Growth is a strong motivator for initiating mergers and acquisitions (M&A). For years, businesses created progressively more complex organizations, acquiring or expanding into unrelated business lines, consequently often suppressing overall company valuations. The complexity of melding disparate corporations appeared to make it exceedingly difficult for investors to evaluate companies’ true worth. In the present period of slow U.S. economic growth, a new trend in M&A has emerged, as many companies are reversing these moves, benefiting stock prices, investors and, potentially, the economy.

Executive Summary

After years of growing more complex, businesses are increasingly favoring simplification. Many are shedding non-core business lines while other companies are strategically acquiring business lines that fit within their core strengths. Several factors are currently driving this trend, including rising cash levels on balance sheets, an attractive lending environment, and relatively low interest rates. Shareholder activism is an additional catalyst, as hedge funds and other institutional investors seek changes with the goal of unlocking the potential hidden value of these large corporations. The outcome is often mutually beneficial following the transaction, as management can focus on the core business, balance sheets are simplified and stock performance is often enhanced.

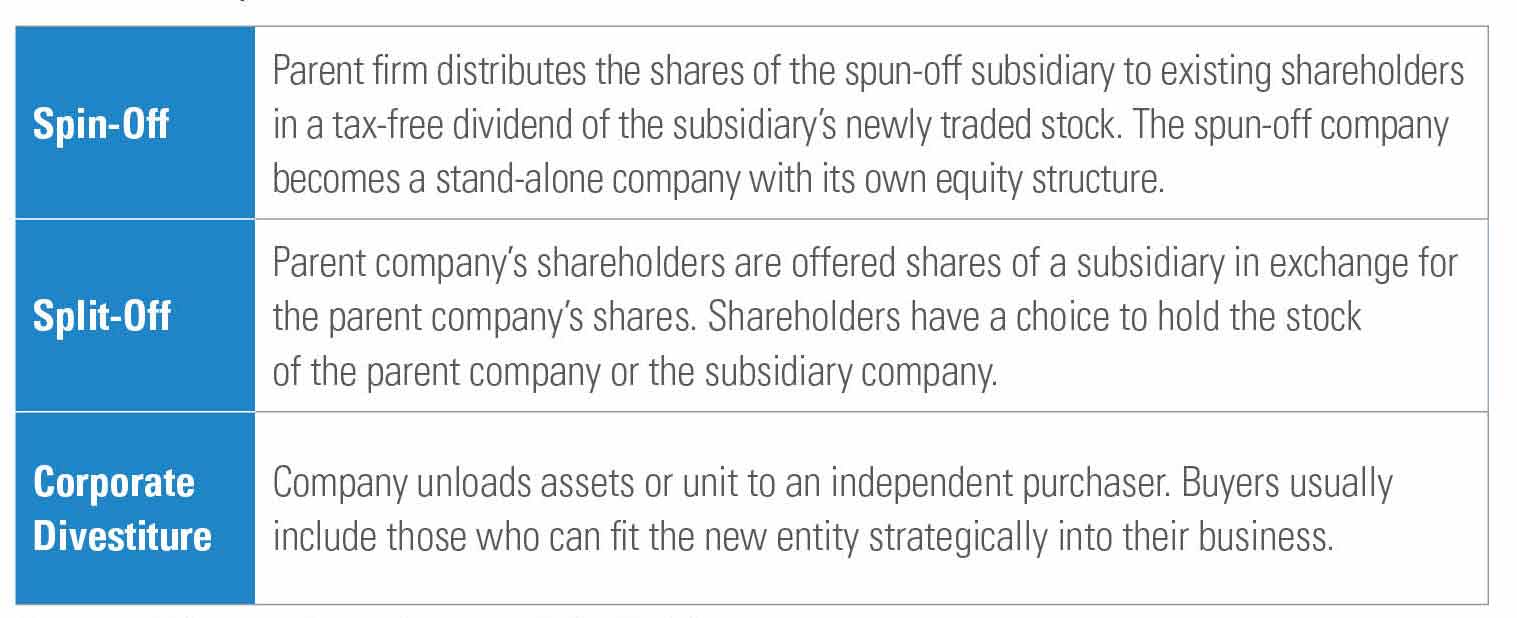

Types of simplifications

When engaging in M&A transactions, companies have multiple ways to restructure or simplify their businesses. Spin-offs, split-offs and corporate divestitures represent three of the most common transactions, with each structure having its own advantages, along with accounting and legal considerations.

