A number of central banks around the world tightened monetary policy during the week of January 27, but the rationale for their policy decisions varied significantly. In the U.S., the Federal Reserve continued its “tapering” of quantitative easing (QE) to reflect the strong economic growth prospects, while Turkey, India and South Africa tightened policy in an attempt to prevent an exodus of foreign capital from their countries.

- The recent flight of capital could persist in some emerging economies, but we believe the probability of a full blown emerging market (EM) crisis remains low.

- EM growth depends on developed market (DM) growth far more than the other way around, so we do not expect contagion from emerging economies to the U.S. economy.

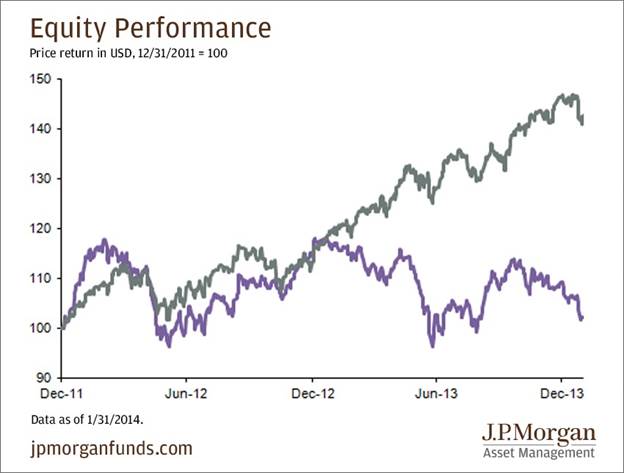

Equity Performance

Price return in USD, 12/31/2011 = 100

Sources: Standard & Poor’s, MSCI, J.P. Morgan Asset Management. For illustrative purposes only.

Data as of 1/31/2014.

How did we get here?

During the last few years, excess global liquidity, generated by ultra low U.S. interest rates, found its way to emerging economies, where consumers and corporations had healthy balance sheets and offered higher yields. Global investor capital flooded into those markets putting upward pressure on their currencies. Unfortunately for many countries, the currency appreciation ran too far and dragged on their global competitiveness, while some money was used to fund unproductive consumption. Instead of using a stronger currency to build a new rail system to transport goods, some countries used the stronger currency to buy bigger flat screen TVs from abroad. Over time, some of these economies developed large current account deficits as they imported goods and were less able to sell competitively abroad.

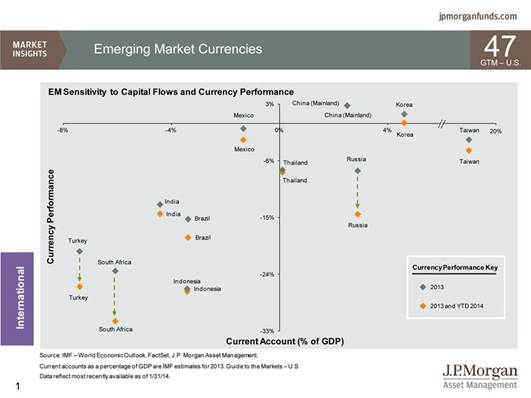

With the prospects of the global liquidity wave receding, the dependency of some EM countries on this overseas financing has lead to a “liquidity squeeze” in their markets, as skittish investors rushed for the door in the face of uncertainty. Page 47 of the Guide to the Markets illustrates the currency sell-off last year, highlighting that not all currencies are created equal across EM.

Countries such as Mexico and South Korea, with benign inflation and stronger current accounts, had more resilient currencies. Countries with significant current account deficits on the other hand, like Turkey, saw their currencies depreciate more than 20%.

Where are we now?

The pressures that had been building last year in EM finally came to a boiling point during the week of January 20, creating a global risk-off environment. (For more details on the global sell-off, refer to the market bulletin, What is leading the global sell-off?)

This week there were a number of policy reactions to the market sell-off, including:

- Turkey’s Central Bank raised its interest rates much more than expected during an emergency meeting, hiking its overnight lending rate 425 basis points to 12%, in response to recent weakness in the Turkish Lira.

