The Bank of England gets what it wished for

January 24, 2014

- The Bank of England gets what it wished for

- U.S. capital spending: is 2014 the catch-up year?

The United States has enjoyed a surge in its exports over the past few quarters. This has been especially impressive, given the modest levels of economic growth seen in many other world markets. But it isn’t just goods and services that we’ve shipped overseas. We’ve been sending our monetary policy tactics to other countries as well.

The Bank of England (BoE), in particular, signed up for the full package: interest rates of zero, quantitative easing and forward guidance. In the United Kingdom, as in the United States, an expansion is gaining steam. There, as here, a target unemployment rate is the basis of the central bank’s forward guidance, and joblessness has fallen very close to that target. But there, as here, the BoE’s Monetary Policy Council (MPC) seems unlikely to follow through on its guidance by raising interest rates anytime soon.

How the Fed and the MPC handle this parallel challenge will go a long way toward determining whether announcing target levels for policy objectives is an effective means of central bank communication. Targets may lose their credibility if reaching them prompts relaxation instead of action.

In a sense, this is a happy set of circumstances. The outlook for the U.K. economy has strengthened considerably in the past six months. The International Monetary Fund was forced this week to upgrade its 2014 expectations for real gross domestic product (GDP) growth, raising the forecast to 2.4% from 1.9%. The sharp increase nonetheless falls short of many private-sector projections.

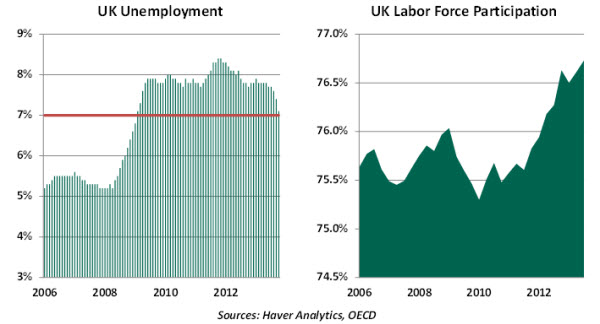

Reduced levels of unemployment have accompanied and abetted the acceleration. Joblessness in the United Kingdom fell to 7.1% in the most recent month, the lowest since early 2009. And a rising level of labor force participation enhances the strength of this outcome.

Last summer, the MPC established an unemployment target of 7% as the point at which short-term interest rates might come under review for an increase. Yet while this objective is near at hand, there seems to be no urgency to begin unwinding monetary accommodation.

The minutes of the January MPC meeting were filled with equivocation. While acknowledging that the recovery had become “more firmly entrenched,” the group noted subdued price pressures and lingering headwinds from the financial crisis as cautionary elements. In addition, the United Kingdom has had much better success of late than the United States in moving the long-term unemployed back into jobs, which may reduce the level of unemployment that would be associated with price pressure. Wages have increased by less than 1% over the past 12 months.

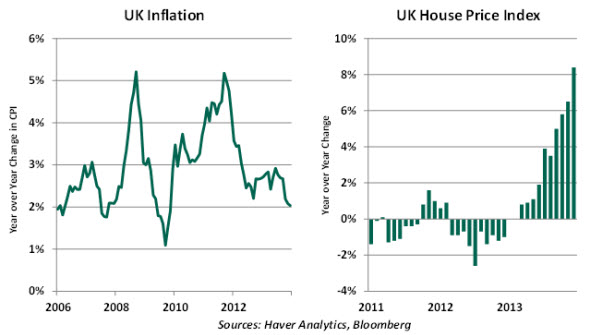

There may also be hesitation to commit to a change of posture because of the uncertain trend of U.K. inflation. After running well above the BoE’s 2% objective since 2010, the year-over-year change in consumer prices has fallen sharply and now stands at its targeted level. The question is: where will it go from here?

Governor Carney noted that inflation expectations have remained well-anchored despite the recent moderation. On the other side, however, one must wonder whether the disinflation seen over the past year could continue, bringing inflation below the targeted level by a considerable margin. There are certainly reasons why this might occur: lots of global capacity, weak commodities prices, and the strong pound, among them. The experience just across the English Channel in the eurozone may provide a glimpse of what lies ahead.

On the other side of the ledger, a different brand of inflation is working its way into the MPC debate. House prices are rising very rapidly, leading to worries of excess. While some call for a rate increase to slow the housing market, the BoE may try to deal with this situation through its supervision of banks. This sort of “macroprudential” policy is among the tools the Fed has suggested it would bring to bear in an effort to head off bubbles.

Should unemployment and inflation continue their recent declines, the MPC will be in a bit of a quandary. They would likely be forced to retreat from their promise to consider rate hikes at 7% unemployment, which some in the markets would consider a flip-flop. At the World Economic Forum in Davos this week, Governor Carney suggested that the link between unemployment and interest rates might be dropped altogether.

This predicament raises questions about the proper formulation of forward guidance and its standing among other tools of monetary policy. If specific terms within the guidance are subject to meaningful alteration, does this create a credibility problem for the central bank with investors? Will this be seen as a broken promise or a sensible reaction? A loss of face could create volatility or even the opposite outcome from what was intended.