Common Simplifications

Sources: PricewaterhouseCoopers, Spinoffadvisors.com

For the purposes of this paper, our focus will be on M&A activity from the perspective of both the buyer and seller.

Forces Driving the Trend of Simplification

Several forces have converged to cause businesses to take action and simplify.

Rising Cash on Balance Sheets

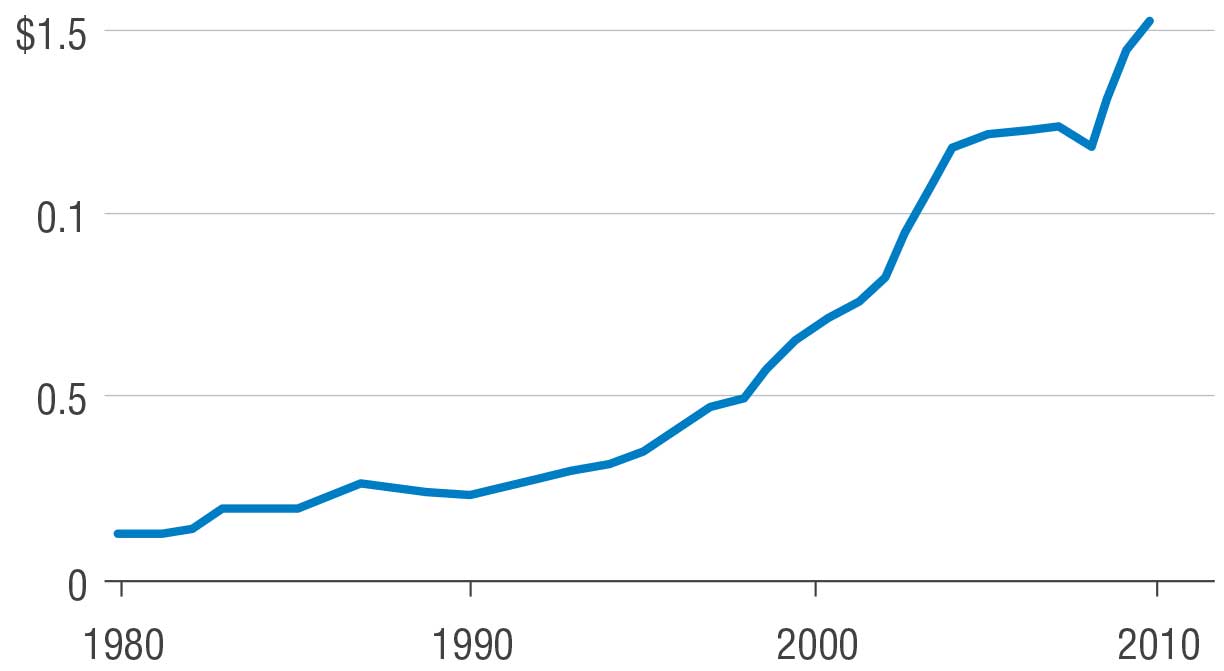

Companies have been holding a high level of cash. According to the Federal Reserve Bank of St. Louis, aggregate cash at non-financial and non-utility U.S. companies rose at a fast pace between 2002 and 2004, rising an average 19%. Cash subsequently leveled off until the end of 2008. Following the Great Recession, cash holdings continued climbing. In fact, by the end of 2013, Moody’s Investors Service found that the top 50 richest non-financial companies held $1.64 trillion in cash,1 a figure slightly larger than Australia’s GDP in 2012.2

Aggregate Cash and Equivalents of Non-Financial Non-Utility U.S. Firms

(in Trillions)

