Much attention has been given recently to the complexities of U.S. equity market structure, and the potential for predatory high-frequency traders to work within that complex structure in a way that negatively impacts other market participants. There is no question the market structure faces challenges, but there are a number of tools and best practices that asset managers can utilize to mitigate the negative impact of high-frequency trading. We highlight many of those tools and practices below. While such tools can mitigate the impact of high-frequency trading, we are also working with the regulatory community to identify structural changes that would go a long way toward leveling the playing field for all market participants.

The Race for Speed

In the wake of Michael Lewis’ recent book, Flash Boys, never has there been such broad discussion and acute focus on U.S. equity market structure. To his credit, Lewis articulates a very complex topic to both practitioners and non-practitioners alike. He carefully describes the many eclectic facets of equity trading virtually unknown to the average investor, and sheds some light on why our markets often “just don’t feel right.” That said, Lewis often implies these issues are relatively new and that many market participants lacked the awareness and/or understanding of the market structure complexities until recently. There is also an inference in the book that the equity markets are “rigged.”

Changes in market structure, liquidity, and the potential for adverse effects on our clients has been on Janus’ radar, and that of many of our large asset manager peers, for quite some time. While the markets clearly face many structural challenges, the term rigged is quite strong and might spur reaction that distracts from the real issues. Equity markets are undeniably complex – not necessarily by design, but by means of evolution and technological innovation. And with complexity comes opportunity for some, and concern for others. It is our hope that efforts toward structural reform will eliminate some of this unnecessary complexity to allow for a healthier, more level playing field for a majority of market participants. While we will always advocate for a healthier market for the benefit of all market participants, we have also taken a number of steps to maximize our ability to access quality liquidity and mitigate our exposure to predatory high-frequency trading strategies.

