A Centennial to Celebrate - The Federal Reserve Looks Forward to Its Next 100 Years

A Centennial to Celebrate - The Federal Reserve Looks Forward to Its Next 100 Years

February 13, 2014

Given the rapid pace of cultural, civic and commercial change, few institutions reach their 100th birthdays. When they do, such events prompt reflection on origins and evolution.

This year marks the 100th anniversary of the Federal Reserve System. The Fed is not the world’s oldest central bank (the Swedish Riksbank dates from 1668), but it has certainly become the most prominent. Its actions have reverberated through a broad range of world capitals; its philosophies have been adopted by other monetary authorities; and its chairs have become leaders on the world stage.

The Fed’s centennial arrives at an interesting juncture. Never in its history has the American central bank been so deeply involved in economic management, and rarely has it attracted such controversy. The recent transition in Fed leadership marks the end of a significant era. In some ways, this makes it a perfect time to contemplate what the Fed was, what it has become and what it should be during its second century. The results of this review will be valuable to central banks the world over.

Born of Necessity

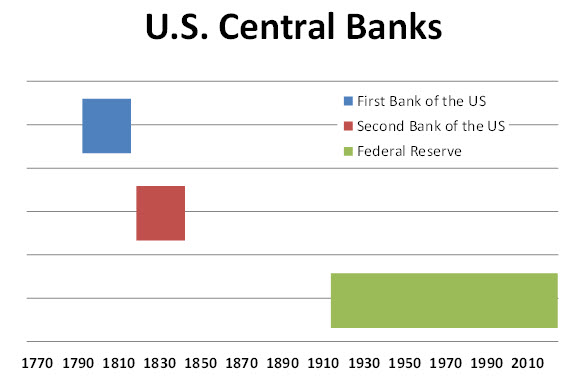

Many don’t realize that the creation of the Federal Reserve was actually the third attempt the United States made at establishing a central bank. For a substantial fraction of American history, there was no such presence.

After the closure of the Second Bank of the United States in 1836, American finance was very loosely controlled. Banks in many parts of the country issued their own currency, and there was little transparency surrounding the banking system. There were consequently a series of panics in the decades that followed, the most seismic being the trust-related meltdown of 1907. That episode ended only after J.P. Morgan placed his resources and reputation behind the system (and earned tidy profits for doing so).

In reflecting on the near-miss, policy makers feared there might come a day when such a powerful personage would not be in a position to ensure financial stability. (Morgan himself died in early 1913.) And so the idea of an American central bank, which had not existed for 75 years, again became attractive.

In order to provide perspective and de-centralize power, the Federal Reserve Act created 12 Reserve Districts, each with an independent Federal Reserve Bank. This structure is unique in central banking, and observers have certainly asked questions about its efficacy, given changing economic patterns over the past century. Nonetheless, the System endures.

While the motivation behind the Federal Reserve Act may have been financial stability, the specific objectives given to the new institution were maximum employment, price stability and moderate long-term interest rates. That last objective proved problematic, as the Fed was often under pressure during its initial decades to increase reserves and purchase Treasury debt. (Until 1935, the Treasury Secretary and the Comptroller of the Currency were members of the Federal Reserve Board.)

The bouts of inflation that inevitably followed eventually prompted the Treasury-Fed accord of 1951 that set the tone for central bank independence. And it left the Fed with the dual mandate of achieving stable prices and maximum employment, which Congress tweaked only modestly in the intervening years.

For the Record

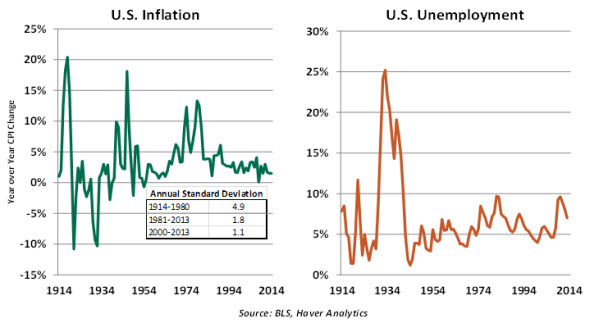

The Federal Reserve has generally had good success in achieving its economic objectives. Since the Great Depression (to which the Fed’s restriction of credit was a contributing factor), both inflation and unemployment have generally been lower and more stable.

Many commentators single out the taming of inflation through strict monetary targeting 35 years ago as the single greatest achievement of the Fed’s first century. It came at the cost of a terrible recession in 1979-81 but set the stage for nearly a generation of prosperity.