Source: St. Louis Federal Reserve, Compustat

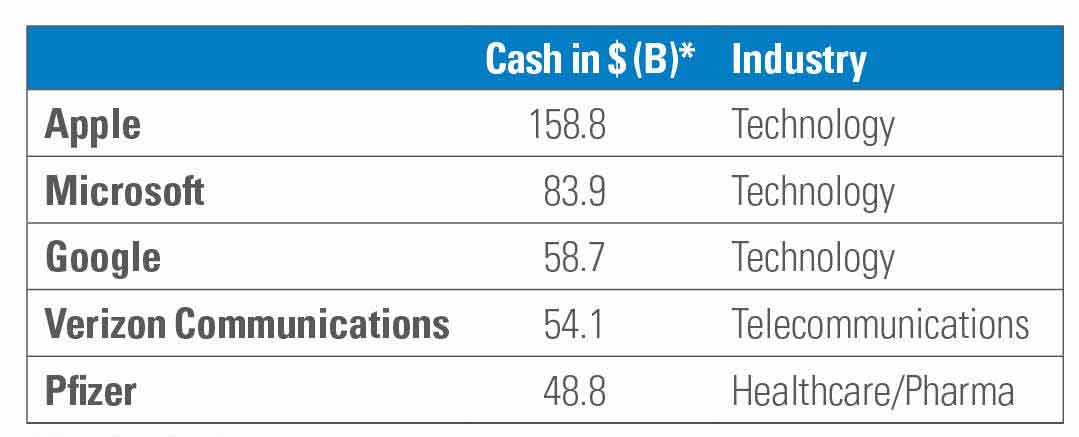

Of those 50 companies, 15 were in the technology sector. Businesses in the healthcare and pharmaceutical, consumer products, automotive and energy industries also topped the list. This industry diversity can be seen in the top five cash-rich firms, shown in the following table. As of December 31, 2013, Apple hoarded the most cash, with the company sitting on $158.8 billion, followed by Microsoft and Google. Verizon Communications and Pfizer also made the top 5. All of these companies held cash totaling approximately $50 billion or more on their balance sheets as of the end of 2013.3

Top 5 U.S. Companies with Most Cash

Companies flush with cash may not be making the most efficient use of their capital structures. Some research suggests stockpiles of cash may have come at the expense of capital spending on facilities, equipment, or new business initiatives. The U.S. Commerce Department indicated that capital spending languished in 2013, growing at its slowest pace in three years. This underinvestment could partially explain the lagging economic growth and elevated unemployment levels.

However, recent earnings reports show companies are beginning to spend their cash hoards, choosing to engage in M&A transactions, increase dividends, or buy back stock. Buybacks have been particularly aggressive: Over the trailing 12-month period as of December 31, 2013, 3.1% of outstanding shares were repurchased by companies. Businesses in the information technology and financials sectors had the largest increase of buybacks, with technology companies spending $34.6 billion in the fourth quarter of 2013 alone, according to Factset Research Systems.4 Looking ahead, repurchases may slow, as higher share prices make buybacks less attractive.