Market Evolution: Proliferation of Exchanges and the Need for Speed

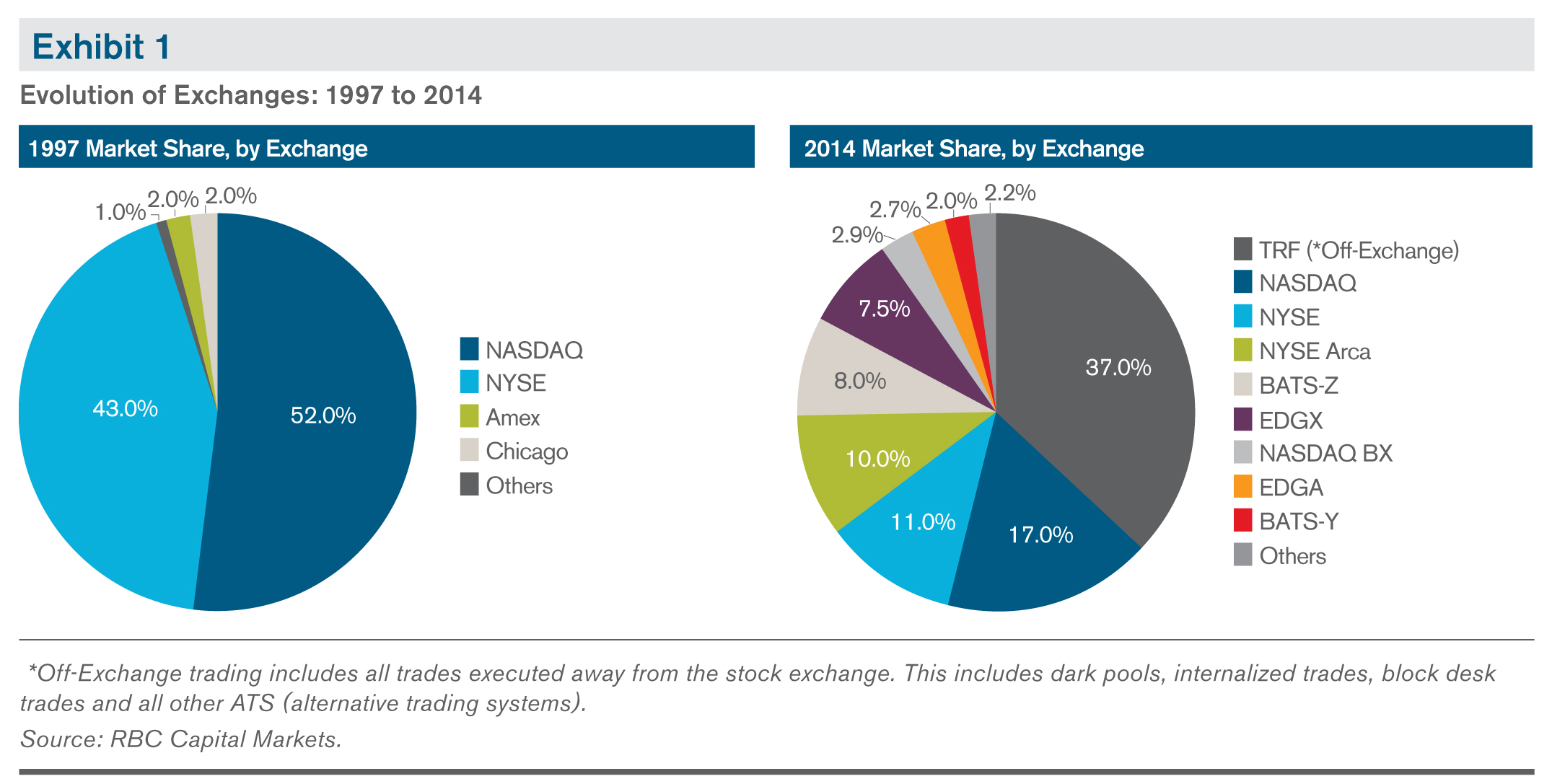

U.S. equity markets have dramatically evolved since the introduction of the National Market System (Reg. NMS) in 2007. The intent of Reg. NMS was to modernize and strengthen market structure, by fostering competition among the existing exchanges to promote efficiencies and fair pricing. What ensued was the creation of competition to the existing duopoly of NYSE and NASDAQ, with a proliferation of both traditional and nontraditional exchanges that became geographically fragmented (Exhibit 1).

Coupled with decimalization in 2001 (prices no longer expressed in fractions) and exchanges going public (no longer owned by their members) around 2006, the stage was set for technological evolution that created computerized competition and efficiencies, with electronic market making and increased arbitrage opportunities. The regulatory and structural shift prompted a race for speed, as short-term traders looked for any edge to exploit this new complexity. “Co-locating” client servers as close as possible to exchange servers, accessing faster fiber optic cable between trading centers, demanding faster data from each venue and acquiring top developers were all part of the frenzy by high-frequency trading (HFT) firms, including those considered “beneficial” as well as those considered “predatory.”