There are still those who wish that the Fed would manage the money supply to strict target ranges, as it did during that era. Unfortunately, getting a handle on the money supply became much more difficult as modern technology redefined the payments system.

Recognizing this, the Fed returned to the practice of interest-rate targeting but also adopted an inflation target of 2%. Consequently, actual and expected U.S. inflation have been well-anchored for many years, to the benefit of business and market performance.

The objectives given to the Fed are not the easiest to quantify. Inflation is most easily gauged for manufactured products, but it is an elusive concept in the service sector that has come to compose the lion’s share of gross domestic product (GDP). And very recent experience has taught us that there is no single measure that captures employment conditions comprehensively.

The explosion of international trade and capital flows in recent decades has challenged the Fed. The global nature of supply and demand influences American economic outcomes, yet an individual central bank controls domestic variables most closely. The presence or absence of capacity, which can drive inflation, must be assessed across national borders.

All of these factors challenge the application of monetary policy “rules,” the most prominent formulation of which was advanced by economist John Taylor. These mechanisms rely on actual and potential levels of economic variables, which are difficult to ascertain with precision. While these kinds of formulae are useful tools, discretion remains a substantial element of central bank decision-making.

Too Much Information?

The Fed’s strategy for communicating decisions and explaining the rationale behind them has evolved tremendously. Thirty years ago, no announcement was offered when policy changed; observers had to infer the shift from trading in the short-term money markets. Today, we have statements, minutes, transcripts, testimony, forecasts, press conferences and a broad range of speeches to sort through.

It is certainly fair to say that the Fed has become more transparent, but it is still sometimes far from clear. Some of this is due to the murky nature of economic data and functioning; we are dealing, after all, with a social science. But the multitude of communication channels can sometimes make it difficult to discern the Fed’s true intentions. And this is a limitation as the Fed seeks to manage market reaction in a manner that aids its objectives. To this day, the institution has mixed feelings about the media. I never thought I would see a sitting Fed chairman appear on “60 Minutes” or Fed presidents as morning hosts on CNBC. This has helped market the central bank’s message but leaves many on the inside uneasy. The confidentiality of monetary deliberations and supervisory information is something the Fed guards very closely.

One reason the Fed has been more vocal is that it needed to reach a new audience. Disintermediation has seen deposits and assets move outside the banking system, which is most immediately influenced by the Fed. Steering investor sentiment correctly has, therefore, become much more important to modulating the flows of credit in the economy.

This migration clouded the translation of money to credit and economic activity. It also created difficulty for the Fed as it tried to respond to the recent financial crisis, as the Fed did not have direct oversight of non-bank financial companies. (Ironically, capital standards enacted by the Fed and other regulators contributed substantially to the growth of the shadow banking system, which became a nexus of financial distress in 2008.)

The Fed’s thinking on the relationship between markets and the economy has evolved considerably. Monetary theorists for decades urged central banks to focus on “real” activity, under the assumption that asset markets were beyond their influence and largely self-governing. Bubbles, according to the accepted dogma, were impossible to diagnose and not within the Fed’s remit to correct.

Today, the linkages between the financial markets and real activity are better appreciated. Until relatively recently, few macro models employed a variable for financial conditions to help forecast economic activity. Today, few models are without such a feature. And behavioral economics is making more significant contributions to the understanding of how psychology influences outcomes.

The Fed as Supervisor

Prior to the 2008 crisis, there was considerable debate about whether major central banks should serve as both monetary authority and a supervisor of financial institutions. Proponents cited the value of two-way information flow, which was beneficial to both exercises. Opponents worried that supervisory policy might be overly shaped by monetary objectives, resulting in potentially destabilizing extremes of credit.

In the post-crisis world, the pendulum seems to have shifted dramatically in the opposite direction. The Federal Reserve is seen as the systemic risk regulator and now supervises financial companies that are very diverse. The Fed has armies of analysts following financial markets for signs of excess, and macroprudential policy (such as higher capital requirements or other supervisory limitations) is touted as a cure for bubbles before they form.

The success of this endeavor is far from assured. The track record of central banks in pulling the punch bowl away when the party gets going is not good; public, political and industry pressure may simply be too substantial to overcome.

When things do go wrong, the Fed is forced to go back to its origins as a lender of last resort. During these episodes, the central bank is confronted with accusations that it is an enabler of financial excess, allowing moral hazard to persist by serving as a backstop. The debate over “Too Big To Fail,” which started 30 years ago after the rescue of Continental Illinois National Bank (which had assets of only $40 billion at the time), still rages actively today.