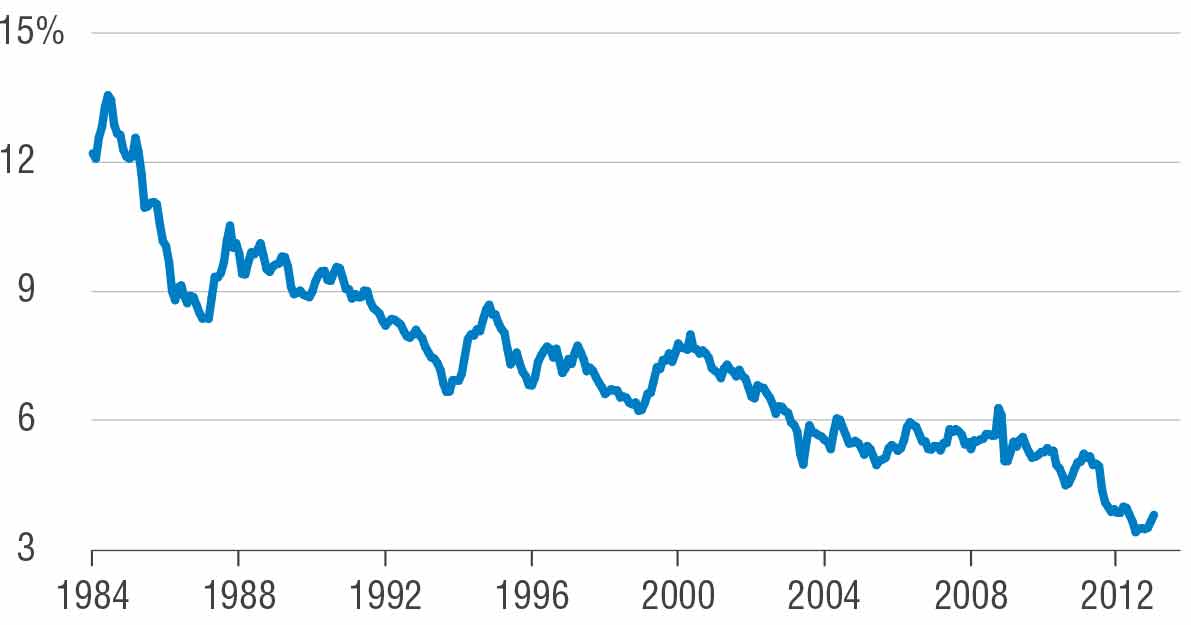

Low Interest Rates

With the Federal Reserve keeping interest rates at or near record low levels, debt financing has been inexpensive. Since the Great Recession, the yield on Aaa-rated corporate debt by Moody’s Investors Service has fallen to 50-year lows.5

As a result, many companies have been incentivized to issue corporate bonds, as they provide a relatively low cost of capital compared to the cost of equity capital.

Moody’s Seasoned Aaa Corporate Bond Yields, 1984-2013

Source: Board of Governors of the Federal Reserve System, Moody’s Investors Service

Funding is Plentiful

Corporate bonds have become increasingly attractive to investors, as U.S. Treasury yields remain modest and the expectation for inflation continues to be low.

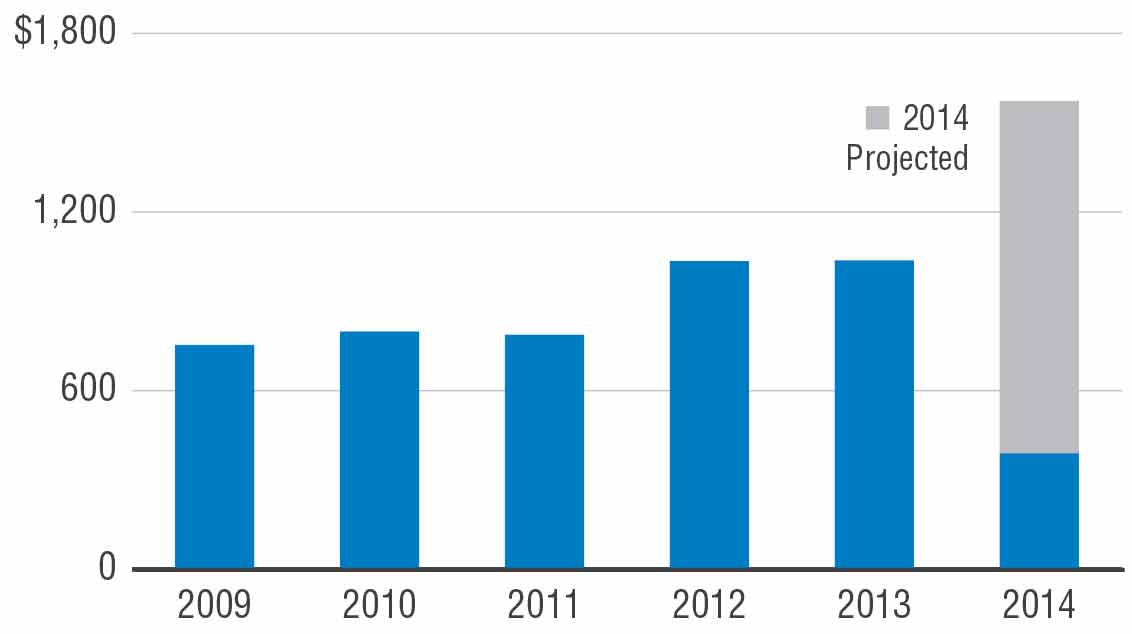

Responding to investors’ interest for higher-yielding fixed income products, companies have been issuing more debt. In 2012 and 2013, U.S. investment grade and high yield corporate bond issuance was more than $1 trillion. According to the Securities Industry and Financial Markets Association, issuance in 2014 is expected to climb even higher, potentially reaching nearly $1.5 trillion.