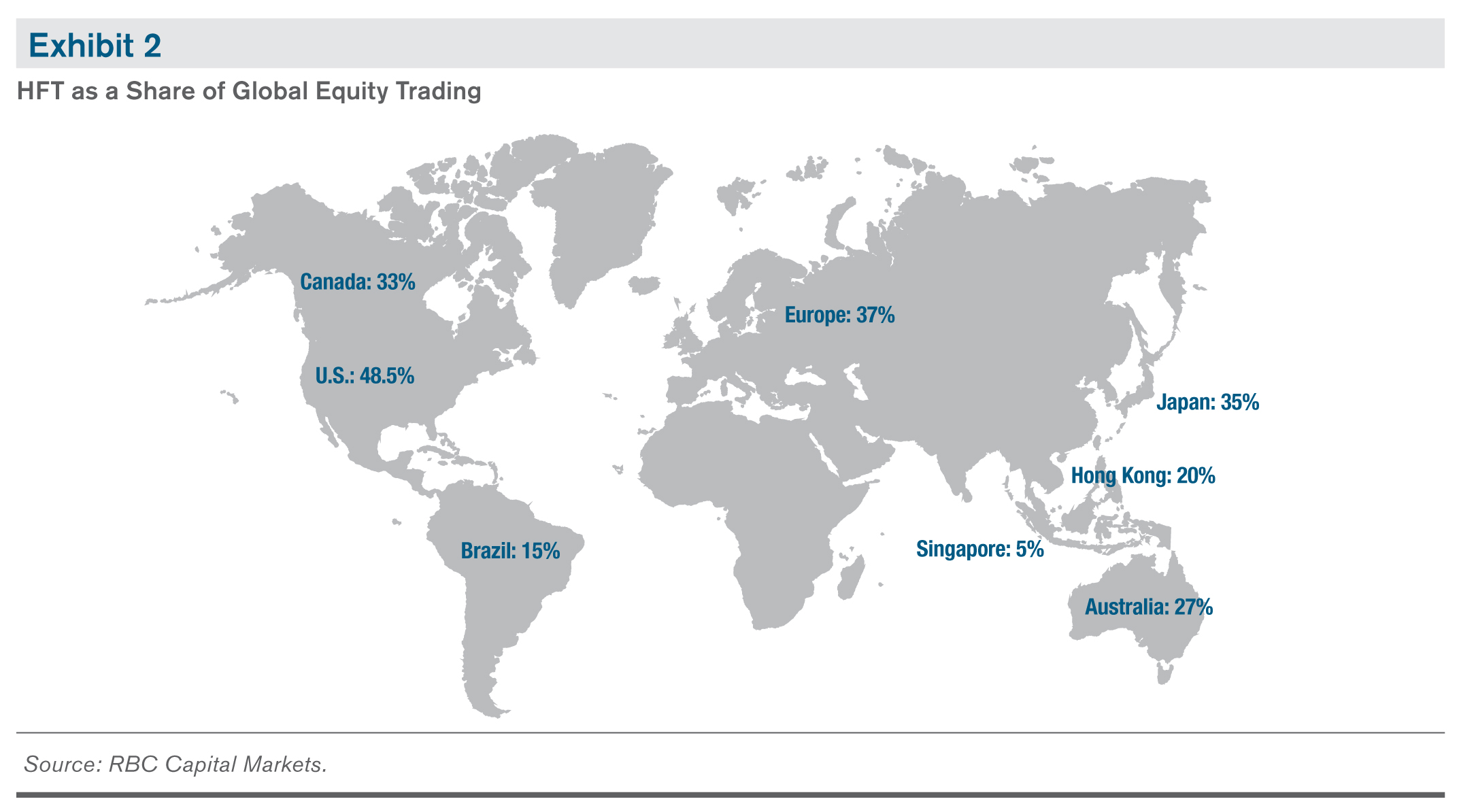

Not surprisingly, exchanges and brokers were all too willing to sell these products at a substantial premium. To put that into perspective, as pointed out by Lewis, Spread Networks charged clients either $360,000 per month for a 60-month commitment, or $10.6 million up front, for a connection between Chicago and New York that was 2.56 milliseconds faster than the existing connection. The race for speed was on. Over the next few years, HFT would garner increasing market share (Exhibit 2).

Competition for Trading Venues and the Institutional Marketplace

In addition to the technological arms race, exchanges offered a complex system of fees and rebates, known as a “maker/taker” model to incentivize volume to their exchange. The intent was to create a class of electronic market-makers that could supplant the specialists and traditional market-makers lost in this evolution. As originally designed, participants would be paid a small rebate to “make” one or both sides of the market (i.e., provide liquidity). These fees were capped by regulation, but within the confines of the cap, the decision was left to each exchange on how to implement the fee model, and thus structures varied widely between exchanges or between clients within an exchange.

As the maker/taker model evolved, several exchanges introduced an inverted rebate model that paid a participant to cross the spread between the bid and ask price and take liquidity (the taker). This begs the question as to why someone would pay to post liquidity, rather than get paid to post bids or offers on other venues. Yet this maker/taker system is an integral component to the decision process that brokers use to route their clients’ orders. If a broker has the opportunity to capture a rebate on part of a client order, it increases their margin on the fixed commission that the client pays.