There is a growing nostalgia for the days when central banks used vague phrases like “considerable period” or “foreseeable future” to bound the duration of their actions. Investors pressed for more specifics, but numeric thresholds have turned out to be just as ambiguous.

So while the Fed was the first to implement nontraditional monetary strategies, the BoE may be the first to unwind them. And it may be the first to test the power of macroprudential policy. The results might make for an interesting export back across the Atlantic.

U.S. Capital Spending – Will It Regain Momentum Soon?

There is optimism in the air about the performance of the U.S. economy in 2014, fully justified by the positive nature of incoming economic reports. One of the factors driving the optimism is the expectation that the disappointing trend of business capital spending (denoted as capex in the rest of the document) will turn around in 2014. The objective here is step back and assess whether there is enough evidence to support this forecast.

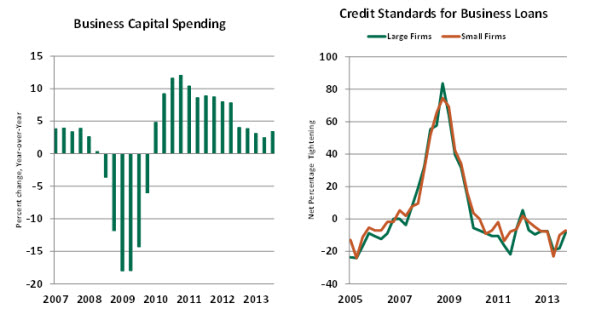

Capex in the current expansion shows three separate trends: robust performance in 2010 and 2011, moderate growth in 2012 and noticeably mild gains in 2013. An evaluation of credit conditions, cash holdings of firms and incentives for undertaking investment should shed light on the reasons for a deceleration of capex last year.

The Federal Reserve’s Senior Loan Officer Opinion Survey indicates that credit conditions have eased for large and small firms and do not present a challenge to those seeking loans for expansion or replacement of equipment. Certainly, large companies do not seem to face cash constraints; the Fed’s financial accounts indicate that non-financial companies were holding a hefty sum of $1.6 trillion as bank deposits and money market instruments in the third quarter of 2013, which is 9.3% of GDP. This is significantly higher than the 5.3% historical median.

One structural impediment is that U.S. firms currently hold significant amounts of their spare cash in overseas locations for tax reasons. Studies note that large companies with a global presence hold about three-quarters of their idle funds in their offshore locations, expecting a change in tax laws will enable them to bring profits back to the United States at a later date.

What cash is accessible has often been used to increase dividends or buy back shares. According to the Fed’s financial accounts, non-financial firms have bought back $1.5 trillion of equity since 2010, which is close to the $1.7 trillion in equity repurchases that occurred in the three years ended 2007. This suggests that firms may not see sufficient rates of return on the horizon and are choosing simply to return capital to their owners.

The bottom line is that the U.S. economy faces the co-existence of unimpressive capital spending and firms holding on to more-than-ample liquid assets, an unlikely combination during a business expansion. The net stock of private capital in recent years has posted the smallest increase of the entire post-war period. This threatens to limit long-term growth.

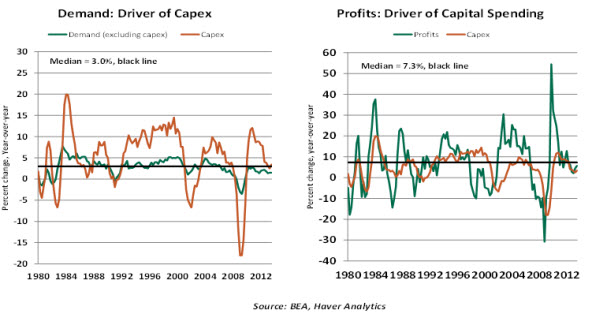

Looking ahead, are conditions ripe for a turnaround in capital spending? Aggregate demand and profits are factors that drive capital spending. Given projections of stronger growth in demand during 2014 compared with 2013, a pickup in capex is within reach.

Profit growth posted a decelerating trend in the latter half of 2012 and the first quarter of 2013 but regained momentum somewhat during the six months ended September 2013. Significant cuts in federal government spending held back growth in 2013. The absence of this headwind, combined with stronger fundamentals in the U.S economy, raises prospects of gains in profits in the quarters ahead. If this forecast is accurate, an increase in capex is strongly likely.

When placed in a historical context of previous business recoveries, capex growth in the current recovery stands in the middle, following the largest cyclical decline in the post-war period. It appears that a lack of confidence and modest demand have held back sustained growth in capex. Predictions of stronger overall growth in 2014 compared with last year’s performance are among the factors driving forecasts of a pickup in capex in 2014.

In the Business Roundtable CEO Economic Outlook Survey of December, 39% of participants expected capital spending to advance at a higher pace in the next six months compared with 30% reported for December 2013. Duke University’s Fuqua School of Business CFO Survey of December also showed a large number of respondents indicating an increase in capital expenditures in the next 12 months compared with their opinion a year ago. In sum, with credit ample and prospects brighter, capex should strengthen. And if this comes to pass, U.S. economic growth could surprise us on the upside.

© Northern Trust