Long-term unemployment needs to be addressed more intensively

February 7, 2014

- Long-term unemployment needs to be addressed more intensively

- January’s jobs data was very much a mixed bag

- Janet Yellen’s testimony will include thoughts on joblessness

Despite her apathy toward football, my 15-year-old daughter was excited on Super Bowl Sunday. Was it the cerebral play of Peyton Manning that interested her? The edginess of Seattle’s “legion of boom?” Neither, as it turns out: she wanted to see Bruno Mars perform at halftime.

“Who is Bruno Mars?” I asked. For people of my generation, Bruno was a performing bear and Mars was just a red planet. In response to that observation, my teenager gave me the look that I get all too often these days. “Dad,” her gaze indicated, “time has passed you by and no amount of re-education will make you hip again.”

When it comes to pop culture, she may be right. But at least for now, I remain professionally relevant, and I am thankful for that. For millions of other experienced Americans, however, the quest for renewed professional relevance is a work in progress. For them, re-education may be the key to success.

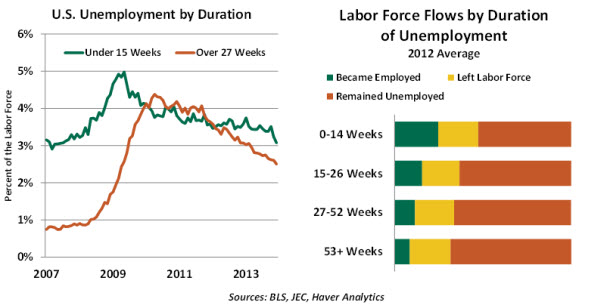

The United States labor market has come a long way since the double-digit unemployment of late 2009. Approximately 7.5 million jobs have been created, and the jobless rate has declined to less than 7%. But there remain more than 10 million Americans who are out of work and looking, nearly four million of whom have been out of work for 26 weeks or more.

The longer people are out of work, the more difficult it is for them to find new opportunities. In 2012, those out of work more than a year were one-third as likely to find a new opportunity as workers who had been displaced for less than 14 weeks.

We have certainly had periods of high unemployment before in the United States, but never one where long-term unemployment remained so high for so long. Further, the accounting above does not capture those who have left the labor force after being out of work for extended periods. A recent Congressional Budget Office report estimated that this cohort accounted for a 0.5% drop in the labor force participation rate.

The consequences of long-term unemployment are many and varied. Research has linked this sad state to poor health, poor family dynamics and deteriorating communities. From an economic perspective, the income loss endured by those out of work for more than a year is far greater than for those who find new work more promptly.

There is a general perception that remaining unemployed for a long time causes skills to atrophy and professional networks to thin out. There may also arise a stigma around this hardened core of the jobless that deters hiring managers.

Some have suggested that long-term unemployment is not an entirely uncomfortable situation, given the extension of jobless benefits and the availability of disability payments. Research does suggest that these factors have had an impact on the duration of unemployment but that the impact is relatively small. The loss of mobility (because of negative home equity) has also been cited, but this factor is also thought to be a minor one.

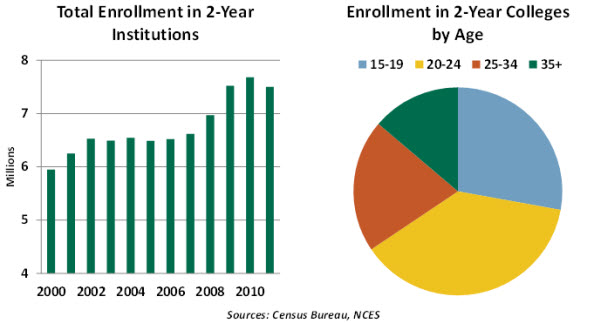

So what’s to be done? Certainly, a more-rapid rate of economic growth should be a big help. But re-education may be another avenue for policy to make a difference. Enrollment in two-year programs has been rising dramatically over the past decade. And adults make up a significant share of the student population at community colleges.

Community colleges often offer very specific vocational training in areas where labor demand exceeds supply. For mid-career professionals, these institutions offer an opportunity to fine-tune skills without starting from scratch. And employers find it convenient to work with placement offices to find candidates as opposed to generating them from advertising.

While community college typically costs far less than a four-year school does, it still represents an investment that many families find difficult to finance. As a result, some adults leave these programs before completion and fail to derive the full benefit of retraining. This leaves them much more likely to rely on public assistance of some form.

The challenging state of federal student loan programs has made many a bit wary about offering more grants or financing for post-secondary education. There are certainly both students and institutions that have used the system in ways that are not ideal. And in these challenging times for public budgets, every line item looks like a cost to be contained.

But a focused effort to help experienced professionals transition back to employment would be an investment and not an expense. Such a program could certainly pay for itself, creating more taxpayers and fewer beneficiaries. The restoration of self-esteem provided by a return to work would be an added dividend for those affected.

