Turning and turning in the widening gyre

The falcon cannot hear the falconer;

Things fall apart; the centre cannot hold;

— William Butler Yeats, 1919

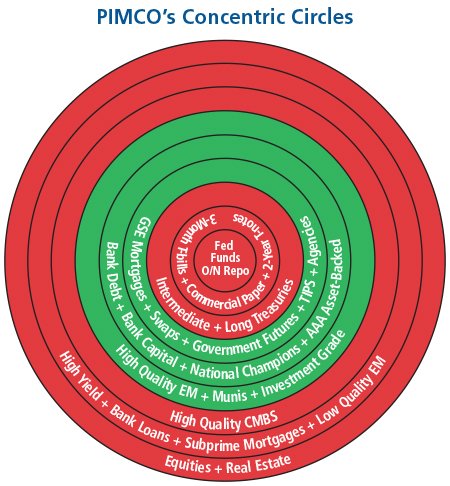

Almost permanently affixed on the whiteboard of PIMCO’s Investment Committee boardroom is a series of concentric circles, resembling the rings of agiant redwood, although in this case exhibiting an expanding continuum of asset classes with the safest in the center and the riskiest on the outer circles. Safest in the core are Treasury bills and overnight repo, which then turn outwards towards riskier notes and bonds, and then again into credit space with corporate, high yield, commodities and equities amongst others on the extremities. The intent of the image is to constantly remind us as investors that higher returns are correlated with greater risk, and that portfolios that seek to maximize beta usually do so with increasing volatility and potential loss of principal. Conversely, investors who are risk-averse and move towards the safety of the center, sacrifice expected and in most cases historical returns in the process.

Yet there is more to our concentric circles of asset classes than meets the eye. If its only message were that risk and return were correlated, then we could simply write that on the whiteboard and be done with it. Instead, our visual schematic expresses a more complicated process of cause and effect that allows an investor to anticipate price changes instead of simply describing ex post returns and volatility. It provides the foundation for alpha generation, as opposed to simple beta summation, and therefore the potential to beat the market and outperform competitors.

This conceptual “cause and effect” is what brings life to our concentric circles – it is what allows us – if done properly – to make profitable choices between asset classes at the appropriate time; it is the heart of our active management process and our YGIA “Your Global Investment Authority” platform. Stated perhaps too simply, the primary “cause” is central bank monetary policy. The “effect” is an expanding or contracting array of asset prices that are dependent upon it. Change the price of credit at the center and you change the price of assets at the outer extremities. Simple really, although the timing and yield of price at the center is no easy matter as Yellen, Carney, Draghi and Kuroda would be the first to admit.

In addition to the changing policy rate at the center, asset prices on the outer circles are dependent on investor expectations and the confidence in policymakers and the effectiveness of their policies. The center must have credibility, the center must “hold” or else the entire array of asset prices at the extremities is at risk.

This focus on the center brings to mind the rather ominous poem of William Butler Yeats cited above. Not that his conclusion as to the evolution of human history applies equally to financial assets – he was a poet, not an investor – but the metaphorical similarity to PIMCO’s concentric asset circles is striking. Yeats describes a falcon, which in this metaphorical context should be assumed to be the investor, “turning and turning in the widening gyre,” moving outward and outward in PIMCO’s concentric circles in search of higher and higher returns. Thefalconer of course, in our cause and effect model, is the global central banker, training the vulturous investor to swoop down and snatch attractively priced assets on command. But can the falcon hear the falconer ? Does the investor have confidence in the word and efficacy of the falconer’s artificially priced policy rate? Can the center hold?

It’s at this point where the metaphorical allusion and theoretical foundation of our concentric circles turn into strategy and potential alpha generation. If the center holds, if global central bankers can convince investors that their abnormal policies can recreate a semblance of the old normal economy, then risk assets at the outer edges of our circle will have higher future returns than otherwise. Presumably, the trickle-down wealth effect of appreciating assets will then lead to respectable growth rates and a reduction in unemployment worldwide. That of course is the presumption, the convincing of which will rely increasingly on what St. Louis Fed President James Bullard recently described as “ qualitative forward guidance” a shift from recent quantitative guidance that focused on unemployment rate thresholds that now are about to be breached. Not just in the U.S. but in the U.K., the new talk is centered on “quality,” not “quantity.” Will the “falcons” hear their master’s message?

PIMCO falcons are now turning and turning in the widening gyre with the following assumption: All financial assets are artificially priced if only because the policy rate at the center is artificially low. Historical models of fed funds and other global overnight yields suggest as much as a 2% artificially low yield, even when U.S. tapering is concluded. Importantly, however, these artificial pricings do not lead to the conclusion of current asset “mis”-pricings. As long as artificially low policy rates persist, then artificially high-priced risk assets are not necessarily mispriced. Low returning, yes, but mispriced? Not necessarily. Show me a perpetually low policy rate at the center, tell me that falcon investors are listening and believe in their masters, and it is reasonable to forecast at least a 12-month future where risk assets on the periphery can outperform the safest assets in the center. In plain English – stocks, bonds and other “carry”-sensitive assets would outperform cash. If, however, the longevity and effectiveness of that artificially low policy rate comes into question, then the center is at risk – it may not hold.

Investing is a combination of fundamental top-down/ bottom-up analysis as well as the critical element of timing. PIMCO’s concentric circles speak to the top-down, “cause and effect” correlation between policy rates, future policy rate expectations and risk asset pricing on the periphery. We have and have had a sense for several years now that ultimately central bank policy will be ineffective in promoting old normal economic growth rates and that asset pricing dependent on it will be low returning. In the short term, however, and to be specific for 2014, artificial prices will not be mispriced if circling falcons can be convinced of the efficacy of qualitative forward guidance. We believe that will be the case. Carry trades, then, in numerous forms should be profitable, although their information or Sharpe ratios may show that these positions provide historically low risk-adjusted returns once volatility is considered relative to lifeless cash.Most risk assets on the perimeter should provide positive returns relative to cash – in fact, an attractive strategy for alternative asset, unconstrained or even total return bond portfolios could be to slightly lever some of the safest carry trades. We would favor yield curve and investment grade credit spreads in this category, based on the assumption of 2% growth in the U.S. and steady rate falconers (central bankers) in developed economies.

Continue to be mindful, however, of longer-term consequences. As quantitative easing ends in the U.S., liquidity in corporate bonds will be challenged. If inflation begins to appear as a result of five years of artificially low policy rates worldwide, then assets may indeed be mispriced. 2014 may be the last of the years in which falconer and falcon act in capitalistic unison. Our entire finance-based system – anchored and captained by banks – is based upon carry and the ability to earn it. When credit is priced such that carry can no longer be profitable (or at least grow profits) at an acceptable amount of leverage/risk, then the system will stall or perhaps even tip. Until that point, however (or soon before), investors should stress an acceptable level of carry over and above index levels. The carry may not necessarily be credit based – it could be duration, curve, volatility or even currency related (with limits). But it must out-carry its bogey until the system itself breaks down. Timing that exit is obviously difficult and perilous, but critical for surviving in a new epoch.

Yeats’ “Second Coming,” when metaphorically applied to financial markets, has come and gone many times in the century since its writing – most often when highly levered economies failed to respond to their falconer’s command. Another “coming” is certainly in our future, but perhaps just not yet. Falcons, for now, can keep circling.

Past performance is not a guarantee or a reliable indicator of future results . All investments contain risk and may lose value.

This material contains the current opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material is distributed for informational purposes only. Forecasts, estimates, and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world.

© 2014, PIMCO.

© PIMCO