China’s shadow banking products are coming under the spotlight

January 31, 2014

- China’s shadow banking products are coming under the spotlight

- Emerging markets: Be sure to differentiate

- The fixed income sector’s surprising strength

Today begins the lunar new year celebration. It is the year of the horse; those born under this sign are said to be animated and independent. Horses are comfortable in crowds, and learn quickly.

One wonders if we might soon see more of these qualities in the Chinese population as a whole, amid revelations regarding China’s shadow financial sector. Tremendous amounts of Chinese money have been invested outside of the official banking system, in products that are not very transparent. As inconvenient truths about these vehicles come to light, investors might gallop away in bunches. The consequences for China, and the rest of the world, could be significant.

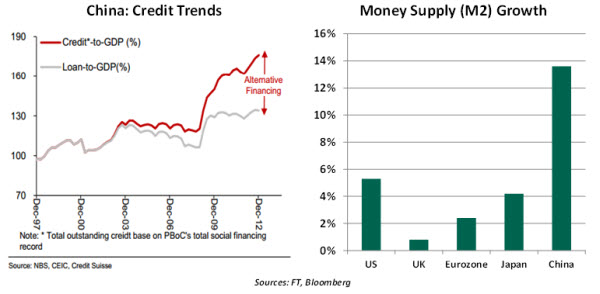

Development across China during the past 20 years has been nothing short of impressive. The boom in economic growth and market capitalization there has enriched the country and many of its citizens. This has created a broadening class of firms and individual investors who seek better returns than those available from domestic banks.

Because most Chinese are prohibited from purchasing foreign assets, and bank deposits offer real rates that are barely above zero, newly created capital has been recycled into domestic real estate and wealth management products (WMPs). WMPs come in a variety of forms; some are backed by pools of assets, some by specific projects. They typically promise to deliver 8% to 10% annual returns.

The flow of funds into WMPs has fueled a rapid expansion of credit that has proven difficult for Chinese authorities to control. The People’s Bank of China (PBoC) estimates that shadow banking accounted for about 30% (or about $1 trillion) of new credit issued last year, amid overall money supply growth that is among the fastest in the world. As always with China, this data must be taken with a grain of salt.

As big as China’s shadow banking sector has become, there is a dearth of detail about the sector as a whole or about the content of particular products. Some vehicles require refinancing or allow withdrawal before the close of the project period, creating a potentially risky mismatch. There is apparently very little regulatory guidance or oversight surrounding this activity.

The prime investors in WMPs are wealthy individuals and institutions, but the products are sold to individuals in a fashion very similar to how American mutual funds were sold in the late 1990s, when regulations allowed banks to market investment products directly to consumers. (The Chinese internet search engine Baidu advertises WMPs for sale on its main pages, and AliBaba supports them too.) In many cases, the investor leaves with either an implicit or an explicit guarantee of principal.

But earlier this month, Industrial and Commercial Bank of China – the world’s largest bank by total assets – announced it would no longer support a WMP worth approximately $500 million due to the failure of the underlying company. (The vehicle carried the ironic name “Credit Equals Gold.”) The consternation that followed this announcement was significant, and a mysterious supporter emerged only days later. Many assume that the PBoC either provided the funds, or made the arrangements for their receipt.

This step was seen as an insurance policy against broader instability. The behavioral economics of financial reversal are well-established; those who come to understand that their money is at significant risk when priors have been benign don’t respond in a measured way. Whether allowed by the investment structure or not, demands for redemption can feed a public perception that can place the financial system under tremendous strain.

