SUMMARY

- Tax rates for the highest income earners rose by nearly 30% in 2013 due to increases on ordinary and investment income taxes, a new health care tax and reinstated limitations.

- The effective tax rate on these investors, including the impact of state taxes, can push many investors into the 50% tax bracket range.

- Tax-exempt interest income from municipal bonds may have become more attractive to investors as a result of the increased tax rates.

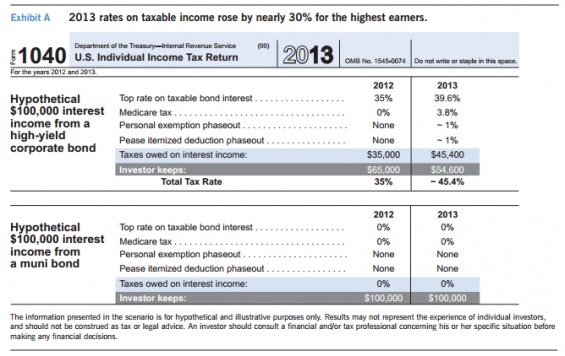

Here is a sobering fact: Investors in the highest tax bracket gave roughly half of their taxable bond investment income to Uncle Sam in the 2013 tax year. Combining federal and state taxes, many investors may find themselves in tax brackets as high as 50% once their 2013 tax bill is paid, a surprising increase from only one year ago. By contrast, the 2013 tax rate for tax-exempt municipal bonds (munis) is far more manageable at 0%.

Higher tax rates may highlight the increased value of muni bonds’ tax exemption. The combined effect of several recent tax increases (capital gains, ordinary income, health care and reinstated limitations) has increased the tax burden on many investors, who should not wait until December to begin thinking about next year’s tax bill. We think many investors should start thinking about the next tax year now and consider tax-exempt muni bonds to potentially help offset the pinch of higher taxes going forward.

How much more are you paying in taxes?

The increase in 2013’s tax bill should not be a surprise to anyone. Here are the details: The American Taxpayer Relief Act of 2012 raised the top marginal tax rate on income to 39.6%, an increase from 35% a year ago (Source: IRS). The new Medicare tax of 3.8% increased the tax rate for the highest earners to 43.4%. It is important to note that income from muni bonds is exempt from this tax. There was also a “stealth†tax increase, given the new limitations on exemptions and itemized deductions. While these provisions do not explicitly increase the tax rate, they each effectively increased the overall amount of taxes paid by high-net-worth investors by approximately 1%.

In total, the highest federal rate for many investors topped 45%, an increase of nearly 30% from the effective rate in 2012. We believe it is helpful to put the numbers to work in an example (above) using a taxable investment in a nonqualified account.

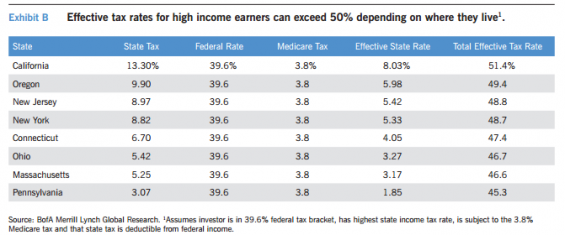

Don’t forget state taxes when calculating your effective rate

If high income earners are wincing at paying more than 45% on investment income, the rate may have been even higher when accounting for their state of residence. The table above highlights several states where the total rate approaches (and in the case of California, exceeds) 50%.

The inherent tax benefits of munis may help tax-worried investors

Interest income from munis is generally exempt from federal income taxes and, if the bonds are held by an investor residing in the issuer state, they may be exempt from state and local income taxes as well. Given the higher tax environment, we think investing in munis remains valuable within a diversified portfolio, particularly for income-seeking investors in higher tax brackets.

On an absolute basis, munis may often have lower yields than taxable counterparts in the fixed-income space, such as Treasurys and corporate bonds. But because of their tax-exempt income, munis have traded historically at 85% to 90% of comparable-duration Treasury bonds. As of June 30, 2014, AAA-rated munis on the long end of the curve yield 98% of similar-maturity Treasury securities, which may make munis more appealing from a value perspective to high income earners.

