For the European Central Bank, actions will speak louder than words

April 4, 2014

The baseball season began this week in the United States. One of our local clubs, the Chicago Cubs, has not won a championship since just after the financial crisis … of 1907.

I recently spoke at a conference where I was followed by the Cubs’ Chairman. He noted the progress he saw in the organization: better facilities, highly rated junior players, and stronger finances. He shared an expectation that the club would soon win the World Series. All was going well, until a questioner reminded him that the team has lost more than sixty percent of its games during the past two years and has finished in last place for five years running.

I was thinking about that exchange while listening to Mario Draghi’s press conference following this week’s meeting of the European Central Bank (ECB) governing council. Asking for patience can be a sound strategy, but sustaining it requires tangible progress, not regression.

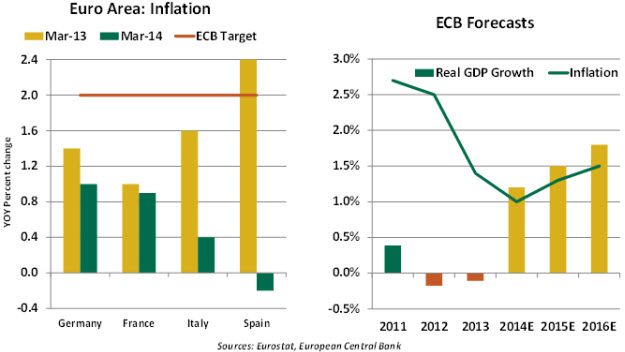

The eurozone has struggled since the financial crisis began, enduring two separate recessions and a sovereign debt crisis. Real gross domestic product (GDP) for the eurozone remains below its peak of first quarter 2008; in that interval, unemployment has risen from 7.2% to its current position of 11.9%. As a result, inflation in the eurozone has fallen sharply over the past year.

Some countries are experiencing outright deflation, and others are seeing it on a limited basis. To be sure, some of the downward pressure on prices is due to falling costs for food and energy, which may not persist. But soft demand and significant economic slack are also at play.

Amid this development, the ECB has made only very minor changes to its policy stance. Mr. Draghi has repeatedly urged us to look forward; in its most recent round of forecasts, the ECB projected an acceleration of growth this year, which would begin to reverse the fall in inflation.

But this outlook is by no means assured, because there are important headwinds to overcome.

- The ratio of household debt to income in the eurozone is higher than it is in the United States, and it is still rising. The need for deleveraging will limit growth in consumer spending. Falling inflation raises the real value of debt, which makes ultimate repayment more difficult.

- European banks have been slow to reckon with the credit problems created by the crisis, and have been conserving their capital by cutting back on lending. The ECB is presently performing an asset quality review, which many expect to result in additional write-downs and to lead some institutions to seek additional capital. It may be a while before the flow of credit improves.

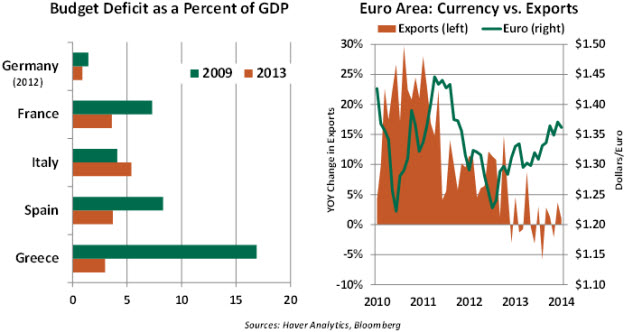

- The turn in the business cycle revealed or created significant budget problems among euro members. As a result, austerity has been stressed over growth. The good news is that annual deficits have declined importantly, but the bad news is that this has come at a substantial cost to economic activity.

While government deficits are under better control, most remain above the annual target of 3% of GDP set forth in the eurozone’s Growth and Stability Pact. Further, the level of sovereign debt borne by eurozone members remains well in excess of the ceiling set forth in the Pact. The mantle of austerity may lighten a bit over time, but it may remain in place for a considerable period.

- The ECB’s reluctance to act has contributed to the strength of the euro, which has hindered exports to countries outside of the eurozone. This has also raised imported inflation.

The ECB has made very sparing use of quantitative ease (QE). There are questions about how effective it is in the European context, where the vast majority of credit is extended through banks rather than the capital markets. More direct efforts to expand credit, like having the ECB purchase loans or asset-backed securities, carry significant challenges of design. And the courts may once again weigh in on the legality of new programs.

Whether by charter or choice, the main ECB strategy over the past year has been verbal. Mr. Draghi has tried to shape market perceptions by promising to “do whatever it takes,” or to “take extraordinary measures” if warranted. This week’s addition to the lexicon was “unanimous commitment to also using unconventional instruments within its mandate.” These statements have stabilized sovereign bond markets, but have failed to slow the march towards deflation.

The success of unconventional tools is by no means assured. While the early rounds of QE in the United States are generally viewed as being successful in retrospect, they were very much experimental when initiated. But the mere step of trying them made a strong statement. Perhaps it is time for the ECB to move from words to deeds.

The eurozone encompasses a population of 330 million people and produces GDP of about $13 trillion. The region is a very significant driver of world economic performance and the profitability of global corporations.

