The choice for Europe: coming together or breaking apart

September 19, 2014

Economists have spent a lot of time studying the benefits of association. When should firms merge, and when would they be better off remaining separate? Do unions advance the cause of labor, and if so, what kinds of collectives work best? How do financial considerations affect decisions to marry? Economic analysis sheds important light on each of these questions.

Today, Europeans have been asking questions about the benefits of two very large associations. The United Kingdom and the European Union (EU) were founded to promote common interests among their members. They each aimed to foster economic progress and to promote peaceful interaction. To their adherents, they’ve been very successful at delivering on these promises.

But in recent years, separatist sentiments have risen. Poor, uneven economic performance and a fading appreciation of history have led some to wonder whether greater independence would be a better course. Objective analysis dispels this notion, but the politics surrounding the situation have appealed to hearts more so than heads. If not quelled, the growing nationalist sentiment in Europe could reverse important economic and social progress.

I spent last week working in Europe, and the conversations were dominated by discussion of two confederations, one 300 years old and one just over 60. After long runs of success, each has been under some siege. Circumstances for Scotland and the EU certainly differ, but there are a number of common threads.

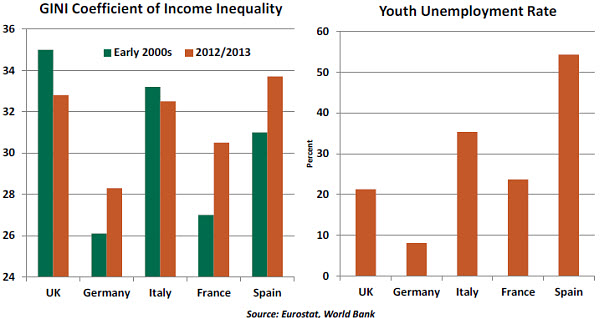

In both places, rifts were developing even before the global financial crisis. Common political institutions left some citizens feeling voiceless, and more open trade produced benefits that were distributed somewhat unevenly. This led to a sense of disenfranchisement among the more-junior partners to the two associations.

The crisis added momentum to the discontent. Internal disagreements over the best way to repair economic damage – stimulus or austerity? currency or wage devaluation? – deepened existing political rifts. The lingering malaise raised long-term unemployment, especially among the young. Calls for greater self-determination consequently grew louder.

Interestingly, even Germany and England – areas on the high side of the recovery – raised questions about continued integration. Neither is overly fond of decisions taken by the EU or the European Central Bank (ECB). Perceived subsidies to weaker members do not play well at home, leading providers to press a stronger sense of economic ethics in exchange for financial aid. Of course, this sort of message is not well-received by the objects of such charity.  Before the centripetal forces increase to an unacceptable level, some perspective is in order. Many who have been considering the fate of the United Kingdom and the European Union are too young to recall the reasons for their formation or to acknowledge the tremendous benefits that they have produced over time.

Before the centripetal forces increase to an unacceptable level, some perspective is in order. Many who have been considering the fate of the United Kingdom and the European Union are too young to recall the reasons for their formation or to acknowledge the tremendous benefits that they have produced over time.

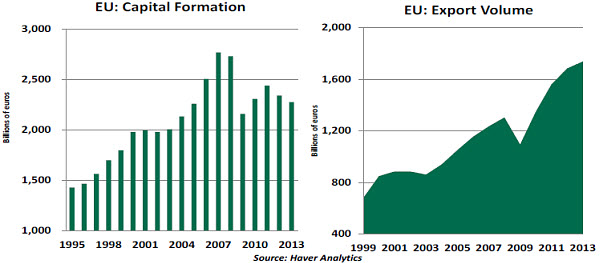

Compacts among nations have a number of advantages. The elimination of economic borders allows free movement of goods and labor, which makes markets more efficient. As the cliché goes, countries can do what they do best and import the rest. Common currencies, product standards, employment rules and safety regulation foster cross-border investment and capital formation.

