The U.S. budget deal reduces policy uncertainty

January 17, 2014

- The U.S. budget deal reduces policy uncertainty

- The fiscal state of the states is better, but challenges remain

- Meeting the new cast at the Fed

I spent the majority of this week in Washington, D.C. catching up on the latest policy trends. The locals tell me that the multitude of budgetary and regulatory issues up for consideration created lots of business for lobbyists last year. Their dinner parties apparently crowded normal folk out of the best local restaurants. I didn’t notice, since I typically dine on cheap takeout while trying to scale my mountain of homework.

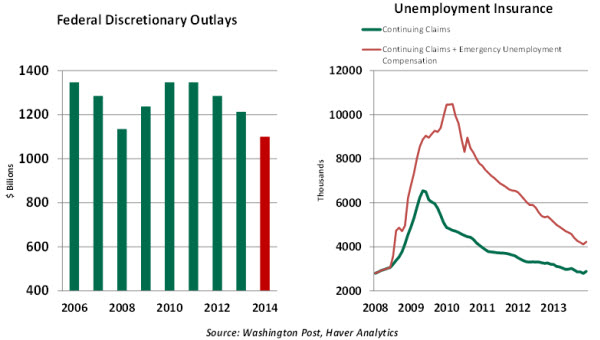

Well, the forecast for the lobbying sector this year may not be so upbeat. During the last weeks of 2013, Congress closed negotiations on broad spending authorizations for the next two fiscal years. Detailed plans for this year were finalized this week, the first time we’ve established a comprehensive budget since 2008. (Spending has been sustained with an endless series of continuing resolutions since then.)

This represents good news on a couple of levels. We’ve implemented considerable spending restraint over the past two years, which has helped to reduce Federal deficits. That trend will continue this year, but at a reduced rate that will produce a much smaller fiscal drag for the economy. Perhaps more importantly, the two-year deal reduces policy uncertainty and removes a challenge to business planning.

Our traveling group was uniformly pleased with this development, but somewhat mystified over why the bonhomie hadn’t produced a measure to raise the debt ceiling. The party lines were that the spending accord was all that they could agree on for now.

We are unlikely to breach the debt ceiling until late spring. In addition to the “extraordinary measures” it has used in the past, the Treasury can seek revenue remittance from Freddie Mac and Fannie Mae to help with cash flow. But investors would like something more lasting.

Some in Congress would like to seek additional fiscal reforms in exchange for raising the ceiling once again. The challenge is that modifications to entitlements would affect those in the lower income quintiles more heavily. With inequality of opportunity, income and wealth likely to be a theme on the mid-term campaign trail, compromise may be difficult to reach. We emphasized to the Congressmen that the threat of default was not a palatable strategy for financial markets, and we hope that our message was taken to heart.

One other issue left open by the compromise was the fate of more than 1 million people whose unemployment benefits expired in December. Debate continues over extending these benefits, but until this issue is resolved, these people will fall out of the labor force and create an artificial improvement in the unemployment rate.

We still have thorny fiscal issues to confront, but the absence of acrimony that surrounded the budget resolution is a welcome change from the salted-earth strategy taken by the two sides last October. Lobbyists may be disappointed, but the rest of us should be pleased.

The Local Angle

The origins of the financial crisis can be found on Wall Street, but its impact hit close to home for many. The millions of Americans that have faced home foreclosure in the intervening years endured a direct hit, while the shrapnel of economic consequences generated immense collateral damage around the world.

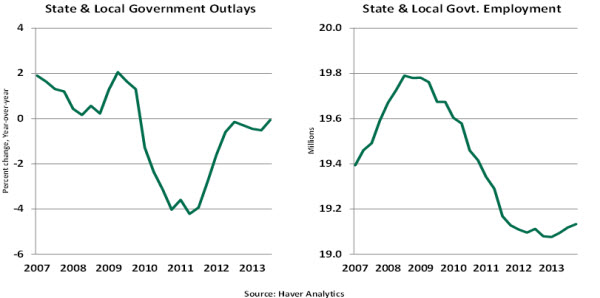

The after-shocks of the crisis hit close to home in another important way: the toll taken on budgets of U.S. state and local governments. While often overlooked amid the circus surrounding the Federal budget, the spending done at lower levels of the public sector is larger and accounts for a greater share of public employment. The retreat endured by both of these metrics has been a headwind for the current recovery.

As we begin 2014, though, the winds may finally be helping and not hurting. State budgets are much healthier, making room for additional spending and hiring. And while the long-term costs of retirement and health care continue to challenge local governments, progress has been made on these fronts, too.

Total spending by state and local governments was $1.9 trillion last year, accounting for 11% of gross domestic product (GDP). While both these numbers are down from their peaks, they remain substantial. Approximately 19 million people work for state and local governments, compared to 2.7 million on Federal payrolls.

Beyond this effect on the overall economy, state and local governments play an outsized role in two sectors: education and health care. These categories account for one dollar out of every two spent by states. State authorities are also primarily responsible for the maintenance of public infrastructure.