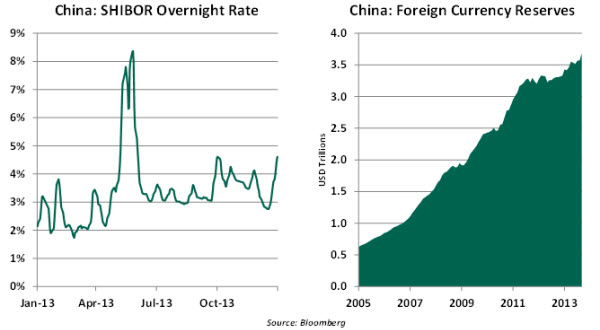

As was the case in the United States in the last decade, the PBoC will have difficulty dealing with the shadow banking system. It has the dual goals of preserving financial stability while curbing the financial excess that may have been accumulating. The first would suggest providing plenty of liquidity to markets, while the second entails curbing credit. Short-term borrowing rates in China have been very volatile over the past year, reflecting some uncertain steps by policy makers.

Now, it is very true that China is far better situated fiscally than either the United States or the eurozone were when trouble washed onto their shores. Beijing has a significant amount of firepower to throw at any problem that comes its way, including a vast reservoir of reserves that most think is sufficient to fill any holes in the banking system.

But the concern is that without reform, the investment of those funds will not rule out a recurrence. And the devotion of those funds to investor rescue precludes their use for further economic stimulus. So disorder in the shadow banking system could cause China’s growth rate to be lower that hoped for. And this outcome would impact economic and financial markets the world over.

Chinese officials have tended to downplay the apparent parallels of trouble created by shadow banks in the U.S. six years ago with what China is experiencing now. But with that memory so fresh in the minds of global investors, only an honest accounting for the activity will suffice. Because this is unlikely to be forthcoming, the mystery and anxiety surrounding China’s shadow banking system will continue.

It is traditional to set off fireworks during the lunar new year celebration, to scare off evil spirits. The international community is certainly hoping that whatever evil lurks within China’s shadow banking system can be reduced, without producing financial fireworks.

Emerging Markets Are Not All Alike

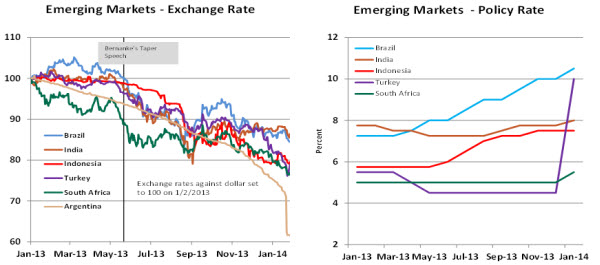

Turbulence in emerging markets commenced in May 2013 when Chairman Bernanke mentioned the possibility of a reduction in asset purchases in the months ahead. These markets stabilized briefly after it was clear that after tapering the transition to monetary policy tightening would be gradual. But emerging markets are exhibiting choppy conditions once again, and several currencies have lost significant value in the last month.

The highly accommodative stance of central banks of developed countries encouraged capital inflows to emerging markets. The transformation of the monetary policy stance of the United States and the United Kingdom, combined with reports of soft economic developments in China, changed the equation. The confluence of these factors triggered the sharp declines in the value of several emerging market currencies, particularly of countries with weak economic foundations and political uncertainties.

At first blush, it may appear that emerging markets are bystanders and victims of Fed monetary policy. Yet poor policy choices are also part of the problem.

At one end of the spectrum, Argentina faces a large current account deficit, has paltry foreign exchange reserves and is beset with 25% inflation. The rampant inflationary situation has driven the conversion of pesos to dollars as people seek a store of value. Argentina is an example of mismanagement because it made up inflation numbers and instituted capital controls that further impaired the situation. The current relative standing and the outlook for Argentina are both the poorest among emerging markets.

The experience of Brazil and India is different. Worrisome inflation trends were addressed with a long delay. The good news is that central banks in these nations have taken aggressive steps to contain inflation and stem the plunge of their currencies. The Brazilian central bank has raised the policy rate 325 basis points since April 2013 and maintains a hawkish position. The Reserve Bank of India’s latest 25 basis-point hike puts the policy rate at 8.0%, a 75 basis point increase in four months. Elections are around the corner in both countries, which raises uncertainty.

The Turkish central bank raised its overnight rate at the last minute to stem the currency plunge. Turkey has an oppressive current account deficit and inadequate reserves. The lira has failed to stabilize because the Turkish central bank has not issued a definitive commitment to contain inflation.