This brings lower prices to consumers, increases productivity and improves standards of living. Trade volume within Europe and between Europe and other nations has exploded in the past 30 years.

It is certainly fair to observe that trade might have grown importantly without an economic union. But a series of studies examining the question have consistently found significant positive increments to the collective model.

Larger economic blocks, especially those where members are committed to support one another, tend to attract more substantial investments and can house financial markets that are larger and more diverse. Bigger central banks are more resourceful and influential. While some recipients of aid packages from the EU and the ECB bristle at their terms, the availability of support is something that should not be taken for granted.  Finally, and most importantly, expanded economic cooperation is seen as a way to reduce the likelihood of armed conflict. The history of Europe is filled with horrific wars that cost millions of lives. Those who formed the United Kingdom and the European Union were hoping to break that pattern, and they have been successful in that regard.

Finally, and most importantly, expanded economic cooperation is seen as a way to reduce the likelihood of armed conflict. The history of Europe is filled with horrific wars that cost millions of lives. Those who formed the United Kingdom and the European Union were hoping to break that pattern, and they have been successful in that regard.

Unfortunately, European parliamentary elections earlier this year saw gains made by parties that are anti-Europe, anti-market and anti-immigrant. While Scotland may have stepped away from the brink of independence, the terms of its association with London may change. Other regions in Europe are calling for self-determination.

When I enumerated the potential adverse consequences of disunion to Scots I met, I was challenged with the precedent of the American colonies, which opted for separation despite tenuous financial circumstances. But the United States had the whole of the West to explore and exploit, in a world that was much less-reliant on free trade and free capital flows.

One quote from the Revolution did stick in my mind as I thought about the situation in the Old World. “We must all hang together, or assuredly we shall all hang separately,” said Ben Franklin. I hope the spirit of that remark, if not the specifics, resonates with modern-day Europe.

Scotland Votes Nay

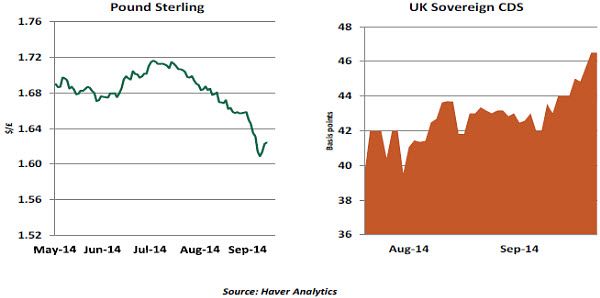

With an extraordinary level of participation, Scotland’s voters opted yesterday to remain part of the United Kingdom – by a margin of 55.3% against independence to 44.7% in favor, and an 85% turnout of voters. The market pundits can heave a sigh of relief; with the uncertainty removed, it’s back to forecasting business as usual. The UK’s economic growth story is intact, investment will flow back into Scottish-based assets, and sterling can continue on its merry way. In addition, with Scotland’s more left-leaning voters still in the fold, the risk of a Conservative government being elected in 2015 and triggering a referendum for the United Kingdom to leave the EU has been significantly diminished.

With a clear margin of defeat – albeit a much narrower one than predicted earlier in the year – there is also little risk of a Quebec-style “neverendum” of constant re-runs. But, it will not be business as usual across the United Kingdom in the coming years.

The leaders of the main UK parties have all promised rapid action to give the Scottish parliament in Holyrood extensive new powers over taxation and spending. With the issue of independence “settled for a generation,” the Scottish Nationalist Party now has every incentive to demand that Westminster make good on its promises. The assemblies in Wales and Northern Ireland are likely to demand similar powers. The prospect of different tax rates, for example, may have interesting implications for investment flows across the United Kingdom.  And in England itself, previous reticence to embrace regional assemblies may give way to demands for more local power. At the least, English Members of Parliament will demand some rights of self-rule. This raises the specter of a national government that cannot control a majority over England-only policy issues.

And in England itself, previous reticence to embrace regional assemblies may give way to demands for more local power. At the least, English Members of Parliament will demand some rights of self-rule. This raises the specter of a national government that cannot control a majority over England-only policy issues.