It is terribly difficult to be simultaneously punitive and palliative. Having tried this and failed during the Depression, the Fed wisely stressed supportive measures as a remedy for the recent crisis, to very good effect. There is a lesson in this for other central banks.

Forecasting the Future

So what awaits the Federal Reserve as it begins its second century? The following themes will be critical in shaping the organization’s destiny:

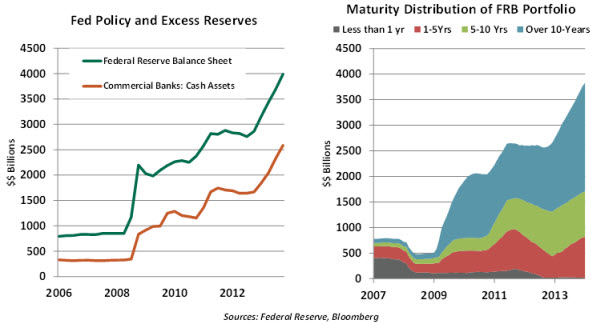

- Defining the New Normal. The Fed begins its second hundred years with a balance sheet that has been distended by several rounds of quantitative easing.

Some call the recent tapering of asset purchases the first step in the exit process, but until the Fed’s balance sheet actually starts to decline, they are still adding to the accommodation.

Real exit will present both tactical and political challenges. Intense debate will swirl around how and when to remove liquidity from the system. The Fed has stated its preference for holding its securities until their maturities, which are fairly lengthy. Its recently introduced reverse repo facility will, therefore, become a critical mechanism for modulating credit and economic activity.

Aggrieved parties will certainly object to reducing accommodation before all economic ills are remedied. But not doing so risks the consequences of excesses in the prices of goods or assets.

- Independence. Placing proper distance between governments and monetary authorities is critical. Countries lacking this separation usually experience trouble.

For the most part, Congress kept its distance from the Fed in the years leading up to the recent financial crisis. In the years since, the engagement has been much more significant. Part of this stems from normal fact-finding after such an infarction. The Fed was not alone in minimizing the warning signs that appeared prior to 2008, but it must nonetheless be called to account for its oversight.

But another part of Congressional angst springs from concern over how freely the Fed was able to expand its balance sheet. Some claim that monetary stimulus efforts have gone so far beyond past precedents that the Fed has annexed terrain normally trod by fiscal policy. As well, some could consider purchasing mortgage-backed securities as making housing policy and favoring one industry over others.

To register its displeasure, the legislature held up nominations to the Federal Reserve Board, leaving it short-handed. (One candidate, a Nobel Prize winner, was deemed by a ranking Senator to have insufficient background.) Calls are heard frequently for audits of monetary policy and changes to the Fed’s mandate. The Dodd-Frank Act placed additional limits on the Fed’s ability to act during crisis.

Given the rather disappointing track record of recent Congresses in managing the nation’s economic affairs, many think that re-establishing a studied difference between fiscal and monetary authorities is highly desirable. Returning the Fed’s balance sheet to a more modest level may help keep the wolves from the door.

-

Affirming a Mandate. Employment and price stability have been part of the Fed’s mandate from the beginning. The two objectives are not inconsistent with one another, and they are not overly burdensome. Other world central banks have much longer mission statements that include managing the value of national currencies and ensuring active markets for government debt.

On the one side, there are those who would prefer to simplify things further by eliminating the Fed’s goal of maximum employment. They point out, correctly, that employment is the product of a great many policies. Public investments in education, incentives for business formation and trade strategy all play roles in this arena.

But a poorly functioning economy will underutilize human resources. And as we’re currently learning, once a hard core of unemployed forms, it is difficult and expensive to dislodge.

On the other end, there are calls for the Fed to expand its scope to take more account of global conditions when setting policy. There are those who trace the recent correction in emerging markets to the first mention of tapering last May. That seems a stretch: local economic policy plays a much larger role in shaping perception and performance.

Yet the degree of financial and economic interconnectedness has mushroomed in the last generation, and it would be naïve for the Federal Reserve to operate in isolation. How best to broaden international perspective while remaining faithful to domestic objectives will require careful thought.

These seem like difficult issues, and they are. But they are a higher class of concerns than the ones faced in 2008. That graduation is a testament to the success of the Federal Reserve’s crisis response, which added to its reputation as one of the most admired organizations in the world. I felt privileged to work there.

That reputation is a great foundation as the Fed contemplates its future. Keeping that reputation and building on it will be a great challenge.

© Northern Trust