Maturity dates are becoming longer as well. From the period of January through April 2014, $48 billion of long-dated corporate debt was issued, which is 20% higher than the same period in 2013.6 Multiple companies issued 30- and 50-year bonds in the spring of 2014, including a construction-equipment maker which sold 50-year bonds at the request of an institutional investor, offering a yield of 1.375% more than the comparable Treasury.7

With plentiful funding and attractive borrowing rates, many companies may appear to be building cash reserves to take advantage of future opportunities.

U.S. Corporate Bond Issuance Investment Grade and High Yield

(in Billions)

Source: Securities Industry and Financial Markets Association

Role of Shareholder Activism in M&A

Shareholder activism, led by hedge funds and institutional investors, has been a strong catalyst in effecting change to companies’ capital structures in recent years. In 2013, about 240 companies became the targets of activist investors, an increase compared to the previous year, when 218 businesses were influenced by shareholder activism.8

In the 1980s, shareholder activism had a negative connotation in the market. Many activists were viewed as corporate raiders involved in takeover battles for short-term gain. Today’s activist firms have been more strategic in nature, targeting companies that have experienced sluggish growth. Hedge fund managers, such as Bill Ackman, Carl Icahn and Dan Loeb, have brought additional experience and wisdom to the board room, pushing companies to make changes.

Activists’ strategies vary: They build an equity stake and gain board representation in an attempt to implement cost-cutting actions, sell or retain assets or influence a spin-off or sale of a business division. Importantly, many have been successful in encouraging company management to make changes to their capital structure or engage in M&A transactions. Of the companies where activists sought or gained board representation in 2013, share prices rose an average of 47%.8

These activists have played a “growing role in countering corporate inertia and clubbiness, in driving M&A activity, and most crucially in unlocking value,” benefiting the targeted company, investors and the economy, according to Fortune.9

Reasons for Simplification

Companies streamline operations and simplify business lines for multiple reasons. First, extraneous business lines can be costly distractions. In research published by the Journal of Financial Economics, Owen Lamont and Christopher Polk, found that diversified firms tend to have a suppressed value due to an inefficient allocation of capital across their differing business lines, regardless of whether the increased diversity comes from external or internal factors.10

The world’s most innovative companies additionally benefited from a narrowed focus. Of 1,000 public companies world-wide that spent the highest amount on research and development, the most successful firms focused on their “distinct capabilities that enable them to better execute their chosen strategy,” according to Booz & Co. These companies aligned their innovation strategy with their overall corporate strategy, and were subsequently rewarded by the market.11

Second, transactions tend to be accretive to earnings per share after factoring in the costs of the transaction. During the current M&A cycle, both buyer and seller experienced an uptick in their stock prices. In fact, year-to-date through April 2014, shares of acquiring companies increased an average of 4.4% within a day of the deal being announced.12

This has not historically been the case. Following an M&A announcement, the buyer would often need to provide justification for the purchase to the investment community to defend the stock price. It appears investors believe companies are putting cash reserves to better use.

Conclusion

Over the next few years, M&A is expected to intensify. We believe the environment remains conducive for companies to pursue simplification: U.S. economic growth remains unimpressive, corporate cash levels are high, borrowing is relatively inexpensive, and debt funding is plentiful. In addition, with the success that shareholder activists have had in 2013, assets under management in these hedge funds have increased, allowing managers to pursue additional opportunities.