Several HFT firms recognized how this might impact broker behavior and they were happy to pay to post prices in return for the information captured if the broker routed its orders there first. Complexity once again fueled the technology race. In addition to creating opportunities to exploit the differences between exchanges with geographic diversity through latency arbitrage, the market has now added the ability to exploit differences within this system and capture information on large institutional orders that need liquidity to exit a position in a portfolio or establish a new one. High-frequency traders seek to capture that information on the large order seeking liquidity, then trade in front of it and drive up the price.

This complex matrix of fee and rebate provisions introduced layers of economic conflicts to brokers’ routing decisions. Brokers were now faced with the decision to get paid to route their clients’ orders to potentially toxic venues or incur additional cost to route to seemingly safer venues. It all resulted in an environment that prompted brokers to internalize order flow into their own “dark pools” to alleviate potential costs and generate revenue. Dark pools facilitate equity transactions without providing bid/offer quotes. Transactions are eventually reported, yet there is little public transparency beyond a simple transmission. The dark pools initially served two functions: 1) by providing a venue to seek liquidity without exposing the order broadly, and 2) by allowing brokers to reduce their transactions costs. In order to be desirable, dark pools require liquidity, and many brokers resorted to inviting a variety of their HFT accounts to participate, which only increased the potential for economic conflicts. Brokers also allowed connections to other broker-sponsored dark pools that in turn included more and more HTF entities. How or which trade was routed to any particular destination has become a nearly unfathomable economic and algorithmic problem.

Buy-Side Leadership Adapts to Market Structure Change

Janus has been in front of this evolution and trading transformation for quite some time. Being students of market structure has helped us ask the right questions of trading partners and establish the proper protections to mitigate the gaming of our orders. Our traders have long been members of various boards and collaborated with regulatory bodies, industry groups and heads of a number of different exchanges to work toward creating a healthier market for all market participants. Just as important, we have also worked closely with trading partners to identify and develop best-of-breed tools that maximize our effectiveness in accessing liquidity for our trading needs. We utilize many channels to access market liquidity that eliminate, or significantly mitigate, exposure to predatory behavior by HFT participants and we have generally been early adopters of many differentiated solutions, described below:

Institutional-focused Crossing Networks. First and foremost, we make extensive use of institutional-focused crossing networks. These brokers, such as Liquidnet, ITG, BIDS and Blockcross, service a community of institutional clients, providing a mechanism to match client buy and sell interest in block transactions without the intermediation of HFT participants. This segment generally represents a significant portion of our order flow for any given period and varies based on crossing opportunities. The providers in this channel have been core partners with Janus long before the implementation of Reg. NMS and their importance has only grown through this technological evolution.

Block Trades. Following crossing networks, we are also large proponents of utilizing block trades and liquidity situations presented via “high touch” channels, where the broker manually coordinates transactions of large blocks of shares, typically 10,000 shares or more, between natural buyers and sellers. Through a variety of information resources, we attempt to best identify opportunities where we can access suitable true liquidity situations. We feel that when available, liquidity situations in the form of larger share amounts help mitigate the potential for adverse impact caused by predatory HFT activity.

New Technology Solutions. In addition to our ability to source block liquidity, we have been early adopters of new technology solutions that improve our ability to access quality liquidity. For instance, RBC’s “Thor” technology significantly improved the effectiveness of a router’s ability to access liquidity and minimize “fading liquidity,” meaning the HFT tactic of withdrawing bids or offers in multiple venues after a transaction occurs in one venue. Thor, which is mentioned in Lewis’ book, compressed the latency differentiation between arrival times to various routing destinations, and resulted in a significant reduction in fading liquidity and much higher participation rates on our orders. We recognized this was a better “mouse trap” and became RBC’s first institutional client on their new routing technology.

Flash Boys focused on IEX, another entrepreneurial solution to many of the structural challenges market participants face. The founders of IEX were a key part of RBC’s electronic and market structure team. Given our close partnership with the RBC team, Janus participated in the initial discussions about the IEX concept and remained an integral part of the discussions through its launch last year. We are firm believers that IEX is a differentiated tool, serve on its Advisory Committee, and remain an active participant on the platform.

