extrapolated to account for the broader population. The household survey includes the self-employed, agricultural workers, unpaid family workers and those on unpaid leave.

By contrast, the universe of the establishment survey consists of data from 557,000 establishments, inclusive of both the government and the private sector. The survey counts nonfarm payroll jobs and does not include those who are self-employed. Multiple job-holders show up more than once.

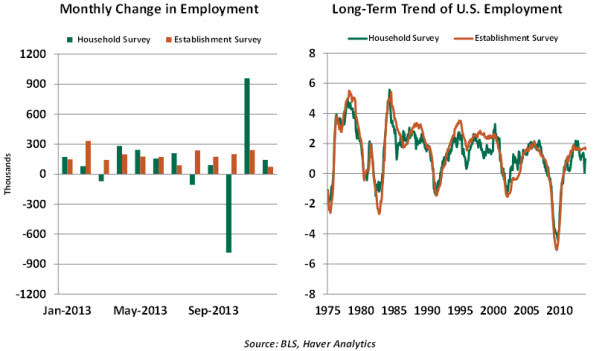

Effectively, the household survey measures the number of individuals employed and is broader in the scope of the types of employment it reflects, while the establishment survey counts the number of jobs. As a result of the differences in survey methodology and scope, the employment estimates from the two surveys can diverge in the short run. But their long-term trends track closely.

According to the BLS, short-term differences between the two series are from “large monthly swings in the household survey employment.” The volatility stems from the fact that the household survey has a smaller sample. It is not uncommon to find noticeable discrepancies in employment numbers from the two surveys, and they are visible over the past year, as the above chart shows.

On average, payroll employment advanced 182,000 per month last year, while employment in the household survey recorded an average monthly gain of 114,500. Some of this is due to structural differences between the surveys, as discussed above. But some have questioned whether the household survey is understating the pace of hiring and therefore overstating the unemployment rate.

These two results were in synch through September of last year and diverged substantially because the government shutdown affected the respective surveys. (Furloughed workers were considered employed in the establishment survey but not in the household survey.) We’ve recovered some of these jobs but apparently not all of them. So there may, in fact, be some upside potential here.

In sum, comparison of employment trends from the two BLS surveys is difficult because employment data are derived from different universes, and definitions of employment do not match. It may not be possible to quantify all the reasons for the discrepancies, so the best advice is to look at both sets of employment data over an extended period and focus less on month-to-month discrepancies.

Europe’s Fragmentation

The new year offers an opportunity to set a new course. Goals are established, resolutions are made, and hope runs high.

For some in Europe, the aim for 2014 is to keep a good thing going. But for others, the hope is to make a clear break from the past. The discussions surrounding central bank meetings in Europe this week illustrate this dichotomy.

The Bank of England (BoE) convened amid strengthening economic conditions and inflation that is running almost exactly at the targeted level of 2%. These outcomes seem to justify the BoE’s decision to end its quantitative easing program in 2012 and ultimately replace it with forward guidance. No changes in policy were recommended by the Monetary Policy Committee.

Speculation for this year centers on whether Governor Mark Carney and his colleagues will move toward raising short-term rates, or at the very least, modifying its forward guidance to acknowledge the improvement in fundamentals.

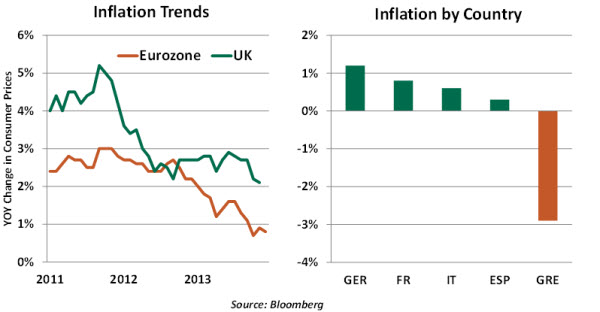

For the European Central Bank (ECB), however, such steps seem a long way off. The group’s resolve for 2014 was challenged immediately by the news that disinflation continues to deepen.

Designing policy to address the situation will continue to challenge the ECB. For one thing, price trends vary considerably within the eurozone; for some countries and for some products, deflation is already here. So members may have an uneven sense of urgency with regard to easing further. This is one of many fronts on which “fragmentation” within the community will present challenges for establishing economic policy.

And as we’ve discussed, it is not clear what else the ECB might do. Reducing refinancing rates to zero from 0.25% is unlikely to have much impact, given that credit channels in the eurozone are not flowing freely. Opening them further may take months, as the ECB carefully conducts an asset quality review of the region’s banks and follows that exercise with a full stress test.

In his press conference following Thursday’s meeting, ECB Chair Mario Draghi was quick to dismiss linkages between Europe’s current situation and the Japanese experience of 20 years ago. And he hinted at further aggressive steps, although he did not offer specifics on what these might be. These were the right things to say, in the name of sustaining confidence. But unless 2014 represents a break from the past, the eurozone could be facing the prolonged malaise that many are starting to dread.

© Northern Trust