This would be a big assist to the Federal Reserve, which has employed the blunt instrument of monetary policy to achieve its goal of maximum employment. An assist from education policy could give the Fed more flexibility to manage its balance sheet.

I wonder if my local community college offers a course in contemporary teenage music. I hear that Drake is now a performer, not just a university in Iowa. I really do have a lot to learn….

January Employment Report – Mixed Signals with a Mild Positive Tone

The January employment numbers were expected to clear the muddy waters after a weather-related soft December report. Unfortunately, we have a mixed bag of employment data. The two employment surveys convey different messages about hiring conditions in January. The household survey has a more-solid tone compared with the establishment survey data.

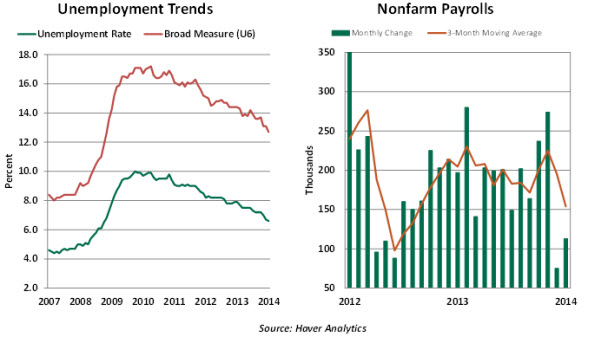

The unemployment rate edged down slightly to 6.6% in January from 6.7% in the prior month. The improvement in the unemployment rate reflects an increase in both employment and the participation rate (63.0% versus 62.8% in December).

The expiration of the Emergency Unemployment Compensation benefit has not translated into a lower participation rate as expected. The much-watched broad measure of unemployment dropped to 12.7% due to a sharp decline in part-time employment. The employment-population ratio during January rose to 58.8%, its best reading since November 2012.

The Bureau of Labor Statistics incorporated new population estimates with the January employment report. These numbers did not alter the participation rate but raised employment by 22,000. The January report also included benchmark revisions to the establishment survey, which added 369,000 jobs to the level of employment in March 2013. The upward revision was mainly from adding a new category that was previously not within the scope of this survey.

Payroll employment rose 113,000 in January, with revisions to November and December data adding only 34,000 new jobs. The three-month moving average slipped to 154,000 from 195,000 in December. Private sector hiring advanced 142,000 compared with an addition of only 89,000 jobs in December.

Construction (+48,000) and factory (+21,000) employment moved up in January. Health care employment appears to be slowing after making noteworthy contributions to the entire recovery. Government payrolls fell 29,000. A loss of 9,000 postal service jobs and declines in education-related employment explain the weakness in government employment.

All in all, the establishment survey results indicate that January was a month of modest growth in employment. Bad weather in the Midwest and the East appears to have played a small role and calls for a wait-and-see approach to assess if one-off factors prevailed in the last two months.

The Fed’s tapering plans are on track, for now. The Fed will have the opportunity to evaluate the February employment report and other economic numbers prior to the March 18-19 Federal Open Market Committee meeting. In our view, it is premature to classify the latest string of soft economic data as the beginning of slowing economic conditions.

Unemployment Rate Threshold – Modification Soon?

Janet Yellen, the new chair of the Federal Reserve, testifies at the House Financial Services Committee on February 11. It is her first report to Congress on the U.S. economy. Yellen’s view about U.S. labor market developments should feature prominently during the session.

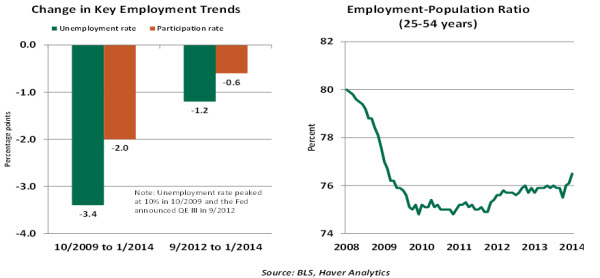

Since December 2012, the Fed has held that a 6.5% unemployment rate would trigger discussion of a higher federal funds rate, if not an immediate increase. This jobless measure has descended rapidly toward this objective.

As we’ve come closer to this objective, the Fed has hedged its reaction because falling labor force participation has accounted for a significant share of the change in the unemployment rate. By contrast, the prime-age employment-to-population ratio shows only a mild improvement since bottoming in 2009.

The Fed tweaked forward guidance in December 2013 to allow for accommodation well past the 6.5% unemployment rate, but our central bank is being pressured to provide a little more clarity. It could do so by changing this targeted level, adding some qualifications that reference trends in labor force participation or dropping the numeric reference in favor of something more vague.

In a June 2012 speech, Yellen defined optimal monetary policy as one that minimizes the “social cost resulting from deviations of inflation from the Committee’s longer-run goal and deviations of unemployment from its long-run normal rate.” How that philosophy might translate into the conduct and communication of monetary policy will be central to Yellen’s first Congressional testimony as Fed chair.

© Northern Trust