Many interested parties are therefore rooting very hard for Europe to succeed. But like Cub fans, some of them are getting impatient with leadership. In both arenas, we need performance, not just platitudes.

U.S. Hiring Is Back On Track

The headlines of the March employment report and revisions of January and February readings remove the pall that was hovering over labor market assessments after the first two months of the year. Firms are hiring at a decent pace and broad labor market fundamentals are improving.

The household survey numbers indicate an increase in employment (476,000) during March, but a steady unemployment rate at 6.7% because the participation rate rose to 63.2% from 63.0% in February. Greater participation, a rising ratio of employment to population, and lower long-term employment underscore that labor market conditions are strengthening.

The one blemish in the household survey is that part-time employment moved up in March (7.4 million versus 7.2 million in February). The elevated level of part-time employment is one of the labor market measures that Fed Chair Janet Yellen follows closely.

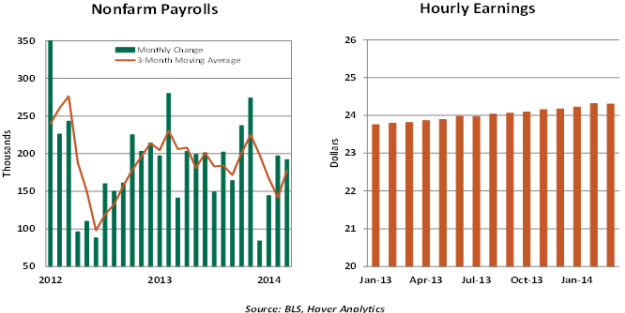

In the establishment survey, payroll employment moved up 192,000 in March, while revisions added 37,000 more jobs to the prior two months. The three-month moving average of gains in hiring at 178,000 is a vast improvement from a 142,000 average in February.

Employment in goods-producing sectors consisted of a small decline in factory jobs (-1,000) and an increase in construction hiring (+25,000). Service sector hiring rose a solid 167,000, with hiring in the private sector accounting for the entire increase as government employment was unchanged. The jump in retail employment (+21,300) after two months of declines was noteworthy. It represents a rebound after a weather-related hiatus.

The average workweek rose to 34.5 hours in March, tracing back the weather-related losses recorded from December 2013 through February 2014. Hourly earnings held steady in March, after a 0.4% increase in the prior month. More importantly, hourly earnings have barely budged in the past year. Wage trends are important, as they reflect the level of labor market slack and can be a leading indicator of changes in the inflation rate.

Of the labor market measures that Ms. Yellen noted in a speech earlier this week, the participation rate and long-term employment rate show improvement, but part-time employment and wage growth are still on the negative side of the ledger. While there is no doubt the Fed will announce another measured reduction of asset purchases at the April Federal Open Market Committee meeting, we continue to think that the first step in a tightening process is well over a year off.

The Debate Over Unemployment and Wage Pressure

As noted earlier, Fed Chair Yellen gave a very interesting speech on labor market conditions this week. It focused on her views about slack in the labor market; she reiterated that high part-time employment and elevated long-term unemployment represent important potential sources of labor supply. As such, they will act to hold down wages and justify monetary accommodation.

Her remarks contrasted a bit with a much-cited Brookings study indicating that low levels of short-term unemployment can pressure inflation. These findings would suggest an accelerated timetable for monetary restraint.

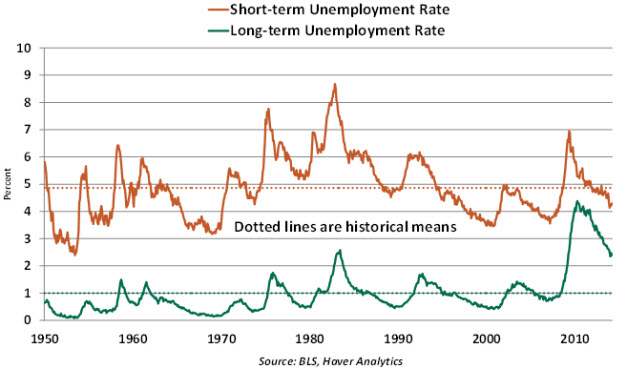

The distinction between short-term unemployment and long-term unemployment is a duration of unemployment of 26 weeks. Of those currently unemployed, a majority are experiencing short-term unemployment. The share of long-term unemployment (35.8%) is elevated, although it has declined from a historical high of 45.3%.

At the present time, short-term unemployment is below the historical mean. The latest long-term unemployment rate is not only higher than the historical mean, but stands far above the peaks of all prior recessions, with the exception of the mark following the 1981-82 recession.

The main thrust of studies examining the relationship between short-term and long-term unemployment and inflation is that as short-term unemployment approaches historical norms, it has the potential to create wage pressures and stoke inflationary concerns. By contrast, long-term unemployment has little influence on wages and inflation.

But the U.S. economy is experiencing elevated and persistent long-term unemployment to such an extent that the reaction of wages to short-term unemployment may be very different from the past. Recent wage trends suggest that conclusions derived from empirical testing could be vastly different in the current context.

As we have mentioned in the past, the outlook for labor costs will be central to the timing of Fed tightening. At the moment, the risk of significant upward pressure seems remote.

© Northern Trust