Focus on the taxable-equivalent yields of muni bonds

When comparing munis to other taxable fixed-income alternatives, investors should examine the taxable-equivalent yield to determine whether it represents a good value. As of June 30, 2014, munis (as measured by the BofA Merrill Lynch U.S. Municipal Securities Index) were yielding 2.46% on a pretax basis. Under the 2012 maximum tax rate of 35%, that is equivalent to a 3.78% taxable instrument. But under the new 2013 maximum rate of 43.4%, which includes the new Medicare tax, the taxable-equivalent rate jumps to 4.35%. It is rare in the investing world to receive an extra benefit without also boosting risk, but that is the case here, courtesy of rising tax rates.

A renewed appreciation of municipal bonds as a tax-avoidance tool may keep the market well-supported throughout the remainder of the year, and potentially result in municipal outperformance relative to taxable alternatives.

Consider professional management to navigate the risks of the muni market

As we’ve shown, munis may hold value in a rising tax rate environment. For investors concerned about the tax drag on their portfolio, tax-free muni income may hold strong appeal. We think both high-net-worth and less affluent investors should consider munis when pursuing a tax-aware investment approach, in consultation with their financial and tax advisors.

Similarly, investors would benefit, in our view, from skilled professional management and credit research when investing in the broad muni market. We believe that issuer balance sheets are generally improving and conditions in the U.S. economy are also improving. But with more than 60,000 different issuers, over one million CUSIPs and about $3.7 trillion outstanding, making generalizations about the broad muni market’s outlook is challenging, if not impossible. Given the size and the disparity of the muni bond market, credit research remains paramount.

Disclosure

Ratings are based on Moody’s, S&P or Fitch, as applicable. If securities are rated differently by the ratings agencies, the higher rating is applied. Ratings, which are subject to change, apply to the creditworthiness of the issuers of the underlying securities and not to the Fund or its shares. Credit ratings measure the quality of a bond based on the issuer’s creditworthiness, with ratings ranging from AAA, being the highest, to D, being the lowest based on S&P’s measures. Ratings of BBB or higher by Standard and Poor’s or Fitch (Baa or higher by Moody’s) are considered to be investment grade quality. Credit ratings are based largely on the ratings agency’s analysis at the time of rating. The rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition and does not necessarily reflect its assessment of the volatility of a security’s market value or of the liquidity of an investment in the security. Holdings designated as “Not Rated†are not rated by the national ratings agencies stated above.

The views expressed in this update are those of Eaton Vance and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund.

Eaton Vance does not provide legal or tax advice. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Individuals should consult their own legal and tax counsel as to matters discussed.

About Risk

An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There generally is limited public information about municipal issuers. As interest rates rise, the value of certain income investments is likely to decline. Longer-term bonds typically are more sensitive to interest-rate changes than shorter-term bonds. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. A portion of municipal bond income may be subject to alternative minimum tax. Income may be subject to state and local tax.

About Eaton Vance

Eaton Vance Corp. is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company’s long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today’s most discerning investors. For more information, visit eatonvance.com.

About Asset Class Comparisons

Elements of this report include comparisons of different asset classes, each of which has distinct risk and return characteristics. Every investment carries risk, and principal values and performance will fluctuate with all asset classes shown, sometimes substantially. Asset classes shown are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. All asset classes shown are subject to risks, including possible loss of principal invested. The principal risks involved with investing in the asset classes shown are interest-rate risk, credit risk and liquidity risk, with each asset class shown offering a distinct combination of these risks. Generally, considered along a spectrum of risks and return potential, U.S. Treasury securities (which are guaranteed as to the payment of principal and interest by the U.S. government) offer lower credit risk, higher levels of liquidity, higher interest-rate risk and lower return potential, whereas asset classes such as high-yield corporate bonds and emerging-market bonds offer higher credit risk, lower levels of liquidity, lower interest-rate risk and higher return potential. Other asset classes shown carry different levels of each of these risk and return characteristics, and as a result generally fall varying degrees along the risk/return spectrum. Costs and expenses associated with investing in asset classes shown will vary, sometimes substantially, depending upon specific investment vehicles chosen. No investment in the asset classes shown is insured or guaranteed, unless explicitly stated for a specific investment vehicle. Interest income earned on asset classes shown is subject to ordinary federal, state and local income taxes, except U.S. Treasury securities (exempt from state and local income taxes) and municipal securities (exempt from federal income taxes, with certain securities exempt from federal, state and local income taxes). In addition, federal and/or state capital gains taxes may apply to investments that are sold at a profit. Eaton Vance does not provide tax or legal advice. Prospective investors should consult with a tax or legal advisor before making any investment decision.

©2014 Eaton Vance Management | Two International Place, Boston, MA 02110 | 800.836.2414