This whitepaper is based on the insights of:

Francis X. Gallagher

Portfolio Manager

• 30 years of investment experience

• Joined Visium in 2011 upon the completion of a strategic transaction between Catalyst Investment Management Co., LLC and Visium

Asset Management, LP

• Previously served as the Director of Research for Oscar Gruss & Son Incorporated, Phoenix Capital Markets and Gallagher Equities

Peter A. Drippé, CFA

Portfolio Manager

• 29 years of investment experience

• Joined Visium in 2011 upon the completion of a strategic transaction between Catalyst Investment Management Co., LLC and Visium

Asset Management, LP

• Previously served as Vice President of the proprietary trading desk in the convertible arbitrage department at PaineWebber. Also focused on convertible arbitrage, merger arbitrage, and high yield debt strategies at Highbridge Capital Management

About VISIUM

Founded in 2005 by Jacob Gottlieb, MD, CFA, Visium Asset Management, LP is dedicated in its efforts to seek high-quality, low-correlated returns in a variety of market environments for high net worth individuals and institutional clients.

Headquartered in New York City, Visium manages over $6.5 billion as of March 31, 2014 in long/short equity, credit, multi-strategy and event driven strategies. In addition to the Visium Mutual Funds, Visium manages five private funds. The firm has a staff of over 140 professionals.

References

1 “US non-financial corporates’ cash pile grows, led by technology,” Moody’s Investors Service, March 31, 2014.

2 World Development Indicators, The World Bank, 2014.

3 Ciaccia, Chris. “Top 50 Cash-Rich Companies In the U.S.,” TheStreet, March 31, 2014.

4 Factset Buyback Quarterly, March 25, 2014.

5 Board of Governors of the Federal Reserve System, Moody’s Investors Service, 2014.

6 Cherney, Mike. “Investors Are Hungry for U.S. Corporate Bonds,” The Wall Street Journal, December 15, 2013.

7 Cherney, Mike and Monga, Vipal. “Caterpillar Sells 50-Year Bonds,” The Wall Street Journal, May 5, 2014.

8 “The Activist Insight Activist Investing Review 2014,” Schulte Roth & Zabel LLP, 2014.

9 Studzinski, John. “Shareholder Activists Up Their Game,” Fortune. April 28, 2014.

10 Lamont, Owen and Polk, Christopher. “Does diversification destroy value? Evidence from industry shocks,” Journal of Financial Economics. 2002.

11 Jaruzelski, Barry and Dehoff, Kevin. “How the Top Innovations Keep Winning: The Global Innovation 1000,” Booz & Co. Winter 2010.

12 Hammond, Ed. “Encouraging signs that 2014 M&A spree is the real deal,” Financial Times April 27, 2014.

Disclosure

The fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The statutory prospectus and, if available, summary prospectus contains this and other important information about the investment company, and it may be obtained by calling 1-855-9VISIUM. Read it carefully before investing.

Mutual fund investing involves risk. Principal loss is possible. Event-driven investments carry the risk that an expected event or transaction may not be completed, or be completed on less favorable terms than expected. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in lower-rated and non-rated securities present a greater risk of loss to principal and interest than higher rated securities. The fund may make short sales of securities, which involves the risk that losses to those securities may exceed the original amount invested by the Fund. Investments in foreign securities involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for emerging markets. Investments in micro, small and medium capitalization companies involve less liquidity and greater volatility than investments in larger companies. The Fund may use certain types of investment derivatives such as futures, forwards, and swaps. Derivatives involve risks different from, and in certain cases, greater than the risks presented by more traditional investments. The Fund may purchase IPOs (initial public offerings) which can fluctuate considerably and could have a magnified impact on fund performance when the Fund’s asset base is small. The Fund may invest in other investment companies and ETFs and will bear its share of fees and expenses, in addition to indirectly bearing the principal risks of those underlying funds. The Fund may have a higher turnover rate which could result in higher transaction costs and higher tax liability which may affect returns.

Aaa-rated debt is the highest possible rating assigned to the bonds of an issuer by credit rating agencies. Earnings per share is the dollar value of earnings per each outstanding share of a company’s common stock. As of 3/31/14, the fund does not hold any of the stocks mentioned in this report.

The Visium Event Driven Fund is distributed by Quasar Distributors, LLC.