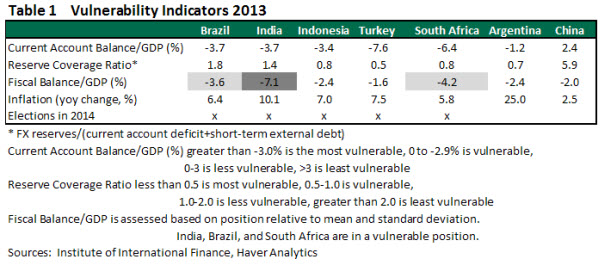

While the recent reaction has been a coordinated exodus, market participants will eventually begin differentiating between emerging markets. As shown in the table below, there is considerable diversity in economic standing among the community of nations most recently under pressure. Countries with large current account deficits, sparse international reserves, high inflation, large budget deficit and political uncertainties are more vulnerable than others.

The International Institute of Finance tracks capital inflows to emerging markets and it has noted that contrary to earlier estimates by private agencies, capital inflows slowed but did not evaporate during last summer’s fit in currency markets.

Constructive central bank policy actions in emerging markets are a positive development. Markets will remain sensitive to shifts in the Federal Reserve’s monetary policy path. A faster-than-expected tightening could lead to another round of adjustments in emerging markets with weak economic fundamentals.

The Fed cannot stem the plight of emerging markets. Respective central banks have to send a definitive message about their determination to contain inflation. There is no panacea; long-term structural reforms applicable to each country should improve market sentiment. History shows that currency market intervention is a temporary option.

At the end of the day, we are left with lower currency values, higher interest rates, possibly slower growth and a less inflationary environment in several emerging markets. But, the key is that emerging markets are not all alike.

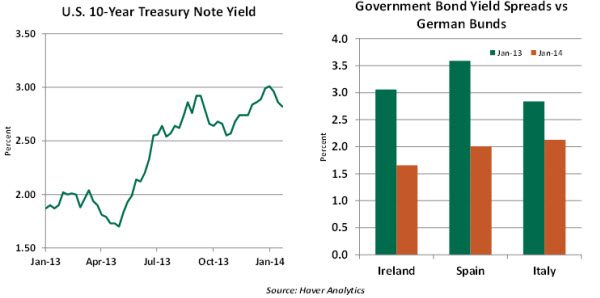

Bonds Make a Return

Six months ago, world bond markets seemed on the verge of a difficult period. Equities were rallying, and attracting lots of interest. Interest rates in the United States had begun rising from their generational lows, raising the prospect of negative returns to bond funds. There were heightened credit concerns around some bond issuers. The Fed was talking tapering, which some thought would presage an aggressive unwinding of quantitative ease.

Instead, many sectors of the bond market have been surprisingly strong recently. The 10-year U.S. Treasury note yield has fallen back after touching 3%. Corporate debt issues have been routinely oversubscribed. Even bonds issued by sovereigns with formerly questionable creditworthiness have been very popular.

The renewed popularity of fixed income appears due to several factors. Portfolio managers with targeted strategic allocations have moved to rebalance their holdings as equity values increase. Pension plans, which have seen their funded ratios improve as higher rates reduce the value of their liabilities, have taken the opportunity to de-risk and more closely match future cash flows. Some developed-market debt may also be benefitting from a mild flight to quality amid the questions surrounding emerging markets.

But additional clarity over central bank strategy is also providing an assist. The Fed and the Bank of England have indicated that they’ll be keeping short-term rates at zero long after their targeted unemployment rates are reached. The Fed’s tapering of quantitative easing seems to be moving along at a very leisurely pace. And with eurozone growth modest and uneven, some think that the ECB is more likely to reduce rates than raise them.

The thinking among many analysts six months ago was that fixed income was an asset class to be minimized. This has proven somewhat misguided. While bonds may occasionally lack the excitement of stocks, they shouldn’t be overlooked.

© Northern Trust