The recession and the ensuring modest recovery damaged governmental revenue sources. The pinch was felt more acutely at local levels, which rely on a mix of income, sales and property taxes for the lion’s share of their receipts. This created a “triple whammy” that substantially diminished state revenues. Since many states have balanced budget rules and limited ability to sustain “rainy day” funds, this forced deep cuts in personnel and service levels.

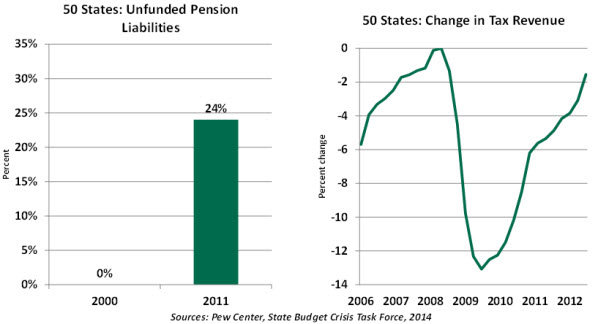

Further, the economic and market correction exacerbated funding shortfalls in public-sector pension plans. While they are increasingly rare in the private sector, pensions remain a very common benefit for government employees. (About 19 million people are due a public pension.) Legislatures have not always had the most actuarially sound perspective on these plans, even in the best of times. But declines in asset values and falling interest rates (which increase the present value of pension liabilities) made matters significantly worse.

Fortunes are certainly improving. State revenues recently began rising for the first time since the financial crisis, thanks to improving property values, retail sales and incomes. Higher interest rates have helped reduced pension shortfalls. Some areas have introduced reforms which have further reduced their long-term liabilities.

But challenges remain. Pension shortfalls aren’t the only holes that need to be closed. Gaps still exist in the investment done by states in human and physical capital. Declining public schools and crumbling roads may ultimately come to limit economic progress if not supported financially. More clearly needs to be done in these areas. The evolving terms of medical coverage will have an important impact on states, which are primarily responsible for the delivery of Medicaid.

The intense competition between states for business, with tax incentives used to sweeten the pot, makes it difficult for some to sustain a revenue base while applying fiscal discipline.

Hopefully, leaders at the state and local level have learned important lessons from the last five years that will provide perspective for the years ahead. It has been said that all politics are local … and a lot of economics is, too.

The FOMC’s Membership – More of the Same or Something New?

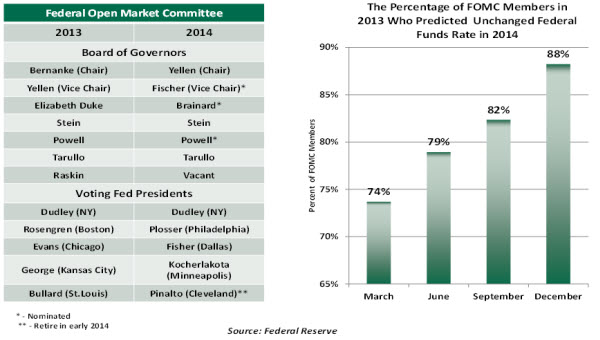

The Federal Open Market Committee’s (FOMC’s) composition in 2014 is noticeably different from 2013. Janet Yellen was confirmed on January 6 as the new head of the Federal Reserve. Three nominations to the Board of Governors and the annual rotation of Fed presidents as voting members is the other reason for the transformation of the committee in 2014.

Most significantly, Stanley Fischer has been nominated as the Vice Chairman of the Federal Reserve. Fischer’s work record is exceptional; he recently concluded a term as the head of The Bank of Israel. Previously, he was the First Deputy Managing Director of the International Monetary Fund (IMF); he also did a stint in Citibank and started his professional career in the hallowed halls of academia. Among his students were Ben Bernanke and Mario Draghi.

Fischer was deeply involved in the IMF programs during the 1997 Asian crisis. His range of experience and depth of academic knowledge will be especially valuable to the Fed as it winds down its asset purchase program. There had been some trepidation about having someone so strong in the second chair, but it appears that Yellen was strongly supportive of the selection.

The key question is what changes are likely to follow with a new cast of members at the FOMC.

Among the incoming voters from the Reserve Banks, Presidents Plosser and Fisher are monetary policy hawks (biased toward the price stability mandate). They are nearly certain to disagree with the doves on the FOMC, but it is not clear whether they will dissent over the Fed’s current path. President Kocherlakota of Minneapolis is very dovish, offering comments this week suggesting that the Fed needs to do more to reach its 2% inflation target.

As we have written before, we consider Yellen to be a data-driven pragmatist. Under her leadership, it will not be surprising if the Fed touches further on its communication strategy, as this has been a past focus of Yellen’s. Fisher’s opinions about forward guidance suggest that he may prefer less transparency than Yellen might.

As the chart indicates, the number of FOMC members predicting an unchanged federal funds rate in 2014 grew significantly as the year advanced. This survey, which included voting and non-voting members alike, suggests that there is more unanimity about the outlook and the course for policy as we entered the new year. Hopefully, this will diminish the likelihood of deeply split decisions, which would not be taken well by the financial markets.

Fed watching has been a spectator sport for a generation. The issues facing the Fed, and the new personalities that will be participating, promise to make this an especially interesting term. We’ll look forward to covering it for you.

© Northern Trust