- The Reserve Bank of India unexpectedly hiked its repo rate 25 basis points to 8.0%, citing inflation concerns.

- In South Africa, the weakening of the Rand, combined with concerning inflation and current account deficit outlooks, prompted the Reserve Bank to unexpectedly raise the key benchmark interest rate 50 basis points to 5.5%.

In the U.S., the Federal Reserve went ahead during the January FOMC meeting and announced its continuation in reduction of asset purchases, trimming its monthly pace by another $10 billion. Notably, given the recent angst around the emerging markets, the Fed made no mention of EM issues in its FOMC statement. As long as U.S. short-term interest rates remain anchored near zero, we do not believe “tapering” will be a catalyst for a more significant EM sell-off. (For more on this refer to Tapering on its own is meaningless…to emerging markets.) Nevertheless, it seems unlikely that the Fed will solve EM’s problems unless contagion spreads dramatically across global capital markets.

EM Credibility issues

Markets have met the recent EM monetary policy decisions with mixed reactions and the main issue seems to be a lack of credibility. Investors don’t believe leaders will make the tough decisions necessary to contain inflation, particularly if it comes at the risk of slowing economic growth. With important elections coming up in many EM countries this year, markets may be looking at recent policy measures as “one-offs,” rather than a true commitment to fix structural issues.

Source: J.P. Morgan Asset Management. Data are as of 1/31/2014.

Where Do We Go From Here

Emerging markets: For countries with significant current account deficits and high inflation, such as Turkey and Brazil, further currency depreciation is likely, at least until leaders are able to coordinate a credible plan to deal with their issues and thus earn back investors’ trust.

Some of the measures to watch for:

- Communication of continued rate hikes

- Continued rate hikes (risks slowing growth)

- Isolated currency interventions (using currency reserves built up over the last decade)

- Coordinated currency interventions (probably requires DM central banks to get involved)

- Fiscal incentives for foreign investors

As you can see on a revised version of page 47 from the Guide to the Markets, the danger of contagion and weakness spreading from vulnerable countries to stronger ones has increased, with countries like Mexico and Korea starting to see some currency depreciation. However, this still does not mean that all countries within emerging markets are dealing with the same problems (or to the same degree) as the countries mentioned above. It is also important to note that EM countries, relative to past decades, now have more flexible currencies, higher foreign reserves and lower debt levels which should diminish the potential for a full blown crisis. For long-term active investors, some contagion can create opportunities, as markets temporarily stop differentiating the good from the bad.

U.S. Equities: The U.S. economy is a relatively closed economy, driven by domestic consumption and thus not dependent on the rest of the world for its growth. Even if volatility in the emerging markets magnifies into a wider EM problem, EM growth depends on DM growth far more than the other way around, so we do not expect contagion to spread from emerging economies to the U.S. economy.

There are strong fundamental reasons to expect the U.S. economic growth to accelerate this year, so while U.S. markets and confidence could take a temporary hit because of market volatility emanating from the emerging markets, the impact should be minor for the U.S. economy.(Read Checking the Speedometer on the U.S. Economy, for more information on the prospects for U.S. growth in 2014.)

DISCLOSURES:

Any performance quoted is past performance and is not a guarantee of future results.

Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Reference to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

J.P. Morgan Asset Management does not predict outcomes of any political events, nor do we voice firm-wide opinions on any political candidates.

International investing involves a greater degree of risk and increased volatility. Changes in currency exchange rates and differences in accounting and taxation policies outside the U.S. can raise or lower returns. Also, some overseas markets may not be as politically and economically stable as the United States and other nations.

J.P. Morgan Asset Management is the marketing name for the asset management business of JPMorgan Chase & Co., and its affiliates worldwide.

JPMorgan Distribution Services, Inc., member FINRA/SIPC

MI-MB_EMGetIntoThisMess_Jan2014

© JPMorgan Chase & Co., January 31, 2014