Finally, despite the result, the nationalist genie has been awakened. Other restive regions will demand the same right to vote on their future, not least Catalonia – the wealthy region that accounts for a full 20% of Spain’s economy. Catalonia's President Artur Mas said today that he will sign a decree to call a referendum on independence on November 9. The national government insists this would be illegal. If the relatively moderate Mas backs down, he could lose power to more-radical groups that will be willing to challenge Madrid. Scotland’s status may be assured for a generation, but Spain’s political scene – and its bond market yields – will be challenged by the issue for some time to come.

The Dollar Rises Again

The dollar registered significant gains vis-à-vis a wide range of currencies recently. Customary questions are trickling in: Is it a durable appreciation of the dollar? What are the implications? We are certain the recent movements of the greenback featured in discussions at the Federal Open Market Committee meeting earlier in the week. Here is our take on the dollar.

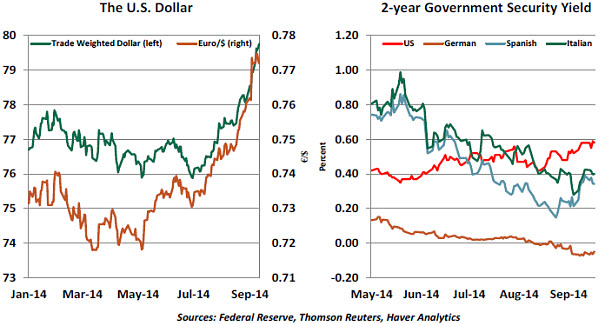

There are a number of reasons for the recent dollar rally. The ECB surprised markets with aggressive monetary policy actions to support economic growth. The ECB’s dovish stance will increase the current interest rate differential between the United States and the eurozone, strongly favoring the dollar. The yield on German two-year government securities turned negative a few weeks ago, while Italian and Spanish two-year government securities are trading at yields of around 35-40 basis points. By contrast, the two-year U.S. Treasury note yields a relatively hefty 60 basis points.

Geopolitical turmoil in the Middle East and the simmering Ukraine-Russia crisis are also drivers of the safe-haven demand for the dollar and U.S. Treasuries. Uncertainty related to the Scottish referendum pulled down the pound sterling vis-à-vis the dollar and the euro.  Will the strong currency serve as a setback to U.S. economic growth? Exports are likely to show a moderating trend as the dollar gains ground. However, this should be of modest significance to U.S. economic growth, as exports account for just 13% of gross domestic product (GDP). By contrast, exports make up nearly 47% of euro area GDP, with a meaningful amount representing exports outside of the region. Likewise, exports are 31% of GDP in the United Kingdom.

Will the strong currency serve as a setback to U.S. economic growth? Exports are likely to show a moderating trend as the dollar gains ground. However, this should be of modest significance to U.S. economic growth, as exports account for just 13% of gross domestic product (GDP). By contrast, exports make up nearly 47% of euro area GDP, with a meaningful amount representing exports outside of the region. Likewise, exports are 31% of GDP in the United Kingdom.

Central banks in Europe can therefore be expected to steer in a manner that keeps downward pressure on their currencies, while this is a much more modest issue for the Federal Reserve and the U.S. Treasury. Gains of the dollar are more problematic for emerging markets, where sustained appreciation of the greenback would result in more expensive imports and inflationary pressures.

It is not an entirely bullish prognosis for the dollar. On the bearish side, Chinese authorities are accumulating reserves at a slower pace and are diversifying their holdings away from the U.S. dollar. Also, the eurozone runs a current account surplus while the United States faces a current deficit, albeit a shrinking one. But, on net, the bullish elements are outweighing the bearish aspects.

As a final thought, the Federal Reserve is winding down its asset purchase program and may soon contemplate changes to forward guidance. The prospect of higher interest rates should drive up the dollar. This development may be helpful to American travelers but will bear monitoring in the world’s financial capitals.