Algorithmic Products. In response to the technological revolution, broker dealers have long offered a wide range of complex algorithmic (“Algo”) tools institutional traders such as Janus can use to access equity markets. These products perform a number of complicated decisions in accessing markets in an electronic manner. Used in coordination with our previously mentioned products and tools, Algo trading products provide a critical method of access to liquidity. These tools are complex and diverse in nature. Yet, we have structured our trading platform to facilitate a meaningful analytical process, utilizing quantitative metrics, trader feedback, routing analysis and economic impact to the broker. Coupled with the ongoing, dynamic dialogue of the Algo providers, we attempt to optimize performance and feel we have developed a suite of trading tools considered best of breed in the industry. Collectively, our traders are equipped with a selection of trading products that is among the best. By staying well informed on market structure issues and maintaining an ongoing dialogue with our trading partners, we feel we are able to provide our traders (and thus our clients) with the most effective tools to access the market.

Fostering Market Structure Reform

While we believe the tools we use make Janus capable of navigating the current market structure in a way that mitigates the potential impact of HFT, we still believe it is in the best interest of our clients for us to continue fostering market structure reform in any way that we can. Historically, buy-side community interaction has often been limited and disjointed due to the inherent competition we have with each other. However, as market structure has become more complex, it has become clear that cooperation and collaboration toward a common goal can benefit us all.

Over the last several years, Janus, in collaboration with other large buy-side asset managers, has been meeting with regulators to express concern, and encourage structural changes based on our collective experience. Given the vast swath of investors that this group collectively represents, there is significant interest among the regulatory community to understand our concerns. This group has identified certain structural challenges that if mitigated, can go a long way toward leveling the playing field for all market participants.

For example, we believe the maker/taker model has run its course, creating economic conflict and unnecessary complexity. The model has the potential to cloud the routing decisions the brokers face with our orders, and it supports additional exchanges that exist solely for the purpose of rebate capture. It also facilitates an extensive list of complex order types, which exist for rebate capture. Lastly, it imposes a toll charge on brokers routing for clients and encourages off-exchange activity, driving volume to dark pools. In this case, eliminating the rebate component of the maker/taker model would be a relatively simple change that could facilitate a large step forward in simplifying our complex equity markets.

Conclusion

Michael Lewis has successfully sparked a robust discussion around HFT and brought it to the attention of a broad audience, including our clients. Shedding light on many of the issues that have silently been part of our world for years will only help foster a broader discussion and help expedite reform to the betterment of market participants. While we recognize there are opportunities for structural improvement within our equity markets, and will continue to advocate for those improvements on behalf of all our own clients and all other market participants, we also believe the negative impacts of predatory HFT can be mitigated. Our seasoned professionals continually strive to utilize the best tools and solutions available in order to navigate the realities of the current trading environment and keep trading a core competency at Janus.

Please consider the charges, risks, expenses and investment objectives carefully before investing. For a prospectus or, if available, a summary prospectus containing this and other information, please call Janus at 877.33JANUS (52687) or download the file from janus.com/info. Read it carefully before you invest or send money.

Past performance is no guarantee of future results.

Investing involves risk, including the possible loss of principal and fluctuation of value.

The opinions are those of the authors as of April 2014 and are subject to change at any time due to changes in market or economic conditions. The comments should not be construed as a recommendation of individual holdings or market sectors, but as an illustration of broader themes.

In preparing this document, Janus has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources.

Statements in the brief that reflect projections or expectations of future financial or economic performance of a strategy, or of markets in general, and statements of any Janus strategies’ plans and objectives for future operations are forward-looking statements. Actual results or events may differ materially from those projected, estimated, assumed or anticipated in any such forward-looking statement. Important factors that could result in such differences, in addition to the other factors noted with forward-looking statements, include general economic conditions such as inflation, recession and interest rates.

Janus Distributors LLC

FOR MORE INFORMATION CONTACT JANUS

151 Detroit Street, Denver, CO 80206 I 800.668.0434

C-0414-62322 04-30-15

188-15-27922 04-14